Diversification myths: How to avoid overlap and really spread risk

Diversification is often touted as the core principle of smart investing—the “free lunch” that reduces risk without sacrificing returns. Yet many investors, despite their best efforts, fall into common traps and misconceptions that diminish the true benefits of diversification. In 2025’s complex and interconnected markets, it’s more important than ever to understand the reality behind these myths. Are you truly diversified, or are hidden overlaps exposing your portfolio to unintended risk? This guide will bust the most widespread diversification myths, reveal why overlap matters, and offer practical ways to build genuinely resilient portfolios.

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam

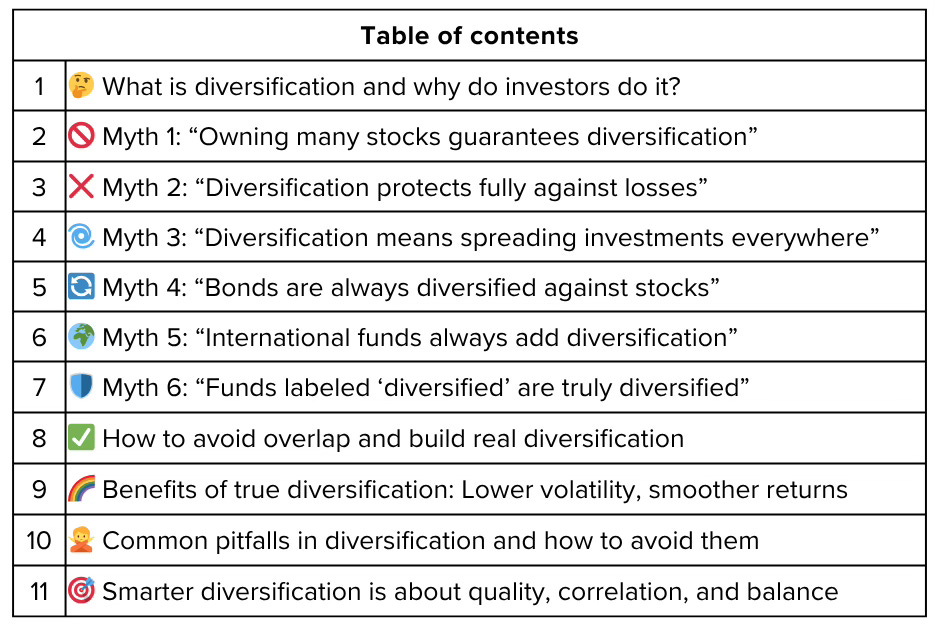

What is diversification and why do investors do it? 🤔

Diversification means spreading your investments across different asset types, sectors, geographies, and strategies to reduce overall risk. The idea:

Avoid putting all your eggs in one basket.

Mitigate the impact if any individual investment or sector drops sharply.

Smooth out returns and help your portfolio survive downturns.

However, true diversification goes deeper than just owning many stocks or different mutual funds. It’s about owning assets that react differently under the same market conditions, measured by correlation, and understanding your portfolio’s risk profile.

Myth 1: “Owning many stocks guarantees diversification” 🚫

Many investors think having 20, 30, or more stocks means they are diversified. This is only partly true.

Why more stocks alone isn’t enough:

If most holdings are in the same sector or influenced by the same economic forces, your risk is still concentrated.

Many mutual funds or ETFs hold mostly the same big companies; adding several funds with large overlaps increases your exposure to those common stocks, not diversification.

At around 20-30 stocks, most benefits of risk reduction happen—but only if they are from truly different sectors, countries, or have low correlations.

Real-world example:

Holding 30 tech stocks doesn’t reduce risk much compared to 5, because their prices tend to move together. Conversely, adding bonds, real estate, or commodities can diversify risk away.

Myth 2: “Diversification protects fully against losses” ❌

Diversification can reduce the impact of losses, but it cannot eliminate losses entirely.

During major market crashes (2008 global financial crisis, 2020 pandemic crash), almost all asset classes fell together.

Correlations between assets often increase during crises, reducing diversification benefits right when you need them most.

Diversification is about reducing risk, not avoiding it. Losses are a normal part of investing.

Understanding this helps set realistic expectations—diversification smooths the ride but doesn’t offer a bulletproof shield.

Myth 3: “Diversification means spreading investments everywhere” 🌀

Overdiversification, sometimes called “diworsification”, is a real risk.

Spreading money across too many assets or funds can dilute potential gains.

It complicates portfolio management, increasing transaction costs and tax inefficiencies.

Gains in some investments may be offset by losses or flat performance in others, turning your portfolio into a zero-sum game.

Smart investing is about choosing the right mix, not just more holdings. Target 60–80 positions or holdings that truly contribute to diversification, focus on quality, and avoid redundant exposure.

Myth 4: “Bonds are always diversified against stocks” 🔄

Bonds are often seen as a safe counterbalance to stocks, but this relationship can vary widely.

Some bonds, like corporate bonds with equity-like risks, may correlate positively with stocks.

Government bonds usually have low or negative correlation, but during certain sell-offs, even government bonds fall together with stocks.

Duration matters: long-duration bonds are more interest-rate sensitive and can react differently than short-term bonds during inflation scares.

Diversifying within fixed income—across durations, credit qualities, and geographies—is as important as diversifying stocks.

Myth 5: “International funds always add diversification” 🌍

Investing overseas does add diversification—different economies, currencies, and sectors react differently to global events.

But beware: many “international” funds hold large positions in the same mega-cap stocks traded domestically (e.g., Apple, Microsoft), reducing diversification benefits.

Currency risk can add both return potential and volatility.

Emerging markets carry higher risk but also opportunity for diversification.

Proper international diversification means looking beyond terminology and analyzing actual holdings and correlations.

Myth 6: “Funds labeled ‘diversified’ are truly diversified” 🛡️

Labels can be misleading:

Some funds call themselves “diversified” but concentrate heavily in popular sectors or top stocks.

Multi-asset funds might underweight non-correlated asset classes.

Fixed-income funds can largely hold government bonds; equity funds may be mostly U.S. large caps.

Review fund holdings and overlaps with your overall portfolio to know where your risks really lie.

How to avoid overlap and build real diversification ✅

1. Analyze your holdings in detail

Look through your portfolio or funds, studying sector, geographic, and individual stock overlaps. Use tools or platforms that help calculate correlations and concentration.

2. Diversify across truly distinct drivers of returns

Blend asset classes (stocks, bonds, commodities), styles (value, growth), geographies (domestic, emerging, developed), and strategies (passive, smart beta, alternatives).

3. Balance portfolio concentration

Avoid overconcentration in a few mega-cap or sector bets. Consider equal weighting or smart beta approaches to spread risk evenly.

4. Understand factor exposures

Know if your funds tilt toward value, momentum, or quality. Factor diversification reduces risk more than just sector or country diversification.

5. Use alternative assets when appropriate

Consider real estate, infrastructure, gold, private equity, or hedge funds for low correlation and enhanced risk smoothing.

6. Rebalance regularly

Market moves can skew your allocation. Periodic rebalancing backs gains from concentrated positions and restores target diversification.

Benefits of true diversification: Lower volatility, smoother returns 🌈

Diversified portfolios:

Experience lower drawdowns and smoother equity exposure.

Gain exposure to multiple economic environments.

Reduce the risk of permanent loss linked to single companies, sectors, or markets.

Improve the reliability of returns across market cycles.

True diversification also improves the likelihood of compounding wealth steadily—investors avoid panic selling during crises and cut risk when needed.

Common pitfalls in diversification and how to avoid them 🙅

Ignoring correlation: More assets don’t mean better diversity if they move together. Check real correlations, especially during stress events.

Chasing trends blindly: Don’t pile into the “diverse” trendy asset class without understanding its risks.

Overtrading: Constant buying and selling to diversify too quickly can drive up costs and reduce net returns.

Neglecting costs and taxes: Diversify efficiently with low-cost ETFs, mutual funds, and mindful tax management.

Smarter diversification is about quality, correlation, and balance 🎯

Diversification is essential—but the common myths can trap investors into thinking they’re safer than they really are.

Overlap, correlation, and hidden risks can break a portfolio’s promise of protection.

True diversification comes from understanding the drivers of return and risk, selecting complementary assets, and managing exposures thoughtfully.

By busting myths and applying smart strategies, investors can build portfolios that absorb shocks, capture cycles, and grow wealth sustainably in 2025 and beyond.

Remember: Diversification is a tool to manage risk—not a guarantee against loss. Using it wisely takes education, discipline, and constant monitoring.

Poll 📊

🚀 Join 60,000+ investors—become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research and consider seeking professional financial advice before making any investment decisions.

The myth about owning many stocks really resonnated, especially after your previous piece on market biases. It makes me question if we often overestimate our own financial literaci.