Walmart is not just a big box anymore. It’s sitting on one of America’s fastest-growing ad businesses.

Buying Walmart because it sells cheap groceries may have worked. Not anymore. Walmart’s advertising business just crossed $6.4 billion in annual revenue, growing 46% in a single year, nearly three times faster than the company’s overall sales. Advertising and membership combined account for roughly one-third of US operating income. And while every other retailer is panicking about tariffs, Walmart is using the chaos to squeeze better prices from suppliers and steal higher-income shoppers from rivals that cannot match its speed.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors think of Walmart as a giant grocery store with a car park. That framing is outdated. Walmart’s retail business is real and enormous, but it runs on margins thin enough to make a banker wince. The parts of the business quietly compounding are an advertising engine, a membership flywheel, and a global e-commerce operation clocking its twelfth straight quarter of double-digit US growth.

In a tariff-disrupted 2026, where “retailer” has become shorthand for “supply chain casualty,” Walmart’s scale and supplier leverage put it in a structurally different position. That resilience is not an accident, and it is not priced in by the people still calling this a grocery stock.

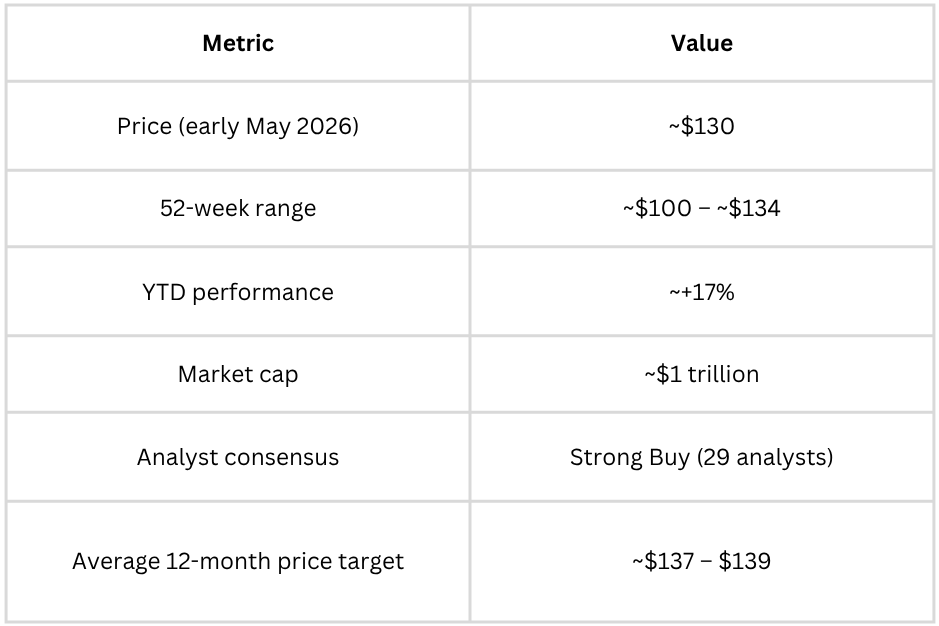

🔥 Top movers

Note: WMT has delivered approximately 17% year-to-date through early May 2026, outpacing the S&P 500’s roughly 8% return over the same period, per Yahoo Finance. Price levels are approximate, drawn from publicly available market data.

🛒 Not one store, but four businesses

Four distinct operations run under one roof, each with materially different economics.

Walmart US is the anchor, with over 4,700 supercenters and neighbourhood markets, the largest grocery retailer in the US by sales volume, and the operating platform on which the faster-growing businesses are built.

Sam’s Club is the membership model within the umbrella. It earns recurring income through fees that carry margins dramatically higher than standard retail, with more than half of US members now transacting digitally, per company disclosures.

Walmart International covers China, Mexico through Walmex, and most consequentially for Indian investors, Flipkart. International net sales exceeded $100 billion in the most recently reported fiscal year, according to company filings.

Walmart Connect is the advertising business, a retail media platform that did not meaningfully exist six years ago and has since become the engine driving the consolidated margin profile of the entire company.

🌀 Turning the tables

How is Walmart repositioning from a cost-leadership retailer into a multi-revenue-stream platform? Three mechanics are doing the work.

1. The store-as-fulfilment-centre model. Walmart’s 4,700 stores are the last-mile infrastructure for one of the fastest delivery networks in US retail, offering store-fulfilled fast delivery to 95% of the US population, per Q4 earnings disclosures. Roughly 60% of e-commerce units are delivered same-day or faster, with 70% of those arriving in under an hour, per company commentary. No pure online rival can replicate this without building the physical footprint Walmart has spent decades constructing.

2. The first-party data flywheel. Every transaction across Walmart’s stores, app, and Sam’s Club feeds Walmart Connect’s targeting. When a brand advertises on Walmart’s platform, it can measure exactly how many units were sold as a direct result, a closed-loop attribution capability neither Google nor Meta can offer because neither owns the checkout. Vizio adds the living-room layer, connecting TV viewing to purchase data on the same platform.

3. Domestic sourcing as a structural tariff moat. Roughly two-thirds of the goods Walmart sells in the US are sourced domestically, per company disclosure, and the company has pledged $350 billion in US-sourced products over the next decade, per company announcements. When tariffs hit, Walmart goes back to suppliers and renegotiates. Its purchasing volume gives it leverage that smaller retailers do not have.

✨ What is working

Several structural advantages are compounding, independent of any single quarter.

Operating income is consistently growing faster than revenue—a spread that signals the business mix is shifting toward higher-margin lines. Management has guided this pattern to continue through fiscal 2027.

The higher-income shopper capture is becoming a structural shift. CFO John David Rainey told CNBC that market share gains were “larger among upper-income households.” For fashion specifically, almost all of the mid-single-digit growth in Q4 came from households earning over $100,000 annually, people with larger baskets and more general merchandise in their carts.

Private label is expanding steadily, and pricing discipline is holding. Grocery private brand penetration was up approximately 60 basis points year-over-year in Q1 fiscal 2026, per company commentary, and Walmart has maintained its price gap versus competitors even as tariffs push costs higher across the sector.

Want to add Walmart to your portfolio? Trade $WMT directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

📢 The ad machine nobody is talking about

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.