Uber (UBER): The $44 billion platform hiding inside the world’s most recognisable taxi app

Analysing Uber meant picking a side in a culture war — Travis Kalanick’s burn-it-all-down growth machine versus every regulator, driver, and competitor it had steamrolled along the way. Not anymore. Today’s Uber is one of the most quietly sophisticated platform businesses in the world: a membership flywheel, an advertising network built on first-party location data, and the distribution layer that every autonomous vehicle company needs actually to make money. None of that shows up in the “gig economy taxi app” framing the financial media still defaults to.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors still think of Uber as the company that disrupted taxis and made Travis Kalanick infamous. That framing is accurate and dangerously incomplete. Today’s Uber simultaneously operates the world’s largest ride-hailing platform, the second-largest food delivery network in the US, a freight brokerage moving billions in cargo, and a nascent advertising business that crossed a $1 billion annual revenue run rate in 2024. It completed an estimated 11-12 billion trips in 2024 — roughly 30-33 million every single day (author’s estimate derived from summing quarterly disclosed trip figures). And it did all of this while turning structurally profitable for the first time, generating more free cash flow in a single quarter than it produced in its entire pre-2021 existence.

But the story that the market is still figuring out is not about what Uber already is. It’s about what Uber is becoming: the platform that every autonomous vehicle company needs to reach riders at scale, the subscription flywheel that locks in the most valuable urban consumers, and an advertising network sitting on first-party location data that most media companies would pay almost anything to access. The transformation isn’t cosmetic. Whether investors are fully positioned to benefit from it depends on understanding a business model that looks almost nothing like the “gig economy taxi app” framing that still dominates the conversation.

🧩 What Uber actually is today

Uber is a demand aggregation platform. It does not own cars, employ drivers, or cook food. What it owns is the matching layer — the algorithm, the app, the brand trust, and the network density — that connects riders to drivers, hungry people to restaurants, and shippers to carriers. That sounds simple. The economics of it are not.

The platform model means Uber’s unit economics improve as the network gets denser. More riders attract more drivers, shorter wait times attract more riders, and higher driver earnings attract more drivers. This is the classic marketplace flywheel, and Uber has spent fifteen years and tens of billions of dollars building one that operates in 70+ countries. That geographic scale is the structural moat, and it is far harder to replicate than it looks from the outside.

The business today has three operating segments — Mobility (ride-hailing), Delivery (food, grocery, and alcohol), and Freight (digital trucking brokerage) — plus two overlapping platform layers: Uber One (the membership programme that bundles benefits across both consumer segments) and Uber Advertising (the ad network built on top of the platform’s first-party data). Understanding how these interact is the key to understanding the bull thesis.

Uber One is now available in 34 markets globally. Members generate a disproportionate share of gross bookings, use the platform more frequently, and churn at significantly lower rates. In Q3 2024, Uber reported over 25 million Uber One members globally, per its earnings release — a number that had been growing rapidly. Members, per management commentary, represented approximately 35% of total Mobility and Delivery gross bookings in late 2024. That’s a cohort generating outsized economics, sticky behaviour, and cross-platform engagement — more like an Amazon Prime dynamic than a standard ride-hailing loyalty programme.

📊 Segment breakdown

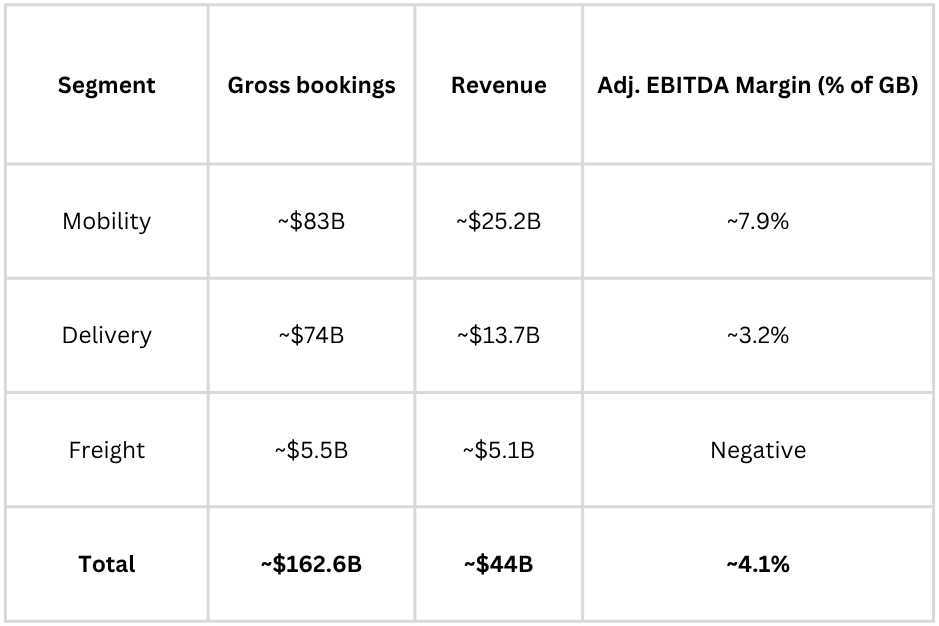

Uber’s reported revenue understates the true scale of the business. The more relevant top-line metric is Gross Bookings — the total value of transactions flowing through the platform — because Uber’s revenue margin (the take rate it keeps from those bookings) varies meaningfully by segment.

Full year 2024, reported results (per Uber earnings releases and SEC filings)

A few things worth unpacking here.

Mobility revenue margin is around 30% — meaning Uber keeps roughly 30 cents of every dollar of ride bookings after paying out drivers. Delivery margin is lower at roughly 18-19%, reflecting the more competitive economics of food delivery. Freight is a largely pass-through logistics brokerage with tight margins, currently operating near breakeven on an adjusted basis amid a challenging freight market cycle.

The overall adjusted EBITDA margin of ~4% on gross bookings sounds thin. But gross bookings grew 18% in 2024 to approximately $162.6 billion, while adjusted EBITDA grew approximately 60% year-over-year to roughly $6.5 billion — meaning profitability is expanding materially faster than the top line as fixed costs leverage against a growing transaction base, per Uber’s Q4 2024 earnings release.

Operating income reached $2.8 billion for the full year 2024, up from $1.1 billion in 2023, per the same release.

Want to add Uber to your portfolio? Trade UBER directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

🚀 The growth engine: Platforms, AV, and advertising

Three distinct growth engines are compounding simultaneously inside Uber. None of them is the core ride-hailing business — though that business continues to grow solidly.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.