This week’s stock shocks as of 17th July, 2026

Watching US markets week to week without context is just noise. This week had a bank earnings season that smashed every estimate on the board, a June inflation print that fell the most in six years, a new Fed chair who refused to take the win, Iran re-escalating the Strait of Hormuz standoff, and then a Thursday chip-stock selloff that undid almost all of it—triggered by a chipmaker that actually beat and raised guidance. That’s five sessions, four narratives, and a market that couldn’t decide which one to trade. That’s why we built Winvesta Crisps—to cut through the noise and tell you what actually moved markets and why. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Banks turned in one of the strongest quarters Wall Street has seen in years. Inflation data came in cooler than anyone expected. And none of it mattered once Taiwan Semiconductor beat estimates, raised its capex guidance, and watched its stock—and the entire chip complex—sell off anyway. This was the week the market stopped rewarding good news reflexively and started asking, “At what price?”

📊 Market recap

Monday opened with a fresh jolt from the Gulf. President Trump announced he was reinstating what he called a blockade on Iranian shipping through the Strait of Hormuz after the US and Iran traded fresh attacks over the weekend and Tehran said it had closed the waterway, undercutting an interim ceasefire signed just weeks earlier. Brent crude posted its biggest one-day gain in more than six years, surging roughly 9.6% to settle near $83.80, per Reuters. Equities fell broadly—the S&P 500 dropped 0.79% to 7,515.34, the Nasdaq slid 1.55% to 25,873.18, and the Dow eased 0.26% to 52,498.64, per CNBC. Energy, financials, and utilities were the only pockets of green; chip stocks led declines, with memory maker SK Hynix down about 9%.

Tuesday was “earnings super Tuesday.” JPMorgan Chase, Goldman Sachs, Wells Fargo, Citigroup, and Bank of America all reported before the bell, on the same morning as the June CPI report and new Fed Chair Kevin Warsh’s first testimony before the House Financial Services Committee. CPI fell 0.4% month-over-month, the steepest monthly decline in six years—pulling the annual rate down to 3.5% from May’s elevated print, per the BLS and FXStreet. Goldman Sachs posted a record quarter, with EPS of $20.98 against a roughly $14.5 estimate, and JPMorgan beat by one of its widest margins in years. Not every bank was rewarded, though: Citigroup and Wells Fargo both beat estimates and still saw their shares fall. Warsh, testifying for the first time as chair, explicitly declined to call the softer inflation data “mission accomplished.” Indexes rose regardless—the S&P gained 0.38% to 7,543.59, the Nasdaq added 0.9% to 26,107.01, and the Dow ticked up 0.02% to 52,508.27, per CNBC.

Wednesday brought Warsh’s second day of testimony, this time to the Senate Banking Committee, alongside a June Producer Price Index that unexpectedly fell 0.3%—its first monthly drop in nearly a year—with core PPI up a modest 0.1%, per the Labor Department and Axios. Rate-hike odds cooled sharply: CME FedWatch data showed the probability of a hold at the July 29 meeting rise to around 86%, while the odds of a September hike fell to roughly 44% from 50% the day before, per TradingEconomics. Morgan Stanley beat estimates comfortably (EPS $3.46 versus $2.89 expected). Oil held steady as the US carried out further strikes on Iran and reinstated its naval blockade, with WTI at $79.60 and Brent at $84.95, per CNBC. Indexes closed at fresh weekly highs—S&P +0.4% to 7,572.42, Nasdaq +0.62% to 26,269.23, Dow +0.29% to 52,658.64—and the VIX fell 5% to 15.67.

Thursday was the week’s real turning point. Taiwan Semiconductor reported a Q2 beat, with revenue of $40.2 billion near the top of its own guidance range, and raised its 2026 capital expenditure forecast to $60-64 billion from $52-56 billion—and its stock fell anyway, dragging the rest of the chip complex down with it. Micron, Intel, AMD, and Broadcom all declined more than 5%, while Alphabet dropped roughly 4.4-4.6% on reports that Google’s flagship AI model is running months behind schedule, per Bloomberg. June retail sales rose a modest 0.2% (in line with estimates, down from May’s revised 1% gain), and jobless claims fell to 208,000. After the close, Netflix’s Q2 numbers were roughly in line with estimates, but Q3 revenue guidance of $12.86 billion missed the Street’s roughly $13 billion estimate, and shares sank about 9% in after-hours trading, per CNBC. The CNN Fear & Greed Index slid into “Fear” territory for the first time in weeks. Indexes: S&P -0.51% to 7,533.77, Nasdaq -1.47% to 25,881.95, Dow -0.20% to 52,552.97; the VIX jumped 6.76% to 16.73.

Friday opened lower, extending Thursday’s chip-led rout. Nasdaq 100 futures fell further after Thursday’s 1.6% drop, with Netflix’s post-earnings slide adding to the overhang. Asian markets sold off broadly overnight—Japan’s Nikkei fell around 4% and China’s CSI 300 dropped roughly 3.6%—while European chip-equipment names like ASML and ASMI slid in sympathy. Friday’s economic calendar included housing starts, industrial production, import and export prices, and the preliminary University of Michigan consumer sentiment reading. Heading into the session, the week-to-date scoreboard read: S&P 500 down about 0.6%, Dow down about 0.2%, and Nasdaq down roughly 1.5%, per CNBC—a week that touched nearly every major 2026 storyline (Iran, the Fed, AI capex) and still ended in the red.

😶🌫️ Sentiment watch

The CNN Fear & Greed Index moved into “Fear” territory by Thursday, with independent trackers putting the reading in the low-to-mid 40s heading into Friday—a meaningful shift from the calmer, more neutral tone that had prevailed through Wednesday. The VIX told a similar story: it fell to 15.67 on Wednesday, a multi-week low, before jumping 6.76% to 16.73 on Thursday as the chip selloff spread.

That’s not panic—the VIX remains well below the levels seen during the sharpest phases of this year’s Iran-driven selloffs—but the direction matters. A market that spent Tuesday and Wednesday celebrating beats from banks and cooling inflation data spent Thursday deciding that a semiconductor giant’s beat-and-raise quarter wasn’t good enough. That’s a market genuinely unsure which of its own storylines to believe.

The stocks moving markets this week are all tradable from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber, or download the Winvesta app and fund your account to get insights like this for free!

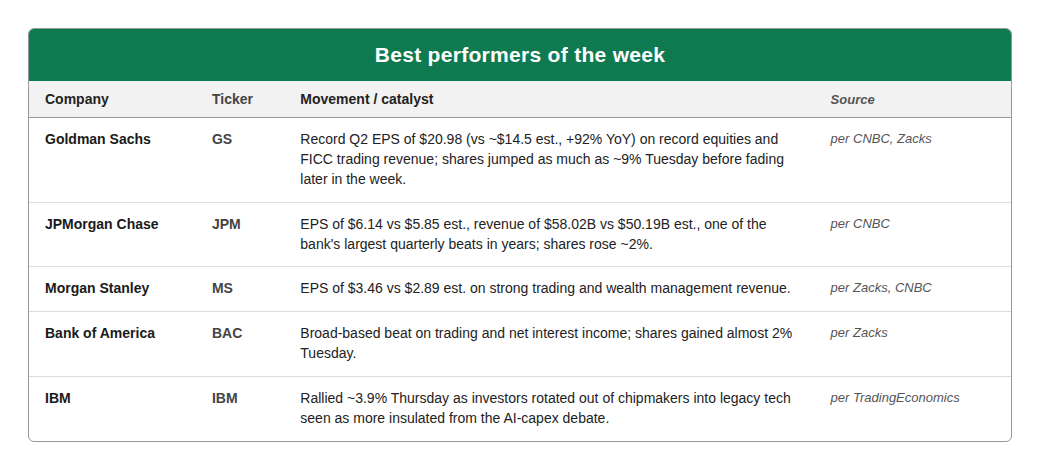

🏆 Best performers

Wall Street’s biggest banks delivered one of the strongest quarters in years. Goldman Sachs posted record trading and investment-banking revenue that nearly doubled year-over-year profit, and JPMorgan’s beat was wide enough to be one of its largest in recent history. Away from banks, Thursday’s rotation out of chipmakers found a landing spot in legacy tech names like IBM, seen as less exposed to the AI-capex debate that hammered semiconductors.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.