This week’s stock shocks as of 13th February, 2026

Wall Street’s growth-to-value rotation deepens amid AI disruption fears

The S&P 500 fell roughly 1.4% through Thursday, February 12, 2026, as a sharp Thursday selloff erased early-week gains and cemented the most dramatic growth-to-value rotation in years. The catalyst: escalating fears that AI tools will disrupt not just software but real estate, logistics, and financial services — triggering capital flight from mega-cap tech into “old economy” sectors like energy, materials, and industrials. The week also delivered a stronger-than-expected January jobs report (+130,000 vs. ~70,000 consensus), plunging existing home sales (-8.4%), and a highly anticipated CPI release on Friday morning. Treasury yields whipsawed, with the 10-year falling toward the low 4% range by Thursday’s close, while the VIX spiked above 20 for the first time in weeks.

This wasn’t a week of broad selloffs or blind panic. It was a market making sharp distinctions — rewarding AI infrastructure winners while punishing anyone on the wrong side of the disruption trade. Micron exploded higher. Cisco imploded. Applied Materials crushed it. Apple couldn’t catch a break. The message is clear: in 2026, the AI trade cuts both ways, and which side you’re on makes all the difference.

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Market recap 📊

Thursday’s rout dominates the tape

The week’s price action told a story in three acts: hope, shock, and recalibration.

Monday and Tuesday were about recovery and positioning. The S&P 500 climbed steadily, with the Dow posting record closes on both sessions — extending the historic streak that began after first crossing 50,000 on February 6. Tech rebounded on Monday (+0.90% Nasdaq), and the mood was cautiously optimistic heading into the jobs data.

Wednesday brought the jobs bombshell. Nonfarm payrolls surged +130,000, nearly double the ~70,000 consensus. The unemployment rate ticked down to 4.3%. The initial reaction was positive — energy, materials, and staples rallied — but gains faded by the close as investors digested the implications for rate cuts. The Dow snapped a three-session win streak, falling more than 50 points. Micron jumped around 10% after Morgan Stanley raised its price target to $450.

Thursday was the reckoning. The S&P 500 cratered 1.57% — its worst session in weeks. The Nasdaq shed 2.03%. Cisco’s 12% plunge after a guidance miss dragged networking and enterprise tech lower. Apple fell 5% on a triple blow of Siri delays, an FTC warning letter, and the broader tech rout. But here’s what made this week fascinating: the Dow’s 1.34% drop was less severe than the Nasdaq’s, and defensive names like McDonald’s (+2.7%) and Walmart (+3.8%) actually gained on the day. The rotation was surgical.

By Friday, markets digested the January CPI print (headline 2.5% YoY, core 2.6%) and attempted to stabilise. The message was unmistakable: the market rewards AI infrastructure and punishes everything else.

Daily breakdown for the week:

The S&P 500 Equal Weight Index continued hitting fresh all-time highs even as the cap-weighted S&P 500 struggled — a clear signal that the average stock is performing far better than the mega-cap-dominated headline index.

Sentiment watch: Fear creeps back in 😶🌫️

Sentiment indicators spent the week fighting gravity — and lost.

The CNN Fear & Greed Index dropped to approximately 37 (Fear) by Thursday, sliding 11 points from a reading of 48 (Neutral) earlier in the week. The index remained in the “Neutral” zone on Wednesday before Thursday’s selloff pushed it firmly back into Fear territory. One month ago, the index sat in the Neutral-to-Greed range (~50–60) before the late-January selloff began the deterioration.

Supporting sentiment data paints a cautious picture. The AAII Investor Sentiment Survey showed bullish sentiment near historical averages but down from the elevated readings of late 2025. The VIX spiked to 20.82 on Thursday (+18%), crossing above the psychologically important 20 threshold for the first time in weeks. Crypto markets remained under severe pressure, with Bitcoin trading below $69,000 and the crypto Fear & Greed Index deep in Extreme Fear territory.

That tension is unstable. It’s a standoff waiting for a catalyst. Strong earnings from Walmart and Arista Networks next week could tip scales toward recovery. Another guidance miss from a bellwether flips it back to fear and triggers the next leg down.

What’s telling? Even as the Equal Weight Index hits records, institutions are hedging, not loading up. The market wants to go higher but knows the path is narrowing — and the AI disruption narrative is scrambling the old playbook.

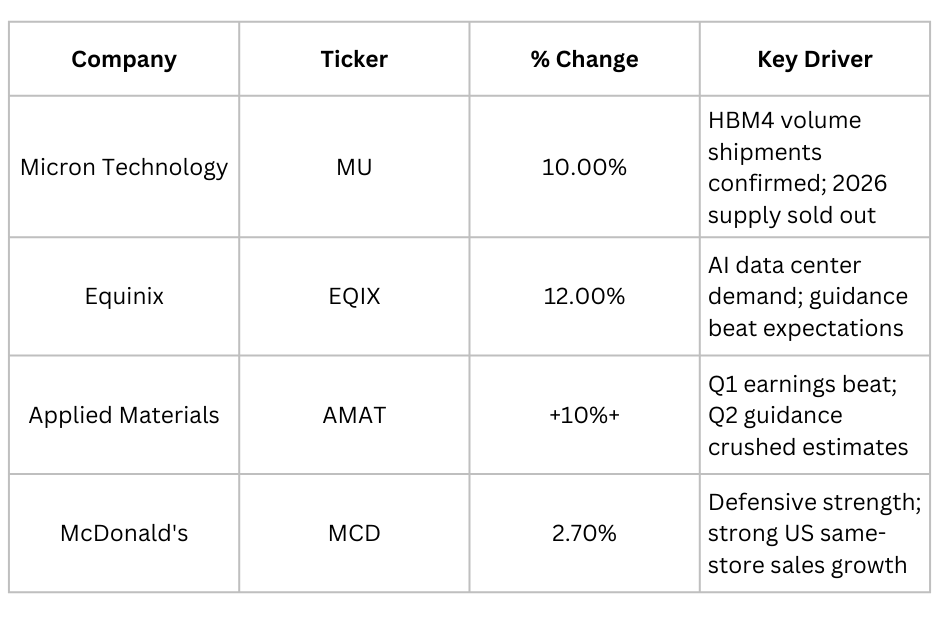

Best performers of the week 🏆

This was the week AI infrastructure names reminded everyone who’s really winning. While growth-to-value rotation punished mega-cap tech, companies building the actual AI backbone surged.

Micron Technology (MU) — up ~10%. CFO Mark Murphy confirmed at the Wolfe Research conference on Feb 11 that Micron has begun volume production and commercial shipments of next-generation HBM4 memory chips, dismissing reports of competitive struggles with Nvidia’s architecture. The company confirmed its entire HBM production for 2026 is already sold out. Morgan Stanley reportedly raised its price target to $450, with analysts citing expectations for EPS potentially reaching the low $50s in 2026. The stock closed at $410.34 on Tuesday before extending gains to $413.97 on Thursday. Memory is the new oil — and Micron controls the tap.

Equinix (EQIX) — up ~12%. The data center REIT delivered full-year 2026 guidance that exceeded Wall Street expectations, projecting mid-single-digit-billion-dollar adjusted EBITDA on record bookings driven by accelerating AI infrastructure demand. Management stated that demand for their solutions has never been higher. When a REIT rallies 12% in a week where real estate gets hammered, that tells you everything about how powerful the AI infrastructure tailwind is.

Applied Materials (AMAT) — up sharply in after-hours Thursday (reflected in Friday trading). The semiconductor equipment maker beat Q1 EPS and revenue estimates and issued Q2 revenue guidance that dramatically exceeded consensus. Management projected semiconductor equipment business growth in the range of 20% or more in calendar 2026, driven by AI chip demand. AMAT is the arms dealer of the AI chip war — and business is booming.

McDonald’s (MCD) — up ~2.7%. In a market that punished growth stocks, McDonald’s stood out as a defensive winner. Q4 US same-store sales showed strong mid-to-high-single-digit year-over-year growth as value meals resonated with cost-conscious consumers. The stock gained on Thursday while virtually everything else fell. When the world is burning, people still eat Big Macs.

Honourable mention: Crocs (CROX) surged on an earnings beat and strong 2026 guidance. Fastly (FSLY), while technically a mid-cap, delivered the week’s most spectacular move on a blowout quarter.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.