The new Fed chair and what it means for your money

Most investors watch every Fed announcement without understanding what actually just changed. On May 22, 2026, the Federal Reserve got its 17th chair: Kevin Warsh, a hawkish former Fed governor handpicked by Trump, stepping into the role as inflation sits above 3%, the FOMC is the most divided it has been since 1992, and the first rate decision under his watch lands on June 17 — six days from now.

The mechanics of how the Fed works, how a chair transition actually moves markets, and what the Warsh era means for your US equity returns — that’s what this issue breaks down. That’s why we built Winvesta Crisps, to break down what’s actually moving markets, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Six days from now, Kevin Warsh will chair his first Federal Open Market Committee meeting. Markets aren’t expecting a rate move — CME FedWatch data puts the probability of a June cut at under 5%. But the rate decision is almost beside the point. What traders, analysts, and every investor holding US equities will be watching is something harder to quantify: whether Warsh signals a genuine shift in how the world’s most powerful central bank operates, or whether he stays close to the playbook his predecessor left behind.

The stakes are real. The Fed’s current rate stance — held at 3.50% to 3.75% across three consecutive meetings in January, March, and April 2026 — sits against a backdrop of inflation still running above the Fed’s 2% target, an oil-fuelled price surge from Middle East tensions, and a US president who has been publicly demanding rate cuts while saying, at the same ceremony where he watched Warsh take his oath, “You get the interest rates down, everybody’s going to be very, very happy.”

That tension — between an institution designed to be independent and a White House that wants cheaper money — is the thread running through everything that happens next. To understand it, you first need to understand how the Fed actually works.

What the Federal Reserve is and why it controls your portfolio 🏦

The Federal Reserve is the central bank of the United States, created by Congress in 1913 after a series of bank panics revealed the dangers of having no lender of last resort. Its primary tools for managing the economy are setting short-term interest rates and controlling the money supply — and the downstream effects of those decisions touch every asset class on earth.

The key decision-making body is the Federal Open Market Committee, or FOMC. It consists of 12 voting members: the seven governors of the Federal Reserve Board (appointed by the President, confirmed by the Senate), the president of the New York Fed (who always votes), and four rotating seats filled by the presidents of the other 11 regional Federal Reserve banks. The full committee of 19 participants — all governors plus all 12 regional bank presidents — provides input; 12 of them vote.

The FOMC meets eight times a year. After each meeting, it releases a policy statement. Four of those meetings per year also include a Summary of Economic Projections (SEP) — which is where the famous “dot plot” comes from.

The dot plot, demystified. Each of the 19 FOMC participants anonymously places a dot on a chart indicating where they believe the federal funds rate should be at the end of each of the next three years, plus the “longer run.” The dot plot shows the full distribution of views — and markets obsess over the median dot as a signal for where rates are heading. Former Fed Chair Jerome Powell himself said, “the dots are not a great forecaster of future rate moves overall,” but markets price off them anyway.

The June 17 meeting includes a full dot plot and a press conference. It is the first time under Warsh that markets will see the committee’s rate outlook shift.

Why does the fed funds rate matter? When the Fed raises the overnight rate at which banks lend to each other, borrowing costs ripple through the entire economy: mortgage rates, corporate loans, credit card rates, and the discount rate used to value future earnings. Higher rates mean future earnings are worth less in present-value terms — which is why rate hikes hit growth stocks harder than dividend-paying ones. Lower rates do the reverse.

For global investors, the Fed funds rate also drives capital flows. When US rates are high relative to other countries, dollar assets become more attractive to global investors, the dollar strengthens, and capital flows out of emerging markets into US Treasuries. When US rates fall, the dynamic reverses.

Who Kevin Warsh is and why his appointment shook markets 👤

Kevin Warsh is 56 years old and became a Fed governor at 35 — the youngest person ever appointed to the Fed’s Board of Governors. He served from 2006 to 2011, sitting through the entire 2008 financial crisis alongside Ben Bernanke. During that period, he was known as a hawk: sceptical of quantitative easing, worried about inflation risks even as others around him focused on unemployment, and willing to push back on the consensus view.

He left the Fed in 2011, spent years at the Hoover Institution at Stanford, worked in finance at Morgan Stanley and the hedge fund Duquesne Capital, and became a persistent critic of what he viewed as the Fed’s excessive reliance on bond purchases and its slow response to post-pandemic inflation.

When Trump nominated him on January 30, 2026, to succeed Jerome Powell, markets reacted instantly. Gold dropped roughly 11% in a single day as investors priced in a potentially more hawkish rate path. The dollar rallied. The bond market repriced. That single-session reaction tells you how much weight markets place on the identity of whoever sits in that chair.

Since then, the picture has become more nuanced. During his Senate confirmation hearings, Warsh appeared more measured than his hawkish reputation suggested. He expressed openness to rate cuts if warranted, argued that monetary policy needs to be “forward-looking” given the 6-to-12-month lag between rate decisions and their economic effects, and signalled interest in AI-driven productivity gains as a potential disinflationary force that the Fed should weigh carefully.

On the balance sheet — the $6.5-plus trillion in assets the Fed holds from years of bond purchases — he is more consistently hawkish, advocating for a gradual but deliberate reduction over time. He was confirmed by the Senate 54-45, the closest vote in the modern era, and sworn in at the White House on May 22 — the first Fed chair sworn in there since Alan Greenspan in 1987.

The short version: Warsh is not a simple “Trump will get his rate cuts” story. He is a genuinely complex figure whose actual policy path will reveal itself over months, not weeks.

How a Fed chair transition actually moves markets 📈

The Fed chair does not unilaterally set rates. That is a consensus decision of 12 voting FOMC members. But the chair’s influence over monetary policy is still profound — through the power to set agendas, shape the committee’s communication, convene informal pre-meeting conversations that align views before votes happen, and control the tone of the public press conference that follows every decision.

The best way to understand a chair transition’s market impact is to look at what changed when previous chairs took over.

Paul Volcker (1979): Inherited an economy with inflation running above 14%. Took rates to nearly 20% and deliberately caused the worst recession since the 1930s to break inflation’s back. Unemployment hit nearly 11%. Markets collapsed. Inflation fell from above 14% to under 3% in three brutal years. His willingness to cause short-term pain for long-term credibility is still the reference point for what central bank independence actually looks like under pressure.

Alan Greenspan (1987): Took over two months before Black Monday. Navigated the 1987 crash with emergency liquidity, setting the pattern of the “Fed put” — the idea that the central bank will backstop markets during severe stress. His 18 years in the chair saw the longest peacetime expansion in US history, though critics argue he kept rates too low for too long and set the conditions for the 2008 crisis.

Ben Bernanke (2006): A Depression scholar who had written extensively about what central banks should do in a financial crisis — and then had to live it in 2008. His deployment of quantitative easing (buying trillions of dollars in bonds to push down long-term rates when short-term rates hit zero) was unprecedented. His Nobel Prize in Economics in 2022 was awarded partly for this work.

Janet Yellen (2014): Oversaw the painstaking normalisation of monetary policy after the crisis — gradually raising rates from near zero without triggering another recession. Markets rewarded her methodical approach: investors earned solid annual returns during her four-year tenure.

Jerome Powell (2018): Raised rates sharply from 2022 to 2023 to fight post-pandemic inflation — the fastest tightening cycle in decades — then cut carefully when inflation cooled. He was simultaneously praised for the “soft landing” and criticised by Trump for not moving faster on cuts. His tenure ended with inflation still above target and the FOMC the most divided it had been in a generation.

What the pattern shows: Chair transitions matter most not when the policy framework is stable, but when there is a genuine question about the Fed’s direction. Right now, that question is wide open: Will Warsh cut when Trump wants him to, or will he prioritise inflation credibility over White House approval? History suggests the chair who makes the former choice tends to be remembered poorly; the one who makes the latter tends to be remembered well — but usually only after a difficult period.

The dynamics covered in this article affect every US stock in your portfolio. Trade from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

The Trump-Fed tension and what it does to markets 🔥

Trump has never been subtle about what he wants from the Fed. During his first term, he publicly attacked Jerome Powell for raising rates, calling him an “enemy” and arguing the Fed should cut to zero. In this term, he has been more explicit: he has said he understands the economy “better than almost anybody” and that he wants rates at 1% or lower. The federal funds rate currently sits at 3.50-3.75%.

At Warsh’s swearing-in ceremony on May 22, Trump said “I want Kevin to be totally independent.” At a rally the same day, he said: “You get the interest rates down, everybody’s going to be very, very happy.”

The Federal Reserve’s independence from political pressure is not just a technicality — it is the institutional bedrock that keeps inflation expectations anchored. Markets trust that the Fed will raise rates when needed to fight inflation, even when it is politically painful, because independent central banks have historically been more credible inflation fighters than politically directed ones.

When that independence is questioned, two things happen. First, long-term inflation expectations drift upward — bond investors demand higher yields to compensate for the risk that the Fed becomes too accommodating. Second, the dollar weakens because a central bank that bends to political pressure is seen as less committed to preserving the currency’s purchasing power.

Jerome Powell — in his acceptance speech for the JFK Profile in Courage Award on May 31, just days before his formal departure — referenced what he called a “stress test” for the Fed, widely interpreted as a reference to the institutional pressure the central bank is navigating.

Warsh has consistently said during his confirmation process that he will not set policy based on Trump’s preferences. His hawkish instincts from his previous stint at the Fed are well-documented. But markets are watching whether those words hold once the political pressure becomes live, which it already has.

The April FOMC meeting — Powell’s last as chair — produced four dissents: the most divided committee since 1992. Three of those dissents came from members who opposed even the existing “easing bias” statement as too dovish, given rising inflation. Warsh inherits a fractured committee that will take genuine leadership to manage.

Here is what recent market consensus reflects: futures markets currently price less than a 10% chance of a rate cut at any of the remaining 2026 FOMC meetings. A growing minority of investors now sees a rate hike before year-end as possible, depending on the inflation trajectory.

Illustrative framework. Not investment advice. Actual outcomes depend on data, policy execution, and market positioning.

What this means for Indian investors holding US equities 🇮🇳

For Indian investors in US markets through platforms like Winvesta, the Warsh transition is not a distant macro story. It runs directly through the rupee-dollar rate, foreign capital flows into India, the valuations of your US equity holdings, and the performance of Indian domestic stocks tied to US corporate spending.

The rate-rupee-returns chain. When US rates are high relative to Indian rates, global capital has an incentive to stay in dollar assets — which pressures the rupee. India’s 10-year government bond yield currently sits around 6.6-6.7%, while the US equivalent has been trading in the 4.3-4.5% range. That differential is narrower than it was at the peak of the 2022-2023 tightening cycle, but it still attracts capital to the dollar. If Warsh stays hawkish and keeps US rates elevated, the rupee faces continued pressure. A weaker rupee directly compresses your US equity returns when you eventually convert back to INR.

The FII flow effect on Indian markets. Higher US rates pull foreign portfolio investors out of Indian equities and into US Treasuries. When the Fed raised rates aggressively from 2022 to 2023, Indian markets saw over Rs 1.2 trillion in FPI outflows. The reverse is also true: when US rates fall, emerging-market destinations like India become more attractive for global capital, supporting Indian equity markets. Warsh holding rates firm means this relief does not come soon.

Your US portfolio directly. A hawkish Fed that keeps rates elevated is bad news for high-multiple growth stocks — especially the large-cap technology names that dominate broad US index funds. Rate-sensitive sectors like real estate, utilities, and consumer discretionary also face valuation pressure when rates stay high. If you are heavily weighted in a broad S&P 500 ETF, you have meaningful exposure to names whose valuations are built on expectations of eventually lower rates.

Defensives fare better: healthcare, consumer staples, energy stocks — sectors whose earnings do not depend as heavily on cheap borrowing or stretched forward multiples.

Indian IT, again. The channel that runs from Fed policy through US corporate capex to Indian IT order books is well-established: higher rates pressure corporate margins and technology spending budgets, which shows up in the guidance of Indian IT services companies with large US client bases. The Nifty IT index has been under pressure through 2026 as both AI substitution risk and tighter US corporate budgets compound. A hawkish Fed that keeps rates elevated prolongs the second of those pressures.

Gold. If the Trump-Warsh tension raises doubts about Fed independence and long-term inflation credibility, gold benefits. Gold has historically performed well when real yields are low or negative, and when inflation expectations drift upward. The January 30 nomination announcement saw gold crash 11% as markets priced in a hawkish Fed that would keep real rates positive. If Warsh turns out to be more dovish than feared — or if political pressure appears to be bending his decisions — the gold trade reverses sharply.

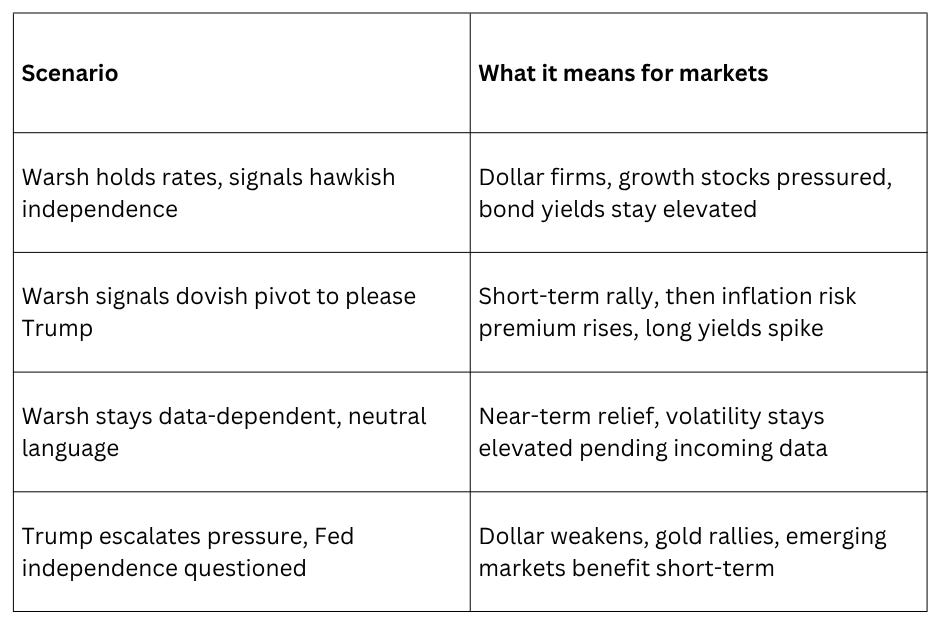

What to watch on June 17 and beyond 🧭

The June 17 meeting will not be remembered for the rate decision — almost nobody expects a move. It will be remembered for what Warsh signals about the institution he now leads.

The policy statement language. The April statement included an “easing bias” — language implying the next move is more likely a cut than a hike. Three of the four dissenters at that meeting opposed that language explicitly. Warsh is widely expected to drop the easing bias at the June meeting, shifting to a neutral stance. That alone tells markets that cuts are not on the near-term horizon and resets expectations.

The dot plot median. The March dot plot showed the median FOMC participant expecting two rate cuts in 2026. If the June dot plot’s median moves to one cut or zero, that is a hawkish surprise with real market consequences. Watch for whether the distribution of dots clusters around “hold for longer” or starts showing upside risk (dots above current rates), which would signal some committee members are seriously entertaining a hike.

Warsh’s press conference tone. This is the first time markets will hear Warsh speak as chair in a live policy context. His predecessors all had a signature communication style: Volcker was blunt to the point of discomfort; Greenspan was famously opaque (”If I seem unduly clear to you, you must have misunderstood me”); Bernanke introduced unprecedented transparency; Yellen was methodical; Powell was plain-spoken and deft at managing market expectations. Warsh has reportedly been contemplating withholding his own dot from the June plot — a reform-minded move that would signal a different approach to forward guidance. How he runs the press conference will define early market perceptions of his tenure.

Incoming inflation data. One source cited consensus economist expectations for US CPI of around 6% for Q2 2026, driven partly by the Middle East oil shock. If those readings materialise as expected, the case for cuts collapses entirely and the June meeting is a foregone conclusion. Watch the May CPI release (due before June 17) closely — it is the single data point most likely to shift the meeting’s market interpretation before the decision.

The Trump-Warsh relationship going forward. The first test of whether Warsh will resist political pressure on rates will come when Trump publicly criticises a decision, which, given the pattern, is likely by September at the latest. How Warsh responds, and whether the Fed’s language in subsequent meetings reflects presidential preferences, will be the most important ongoing signal for whether the US central bank maintains credible independence.

If this changed how you see the Fed’s role in your portfolio, pass it on.

The bottom line 🏁

The Federal Reserve’s job is to keep inflation low and employment high. Its ability to do that job depends almost entirely on one thing: the belief that it will act in the interest of those mandates, not in the interest of whoever occupies the White House. Every time that belief has been tested — and it has been, repeatedly, throughout the Fed’s history — markets have ultimately rewarded the chairs who held the line and punished the institution when it appeared to bend.

Kevin Warsh steps into the chair at one of the more politically charged moments in Fed history. Inflation is above target, an oil shock is adding pressure, the FOMC is fractured, and a president who has been explicit about wanting lower rates is watching closely. Whether Warsh holds to the independent hawkishness of his confirmation hearings or gradually tilts toward accommodation is not yet known — and that uncertainty is itself a market variable.

For Indian investors holding US equities, the practical implications are direct. A hawkish Fed that keeps rates elevated means continued pressure on growth stock valuations, a strong dollar that compresses your rupee-denominated returns, and continued headwinds for Indian IT order books. A Fed that pivots dovishly — whether through genuine economic justification or political accommodation — would do the opposite: weaker dollar, capital rotating into emerging markets including India, growth stocks rebounding.

The June 17 meeting will not resolve this question. But it will give investors the first real signal. Pay less attention to whether rates move or not — they almost certainly won’t. Pay more attention to whether the easing bias is dropped, where the median dot lands, and how Warsh speaks in his press conference. Those three signals will tell you more about the next 12 months of Fed policy than any single rate decision.

By the numbers 📊

3.50%-3.75% — the federal funds rate as of April 2026, unchanged across three consecutive meetings; the starting point Warsh inherits

54-45 — Warsh’s Senate confirmation margin, the closest in the modern era, reflecting the political stakes of the appointment

May 22, 2026 — Warsh’s swearing-in date, the first Fed chair ceremony held at the White House since Alan Greenspan in 1987

4 dissents — the number of FOMC members who dissented at the April 2026 meeting, the most divided the committee has been since 1992

~11% — the single-day drop in gold prices when Warsh’s nomination was announced on January 30, 2026, as markets priced in a more hawkish rate path

~20% — the fed funds rate Paul Volcker reached in 1981 to break the back of double-digit inflation; the historical benchmark for what genuine central bank independence looks like under maximum political pressure

6-12 months — the approximate lag between Fed rate decisions and their full effect on the broader economy, per Warsh’s own confirmation hearing testimony; why forward-looking policy guidance matters as much as the actual rate decision

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.