The dollar’s dominance is being questioned, here’s why it matters for your portfolio

Investing in US stocks from India meant one thing: exposure to the world’s best companies. Today, it means something more complex—you’re also taking a view on the dollar, whether you realise it or not. The currency that denominates your returns is itself in the middle of a structural debate that could reshape global finance over the next decade.

That’s why we built Winvesta Crisps, to break down what’s actually moving the markets you’re invested in, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

For nearly 80 years, the US dollar has been the world’s default currency—the language of oil contracts, trade invoices, central bank reserves, and emergency bailouts. You didn’t think about it. It was just the way things worked.

That assumption is being tested in 2025 in ways that feel different from previous episodes. The dollar has weakened meaningfully against a basket of major currencies since the start of the year, central banks around the world have been quietly accumulating gold at a record pace, and a growing coalition of countries is actively building infrastructure to settle trade outside the dollar system. None of this is happening overnight. But the direction of travel is real—and for investors holding US assets from India, it has direct consequences for your returns, your risk, and how you think about currency as a variable in your portfolio.

How the dollar became the world’s reserve currency 🏛️

The dollar’s dominance didn’t happen by accident—it was designed.

In July 1944, with World War II still ongoing, representatives from 44 Allied nations gathered in Bretton Woods, New Hampshire. They agreed to peg their currencies to the US dollar, which would itself be convertible to gold at $35 per ounce. The US, which held the majority of the world’s gold reserves at the time and had emerged from the war with its industrial base intact, became the anchor of the global monetary system.

In 1971, President Nixon ended dollar-gold convertibility—the “Nixon Shock.” The dollar was no longer technically backed by gold, but its dominance was already structural. International oil contracts were priced in dollars. Trade finance was conducted in dollars. Central banks held dollars as reserves because everyone else did, and that self-reinforcing logic made the dollar hard to displace.

Today, the dollar still accounts for around 57–58% of global foreign exchange reserves, per IMF COFER data as of early 2025. It’s used in an estimated 40–50% of global trade invoicing—far more than the US’s actual share of global trade. And most commodity markets, from crude oil to gold to copper, are priced in dollars by default.

That’s the baseline. It’s a formidable position. But formidable doesn’t mean permanent.

What de-dollarisation actually means 🌍

De-dollarisation is not a single event. It’s a slow-moving structural shift in how countries, central banks, and businesses choose to store value and conduct trade—and it’s been building for over a decade.

The clearest signal has been central bank gold buying. Since around 2022, central banks globally have been purchasing gold at the highest pace in decades, per World Gold Council data. China, India, Poland, Turkey, and several Gulf states have all added meaningfully to their gold reserves. The motive is explicit in many cases: reducing dependence on dollar-denominated assets that, in theory, could be frozen or sanctioned.

The freezing of Russian central bank assets in 2022—following the invasion of Ukraine—accelerated this thinking dramatically. Countries that previously treated US Treasury holdings as simply a risk-free savings account suddenly saw them as a geopolitical instrument that could be turned off. Whether or not you agree with the policy, the signal to non-aligned nations was clear.

Bilateral trade in non-dollar currencies has also grown. China and Russia now settle the large majority of their bilateral trade in yuan and rubles. India and Russia explored rupee-rouble trade settlement for oil purchases, with mixed results. China has been expanding yuan-denominated oil contracts, particularly with Gulf producers.

The BRICS expansion is part of the same story. The grouping—Brazil, Russia, India, China, South Africa —now expanded to include Saudi Arabia, the UAE, Iran, Egypt, and Ethiopia—has explicitly discussed creating an alternative settlement mechanism. However, a formal BRICS currency remains distant and faces significant structural hurdles.

None of this means the dollar is about to be replaced. It doesn’t. But it does mean the dollar’s share of global reserves and trade finance has been declining at the margin—slowly, not sharply; IMF data adjusted for valuation effects show the USD share has been broadly stable in recent quarters, with the longer-run decline a gradual drift from the early 2000s rather than a 2020s leg down. The direction is real. The speed is slow.

Why the dollar is under pressure right now 📉

Structural de-dollarisation is a decade-long story. But the dollar’s more immediate weakness in 2025 has a few distinct near-term drivers worth separating.

Tariff-related uncertainty has done something counterintuitive: instead of strengthening the dollar as a haven—which is the typical pattern in times of global stress—the Liberation Day tariff shock weakened it. One explanation is that investors are pricing in damage to US economic growth and the credibility of US economic policy, per commentary from several major banks and financial news outlets. When confidence in the US as a reliable trade partner wobbles, so does confidence in its currency.

Fiscal trajectory is a slower-burn concern. The US is running structurally large budget deficits, and debt servicing costs have risen significantly as interest rates remain elevated. Investors who hold US Treasuries as the backbone of their reserve portfolio are watching the supply of dollar-denominated debt increase faster than natural demand can absorb it—which, at the margin, pushes yields up and the dollar’s appeal as a long-term store of value down.

Federal Reserve rate path matters too. If the Fed cuts rates more aggressively than other major central banks—such as the European Central Bank, the Bank of Japan, and the Reserve Bank of India—the interest rate differential that attracts capital to dollar assets narrows. Lower relative rates mean lower relative demand for the currency.

The US Dollar Index (DXY), which measures the dollar against a basket of major currencies, peaked in late 2022 and has traded below those highs since—but the move has been choppy rather than a clean downtrend, with the index rebounding toward the high-90s to around 100 by early 2026, per market data. The “weak dollar” story is real relative to the 2022 peak; it is not a straight-line decline.

Want to navigate currency shifts and invest in US markets directly from India? No US bank account needed.

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

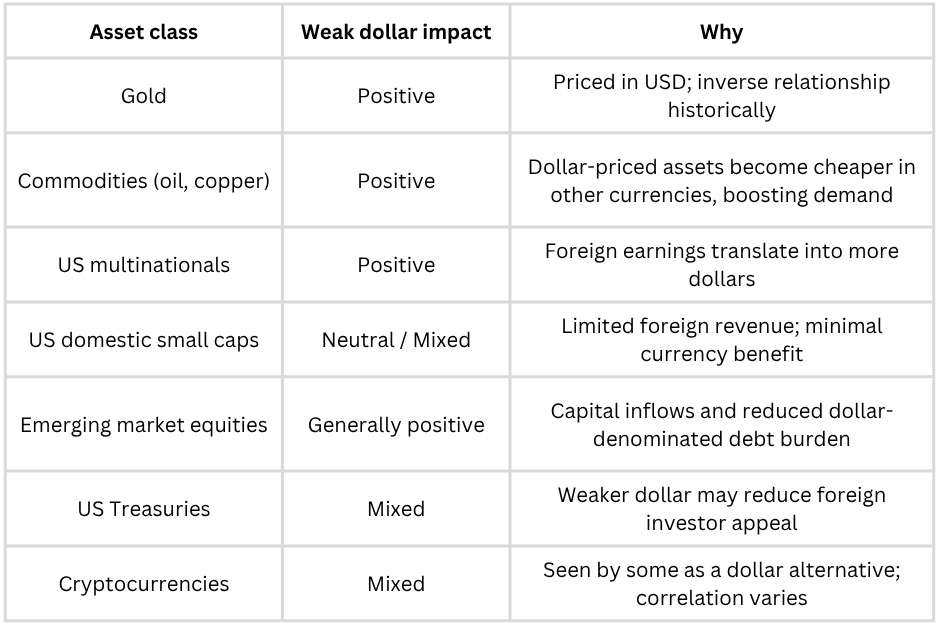

What a weaker dollar does to markets 📊

Currency moves don’t stay in the currency market. They ripple through equities, commodities, and global capital flows in ways that matter to portfolio positioning.

Commodities rise in dollar terms. Since most commodities are priced in dollars, a weaker dollar means the same barrel of oil or ounce of gold costs more dollars to buy. Gold has been one of the standout performers in 2025, partly driven by this dynamic, on top of safe-haven demand amid geopolitical uncertainty. Energy and metals tend to benefit in dollar-weakening environments.

US multinationals see a translation tailwind. Companies that earn significant revenue outside the US—think large-cap tech, pharma, consumer staples—translate foreign earnings back into dollars when they report. A weaker dollar makes those foreign earnings worth more in the reported figures. This is one reason some analysts have argued the earnings impact of a weak dollar partially offsets the tariff headwinds for globally diversified US companies.

Emerging markets tend to benefit. A weaker dollar reduces the debt servicing burden for emerging market countries that borrowed in dollars. It also tends to push capital flows toward higher-yielding assets in developing economies, as the premium of sitting in dollar assets narrows. India, Brazil, and other emerging markets have historically outperformed during sustained dollar weakness cycles.

US domestic-focused companies face less tailwind. If a company earns and spends almost entirely in dollars, currency moves don’t help its earnings. The dollar weakness benefit is concentrated in globally exposed businesses.

Illustrative framework. Not investment advice. Actual outcomes depend on magnitude, pace, and accompanying macro conditions.

What this means if you’re investing in US stocks from India 🇮🇳

Here’s where it gets personal for investors like you.

When you buy US stocks from India, you’re converting rupees to dollars at today’s exchange rate. When you eventually sell, you convert back. The dollar’s movement during that holding period is a return variable you’re taking on—whether you’ve thought about it explicitly or not.

A weaker dollar reduces your rupee-denominated returns, even if your USD returns are positive. If you hold a US stock that rises 10% in dollar terms, but the dollar falls 5% against the rupee during that period, your actual return in rupees is closer to 5%. Currency drag is real, and in a sustained dollar-weakening cycle, it meaningfully compresses what you actually take home.

Conversely, a strong dollar has been a quiet return booster over the past decade. Much of the outperformance that Indian investors in US equities experienced in the 2010s and early 2020s was amplified by a gradually weakening rupee and strengthening dollar. That tailwind is not guaranteed going forward.

What this argues for is diversification within your US exposure. Holding some allocation in commodities (gold ETFs, for instance), or in US companies with heavy international revenue, means you’re not entirely reliant on dollar strength to generate rupee-denominated returns. It doesn’t mean abandoning US equities—it means being thoughtful about the currency dimension as a deliberate variable rather than an afterthought.

The rupee’s own dynamics matter too. A weaker dollar often brings capital into India’s equity and bond markets as investors seek emerging-market yields. That can support the rupee and partially offset the impact of dollar weakness on Indian investors—but the timing and magnitude are never guaranteed.

If this changed how you think about the currency dimension of your portfolio, share it with your investing circle.

How to think about your portfolio in a de-dollarisation world 🛡️

You don’t need to make sweeping changes. But a few frameworks help.

Don’t confuse structural and cyclical. The structural story—BRICS expansion, central bank gold buying, bilateral non-dollar trade—plays out over decades. The cyclical story—DXY weakness in 2025 driven by tariff uncertainty and Fed rate expectations—plays out over months. They’re related but distinct. Don’t panic about the structural story showing up in your quarterly returns, and don’t extrapolate the cyclical story into a permanent regime shift.

Gold deserves a look as a portfolio component. If central banks around the world are diversifying into gold as a dollar alternative, that’s a structural demand driver that’s been in place for several years and shows little sign of reversing. Gold doesn’t pay dividends, but it has historically performed well in dollar-weakening cycles and acts as a portfolio stabiliser during periods of macro uncertainty. Gold ETFs listed in the US are accessible through platforms like Winvesta.

Global diversification within equities is a feature, not a bug, right now—US companies with high international revenue exposure benefit from a weaker dollar. European equities, Japanese equities, and emerging market indices become more attractive in dollar terms when the dollar weakens. If your US equity exposure is entirely in domestic-focused names, you’re leaving one of the currency tailwinds on the table.

Watch the DXY as a leading indicator. The US Dollar Index is one of the cleaner real-time signals for the dollar’s direction. A sustained break below key levels tends to precede capital rotation into commodities and emerging markets—a useful heads-up for portfolio positioning rather than reactive scrambling.

Don’t over-rotate. The dollar’s reserve currency status, even if diminishing at the margin, is supported by the depth of US capital markets, the rule of law, and the sheer network effects of 80 years of financial infrastructure built around the dollar. De-dollarisation is happening. It is not happening fast. Positioning as if the dollar will collapse next quarter is a much bigger bet than the evidence supports.

The bottom line 🏁

The dollar isn’t going anywhere soon. But the world is quietly, steadily building alternatives—and the dollar’s share of global finance is declining at the margin in ways that matter to asset prices, capital flows, and the currency dimension of your investment returns.

For Indian investors in US markets, the practical implication isn’t to panic or abandon US equities. It’s to stop treating currency as a passive background variable and start thinking about it as an active component of your portfolio return. A weaker dollar means your dollar-denominated gains are worth less in rupees when you bring them home. It also means gold looks more interesting, emerging markets get a tailwind, and US multinationals with global revenue get a translation boost.

Understanding these dynamics doesn’t require a PhD in monetary economics. It requires asking one question every time you make a US investment: What’s my currency exposure here, and am I comfortable with it? That question alone puts you ahead of most retail investors who are still treating the dollar as a given.

By the numbers 📊

~57–58% — the dollar’s current share of global foreign exchange reserves, per IMF COFER data (2025 Q1), down from the low-70s in the early 2000s

~40–50% — share of global trade invoicing conducted in dollars, far above the US’s actual share of global trade

Record pace — central bank gold buying since 2022, per World Gold Council data, as countries diversify away from dollar-denominated reserves

1971 — the year Nixon ended dollar-gold convertibility, the last structural break in the dollar system before today’s debate

Several countries — joined or were invited to the BRICS grouping in its 2024 expansion (including Saudi Arabia, UAE, Iran, Egypt, Ethiopia), reflecting a broader push to build non-dollar trade and settlement infrastructure — though a BRICS currency remains speculative

Big one-day move — markets jumped when the 90-day tariff pause was announced, showing how quickly dollar-linked macro news can reprice everything

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.