The China factor: How US-China tensions are reshaping every portfolio

A spike in US-China tensions was a headline risk — something that caused a brief sell-off, then faded. Not anymore. Today’s decoupling is structural: export controls are rewiring the semiconductor industry, supply chains are physically relocating across continents, and the question of Taiwan sits permanently in the risk premium of every major tech stock.

That’s why we built Winvesta Crisps, to decode the geopolitical forces actually moving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

In April 2026, the US-China relationship is in a state that would have been hard to imagine a decade ago. Tariffs on Chinese goods have reached historically elevated levels — far above pre-2018 norms and among the highest in the post-war era — following what we at Winvesta call Liberation Day. Export controls on advanced semiconductors and chip-making equipment have progressively tightened. China has retaliated with its own restrictions on critical minerals, rare earths, and technology licences. The two largest economies on earth are not just in a trade dispute. They are engaged in a deliberate, multi-front effort to reduce dependence on each other — and that process is creating winners and losers across every sector of the US market in predictable ways, once you know what to look for.

How US-China became arguably the most consequential economic relationship on earth 🌏

The story of US-China economic integration is one of the great globalisation experiments of the modern era — and understanding why it’s unwinding requires understanding how deeply it was built.

Starting in the 1990s and accelerating after China joined the World Trade Organisation in 2001, US companies discovered something powerful: China offered a combination of low labour costs, improving infrastructure, a massive and rapidly expanding consumer market, and a government willing to attract foreign manufacturing. The result was a decades-long migration of manufacturing capacity — textiles, electronics, furniture, appliances, and ultimately semiconductors and advanced components — into Chinese factories.

By the mid-2010s, the integration was profound. Apple’s iPhones were designed in California and assembled in Zhengzhou. Walmart’s shelves were stocked substantially with Chinese-manufactured goods. US companies were generating significant revenue from Chinese consumers. And China’s growth model was, in turn, deeply dependent on access to US technology, US capital markets, and US consumer demand.

Both sides benefited enormously from this arrangement. Both also became dependent on it in ways that created strategic vulnerabilities — and it’s the recognition of those vulnerabilities, more than any single political decision, that is driving the current decoupling.

The shift didn’t happen overnight. The seeds were planted during the 2018–2019 trade war under the first Trump administration, accelerated through the COVID-19 pandemic (which exposed supply chain fragility), and then hardened dramatically in 2022 when the US imposed sweeping export controls on advanced semiconductor technology — and again in 2025 with Liberation Day’s tariff regime. Each escalation made the next one easier to justify, and harder to reverse.

The four fault lines reshaping the relationship right now 🔧

1. Tariffs and trade barriers

Following the renewed tariff escalation in 2025, US effective tariffs on Chinese goods reached multidecade highs by modern standards — well above pre-2018 levels, according to major economic research and index providers. China responded with its own retaliatory tariffs on US exports — agricultural products, aircraft, and industrial goods among the most affected. This isn’t just a cost story. It’s a structural signal: both governments are willing to accept near-term economic pain in exchange for reducing long-run dependency. That signal changes how companies plan their supply chains for the next decade, not just the next quarter.

2. Semiconductor export controls

This is arguably the most consequential front in the US-China technology conflict. The US has progressively tightened restrictions on the export of advanced semiconductors and the equipment used to manufacture them — particularly targeting chips that could accelerate China’s artificial intelligence and military capabilities. Companies like NVIDIA saw restrictions on certain chip sales to China tightened in successive rounds. The Netherlands, Japan, and other allies were brought into the framework, limiting China’s access to the most advanced chip-making equipment from global suppliers like ASML. China has responded by accelerating its own domestic semiconductor investment, though catching up at the cutting edge remains a multi-year challenge, per industry analysts.

3. Critical minerals and rare earths

China controls a dominant share of global rare-earth processing capacity, according to the US Geological Survey. In recent years, China has imposed and tightened export controls on several critical minerals and rare earth elements used in defence systems, electric vehicles, and semiconductor manufacturing — a direct counter to US technology export controls. This dependency on Chinese processing for materials critical to clean energy and advanced technology is one of the most underappreciated structural vulnerabilities in Western supply chains, and it’s now an active policy pressure point.

4. Taiwan

The geopolitical risk that sits underneath all of the above. Taiwan Semiconductor Manufacturing Company (TSMC) manufactures a dominant share of the world’s most advanced chips — those used in everything from smartphones to data centre AI accelerators. Taiwan’s political status and the risk of Chinese military action, therefore, are not abstract geopolitical concerns but direct tail risks embedded in the valuation of almost every major US technology company. Markets are not fully pricing this risk on most days — but it surfaces in volatility spikes whenever tensions escalate, which is why the US has been aggressively subsidising domestic semiconductor manufacturing through initiatives like the CHIPS Act.

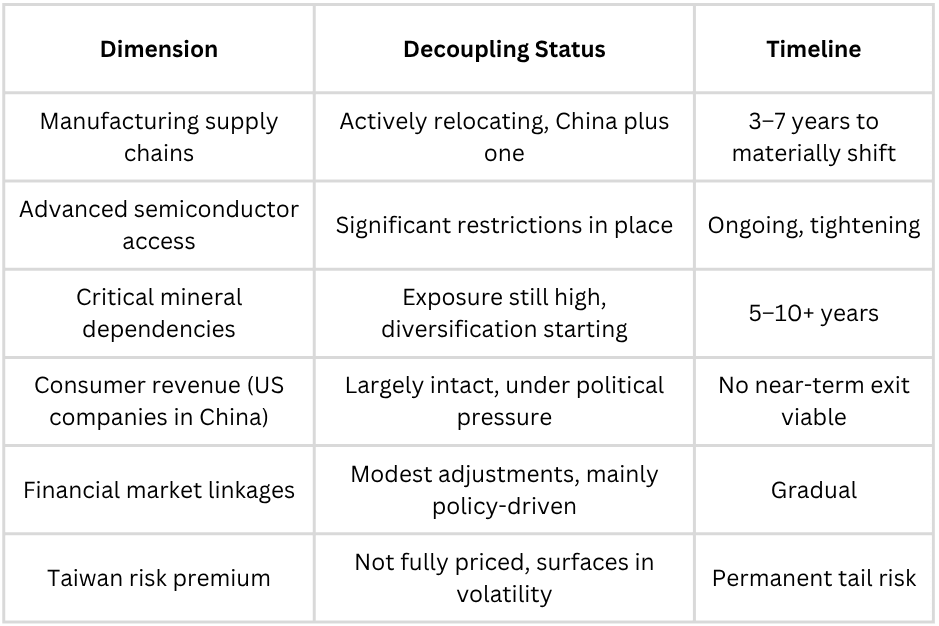

Decoupling: What’s actually happened, and what hasn’t 📊

“Decoupling” is a word that gets used loosely. The reality is more nuanced — in some areas, separation has moved fast; in others, it has barely begun.

Where decoupling is real and accelerating: Supply chain geography has shifted meaningfully. The phrase “China plus one” — maintaining some China operations while building parallel capacity elsewhere — went from strategy-deck buzzword to operational reality after the 2025 tariff escalation. Vietnam, India, and Mexico emerged as the primary beneficiaries of redirected investment, according to reports from the Financial Times and the Wall Street Journal. Apple accelerated iPhone production in India. Electronics and apparel brands moved sourcing across Southeast Asia. This physical relocation of production is slow and expensive, but it is happening.

Technology access has been materially restricted. Advanced semiconductor exports, certain software licences, and investment in specific Chinese technology sectors have been limited by US policy in ways that were unimaginable five years ago.

Where decoupling is slower than the headlines suggest: Consumer goods, lower-tech manufacturing, and commodity flows remain deeply interconnected. US retailers still source meaningfully from China for goods below the tariff sensitivity threshold. Many US companies still generate significant revenue from Chinese consumers — Apple, Starbucks, Nike, and others have large Chinese market exposures that they have no near-term ability or desire to exit. Full decoupling in these areas would require restructuring that would take years and cost, which would visibly hurt margins.

Financial market linkages remain substantial. Chinese companies listed on US exchanges (the ADR market), US institutional ownership of Chinese equities, and bilateral technology licensing arrangements haven’t been unwound at anything like the speed of the trade restrictions.

Directional framework. Individual company and sector outcomes vary.

🚀 Want to invest in US companies navigating the China-US reshaping? Trade US stocks and ETFs directly from India on the Winvesta app — no US bank account needed!

Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Winners and losers: The sector map 🏆

US-China decoupling doesn’t affect all sectors equally. Understanding the exposure map is one of the most practical things an investor can do in this environment.

Sectors under meaningful pressure

Technology hardware and semiconductors carry the most acute exposure — both from direct export control restrictions and from supply chain complexity. Companies reliant on Chinese manufacturing or Chinese customer revenue face a structural drag that doesn’t resolve quickly. The restriction on selling advanced AI chips into China is a direct revenue constraint for companies at the frontier of that market.

Consumer discretionary brands with heavy revenue in China — apparel, luxury goods, and consumer electronics — face a more complex picture. Their Chinese consumer business is valuable and hard to replace. Still, it is increasingly subject to political risk on both sides: US policy pressure and Chinese consumer nationalism, which has periodically shifted domestic buyers toward Chinese alternatives.

Automotive companies operating global supply chains face tariff pressure on both imported vehicles and components, as well as competitive pressure in the Chinese EV market, where domestic players have moved aggressively.

Sectors with structural tailwinds

Domestic US manufacturers and defence-adjacent industrials benefit from both the reshoring narrative and government investment in supply chain resilience. Companies involved in domestic chip fabrication, defence electronics, and strategic materials processing are in an unusual sweet spot, with policy and economics pointing in the same direction.

Contract manufacturers and logistics companies facilitating the “China plus one” transition — building factories in Vietnam, India, and Mexico, moving goods through new trade routes — are direct beneficiaries of the supply chain reorganisation.

Semiconductor equipment companies not subject to China restrictions (and those successfully pivoting away from China revenue) have seen demand from new fabs being built in the US, Japan, and Europe under government-backed programmes.

The nuanced middle

Most large US multinationals don’t sit cleanly in “winner” or “loser” — they’re managing a complex balancing act. A company like Apple is simultaneously moving production to India (a China-plus-one move that reflects decoupling) while trying to protect its significant revenue from Chinese consumers (a reason to avoid fully decoupling). How companies navigate this tension — and how much of the eventual cost they can pass to consumers or absorb in margins — is where the differentiation lies.

The India angle: Threat, opportunity, or both? 🇮🇳

For Indian investors holding US equities through platforms like Winvesta, the US-China story adds a layer of complexity beyond portfolio positioning.

India is a manufacturing beneficiary. India has been one of the primary destinations for capital for supply chain diversification. Apple’s accelerated iPhone production ramp in India — through Foxconn and Tata — is the most prominent example, but electronics, textiles, pharmaceuticals, and industrial components are all seeing investment redirected from China into India. This is a structural tailwind for Indian manufacturing, employment, and GDP — and it shows up in the earnings of Indian IT and industrial companies that service these transitions.

The Indian IT services connection. India’s listed IT sector — Infosys, TCS, Wipro, and others — generates a substantial share of revenue from US corporate clients. When US companies tighten technology capex due to tariff uncertainty or US-China friction affecting their own margins, Indian IT order books feel it. Liberation Day’s disruption to US corporate planning showed this channel clearly. It’s a reason why US-China macro stress reaches Indian domestic markets through earnings, not just portfolio outflows.

India’s own tariff exposure. India navigated earlier rounds of US tariffs with lower direct exposure than China or Vietnam. In recent years, however, some Indian export categories have faced higher US tariffs or greater trade scrutiny than before. Indian pharmaceutical and textile exporters carry greater direct exposure than IT services, which largely escapes goods-tariff frameworks. Understanding this distinction matters for investors who hold both US equities and Indian domestic names.

The currency and capital flow dimension. When US-China tensions spike, and emerging-market risk aversion rises, India often experiences portfolio outflows alongside other EM destinations — even when India itself is a structural beneficiary of the realignment. The short-term and long-term effects can point in opposite directions. The discipline is knowing which timeframe you’re reacting to.

What to watch: The signals that actually matter 🧭

Investors who track US-China dynamics effectively don’t watch every headline. They watch for specific signals that tend to move the needle.

Tariff escalation or de-escalation. New tariff announcements — or exemption lists or bilateral negotiation signals — still sharply affect affected sectors. Having a basic tracking habit for trade policy announcements saves you from reactive scrambling.

Export control tightening. When the US Commerce Department adds companies to the entity list or announces new restrictions on chip sales to China, the impact on semiconductor earnings estimates needs to be re-run. These are often priced in advance of time, based on industry commentary, so watching earnings call guidance from semiconductor companies is a useful leading indicator.

Critical mineral supply disruptions. Chinese restrictions on rare-earth or mineral exports can move materials and defence-sector stocks sharply.

Corporate guidance language. Every earnings season, listen carefully to what management teams at companies with significant China exposure say about revenue outlook, supply chain costs, and their “China plus one” progress. The guidance language tells you more about how decoupling is actually landing than the headline trade data.

Taiwan's geopolitical temperature. Military exercises, political statements, and US arms sales to Taiwan are the leading indicators for the tail risk premium. When tensions spike, technology stocks with Taiwan supply chain dependency see elevated volatility — and gold tends to benefit, as covered in the broader geopolitical risk context.

If this changed how you see the geopolitical dimension of your US portfolio, share it with your investing circle.

Common mistakes investors make with China risk ⚠️

Treating “US tech” as a homogeneous China exposure. A cloud software company generating 95% of its revenue domestically in the US has almost no exposure in China. A hardware manufacturer with China-assembled products and Chinese consumer revenue has enormous exposure. Lumping them together under “tech” produces poor risk assessments and poor portfolio decisions.

Assuming decoupling happens fast. The political rhetoric of “decoupling” moves faster than actual supply chains do. Building a factory, training a workforce, qualifying a new supplier, and shipping products through new logistics routes takes years. Companies that announce “China plus one” strategies in 2024 are still executing them in 2027. Don’t price in the outcome before the transition is complete.

Ignoring the China revenue side of US companies. Most coverage focuses on China as a sourcing risk, where goods are made. The revenue risk — how much US companies sell to Chinese consumers — is equally important and often less discussed. A company that shifts manufacturing out of China but still derives 20% of its revenue from Chinese consumers remains significantly exposed to China.

Over-reacting to every bilateral headline. US-China tensions produce a constant flow of headlines that often move stocks intraday but have little long-run impact on earnings. The discipline is distinguishing policy changes with structural earnings consequences — such as new export controls and permanent tariff levels — from the diplomatic noise that surrounds them.

Assuming India captures all of China’s lost manufacturing. India is a meaningful beneficiary of supply chain diversification, but so are Vietnam, Mexico, and increasingly Southeast Asian economies. The “China to India” thesis is directionally correct but overstated if taken as a simple substitution story. India benefits significantly but competes for those flows.

The bottom line 🏁

US-China decoupling is not a political story with occasional market implications. It is a structural economic reorganisation that is actively reshaping supply chains, access to technology, corporate earnings, and geopolitical risk premiums across the entire US equity market.

For investors, the practical edge isn’t picking a side in the geopolitical argument — it’s understanding the exposure map of what you own. Which companies are net beneficiaries of reshoring and domestic investment? Which carry structural headwinds from losing China market access or facing higher input costs? Which are managing a transition that will take years and compress margins along the way?

The investors who did that analysis coming into Liberation Day were positioned to act when others were scrambling. The same analysis is just as relevant today — because the structural forces driving US-China decoupling haven’t reversed. They’ve deepened.

Understanding that isn’t pessimism. It’s the kind of informed positioning that turns macro disruption into a portfolio opportunity.

By the numbers 📊

Historically elevated — US effective tariff rates on Chinese goods remain far above pre-2018 norms and at some of the highest levels in the post-war era, per major economic research and index providers.

Dominant share — China’s control of global rare earth processing capacity, per the US Geological Survey; a structural dependency that has become an active geopolitical lever

China plus one — the supply chain strategy is now standard boardroom practice; Vietnam, India, and Mexico are the primary beneficiaries of manufacturing investment redirected from China.

Years, not quarters — the realistic timeline for meaningful supply chain relocation; companies announcing “China plus one” in 2024 are executing through 2027 and beyond

Both sides — US companies simultaneously face China as a supply chain risk (where they make things) and a revenue risk (where they sell things); both dimensions need to be tracked separately.

Taiwan — a permanent tail risk embedded in the valuation of every major US technology company with advanced semiconductor dependencies; not fully priced on most days, but surfaces in every escalation spike

All figures are directional. Individual company and sector outcomes vary based on specific exposure.

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.