The AI bubble debate: correction, or the beginning of the end?

Most investors have spent the past two weeks watching the Nasdaq swing wildly without understanding the specific financial structure that’s actually being questioned underneath it. A small group of companies has built a web of deals worth hundreds of billions of dollars, where chipmakers fund AI labs, AI labs spend that money on cloud capacity, and cloud providers spend it on chips again, with the same dollar counted as revenue at every stop along the way. Last week, Wall Street started asking out loud whether that revenue is as real as it looks. That’s why we built Winvesta Crisps, to break down what’s actually moving markets, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

On June 24, the Nasdaq fell 2.2% in a single session, South Korea’s Kospi crashed 10% and tripped its first trading halt since March, and chip stocks from Seoul to Santa Clara had their worst day in months. Five trading sessions later, the same Nasdaq closed up more than 2%, the Dow broke 52,000 for the first time in its history, and the same chip stocks were leading the rally. Same stocks, same week, opposite story.

That whiplash is the AI bubble debate playing out in real time. Four or five companies are on track to spend somewhere between $450 billion and $700 billion this year alone on chips, data centres and power, depending on which companies you count and whose estimate you use, and every version of that number is larger than what most countries spend running their entire energy sector. A meaningful share of that spending moves through deals where the same dollar shows up as revenue at two or three different companies on its way around a loop. Whether that loop reflects real demand or something closer to financial sleight of hand is now the single most consequential question for anyone holding a US index fund, and most people holding one have never thought about it.

How four companies built a financing web nobody fully understands 🏗️

When we wrote about this AI capex story back in May, the major hyperscalers were on track to spend roughly $600 to $700 billion combined in 2026, nearly tripling the roughly $162 billion the five biggest cloud companies spent in 2022. Two months and one Q1 earnings season later, that range has mostly held. Narrower estimates centred on the core four companies, Alphabet, Amazon, Meta and Microsoft, sit closer to $450 billion. Broader ones that include Oracle’s cloud arm push past $700 billion. Either way, the spending itself hasn’t slowed. Alphabet guided to $175-$185 billion in 2026 capex, roughly double what it spent in 2025. Amazon flagged around $200 billion.

For a while, the market mostly applauded the spending. Then the cash flow numbers started catching up with it. Alphabet’s free cash flow fell 47% year on year to around $10 billion in the first quarter. Amazon’s trailing twelve-month free cash flow collapsed by roughly 95% to about $1.2 billion. Spending kept rising. The cash actually coming back in fell fast.

That tension came to a head in June for two separate reasons that compounded each other. On June 17, the Federal Reserve held its benchmark rate at 3.5 to 3.75%, the first meeting under new chair Kevin Warsh, and revised its year-end rate projection up to 3.8% from 3.4% in March, signalling that roughly half the committee now sees a hike as more likely than a cut. Higher rates raise the discount applied to any company whose value depends on profits arriving years from now, which describes most of the AI trade. A week later, the AI-specific selloff hit. On June 24, the Nasdaq fell 2.2%, the Kospi fell 10% and triggered a trading halt, SK Hynix and Samsung each lost more than 12%, the newly listed SpaceX fell 16%, and Japan’s SoftBank, which holds a sizeable stake in OpenAI, fell 15% in a single session.

The proximate trigger was a report that OpenAI, the company sitting at the centre of almost every one of these financing deals, was leaning toward delaying its own IPO from 2026 to 2027. OpenAI’s bankers had watched SpaceX rally hard on its debut and then slide, and worried that retail enthusiasm for a second mega-cap tech listing in the same year might not show up twice. If the company anchoring the entire web of AI financing commitments is getting cold feet about its own valuation in public markets, that’s a meaningful data point, whichever way you read it.

Inside the loop, everyone is suddenly asking about 🔁

Strip away the jargon and the mechanism is simple. A chipmaker or cloud provider invests cash into an AI lab. The AI lab spends that cash buying chips or cloud capacity from the same investor, or from a tightly linked group of two or three companies. Each company in the loop can count the transaction as revenue or as contracted backlog. The same dollar effectively gets counted multiple times across multiple income statements, even though only one dollar of new cash ever entered the system.

The specific deals add up fast. Nvidia has agreed to supply OpenAI with 10 gigawatts of systems and has discussed investing up to $100 billion into the company. OpenAI has separately committed roughly $300 billion to Oracle for cloud computing capacity under the Stargate initiative, and Oracle uses a meaningful share of that money to buy more Nvidia chips to build the data centres it owes OpenAI. AMD struck a 6-gigawatt chip supply deal with OpenAI and added warrants for up to 160 million AMD shares at a cent each, vesting as OpenAI hits purchase milestones and AMD’s own stock price climbs toward $600. Microsoft holds roughly a 27% stake in OpenAI, alongside a multi-year Azure commitment from OpenAI valued at $250 billion. CoreWeave, a so-called neocloud that rents out Nvidia capacity, took a $350 million pre IPO equity stake from OpenAI while expanding its own cloud contract with OpenAI to as much as $22.4 billion. Add it up and OpenAI alone has signed something in the order of $600 billion in future computing commitments, against roughly $13 billion in 2025 revenue and a $38.5 billion net loss the same year. Across the wider Nvidia, OpenAI, Oracle, Microsoft, AMD and CoreWeave web, various 2026 estimates put the total scale of circular financing arrangements above $800 billion.

Economist Ed Yardeni’s research team has tried to run what they call a capex payback test: do OpenAI and Anthropic’s revenue growth rates look fast enough to eventually justify the spending hyperscalers are committing on their behalf? Their conclusion, as of mid-2026, is that the picture is not yet fully revenue-backed, but it improves meaningfully by the early 2030s if current growth holds. That’s a more measured answer than either side of the debate wants to admit, neither proof of fraud nor proof of safety.

The defenders of these arrangements have a real argument, not just a talking point. Vendor financing, where a supplier helps fund its own customer, isn’t new or inherently fraudulent. Aircraft manufacturers and telecom equipment makers have done it for decades. The chips and data centres being built are real, usable assets rather than vapourware, and they can in principle be redeployed if a specific AI lab fails. And there’s genuinely independent evidence that demand for compute is outstripping supply right now, not just inside the loop.

That evidence shows up in the memory chip market, an industry the AI story barely touches in most coverage, but one that is currently living through what traders have started calling RAMmageddon. Samsung, SK Hynix and Micron, who together control more than 90% of global DRAM and HBM production, have shifted somewhere around 90 to 93% of their combined output toward the high-bandwidth memory that AI accelerators need, leaving a shrinking slice of capacity for the ordinary memory chips that go into phones, laptops and cars. DRAM prices rose roughly 90% in the first quarter of 2026 alone compared with the previous quarter. SK Hynix’s HBM order book is reportedly sold out through 2027. Samsung’s memory division now generates close to 94% of the company’s total quarterly profit. None of that can be faked by circular contracts between four companies. It’s showing up as higher prices for laptops and smartphones that have nothing to do with AI, which is about as close to independent confirmation of real demand as this debate gets. It’s also, on its own, a cost the rest of the economy is quietly absorbing regardless of how the bubble debate eventually resolves.

The dynamics covered in this article affect every US stock in your portfolio. Trade from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

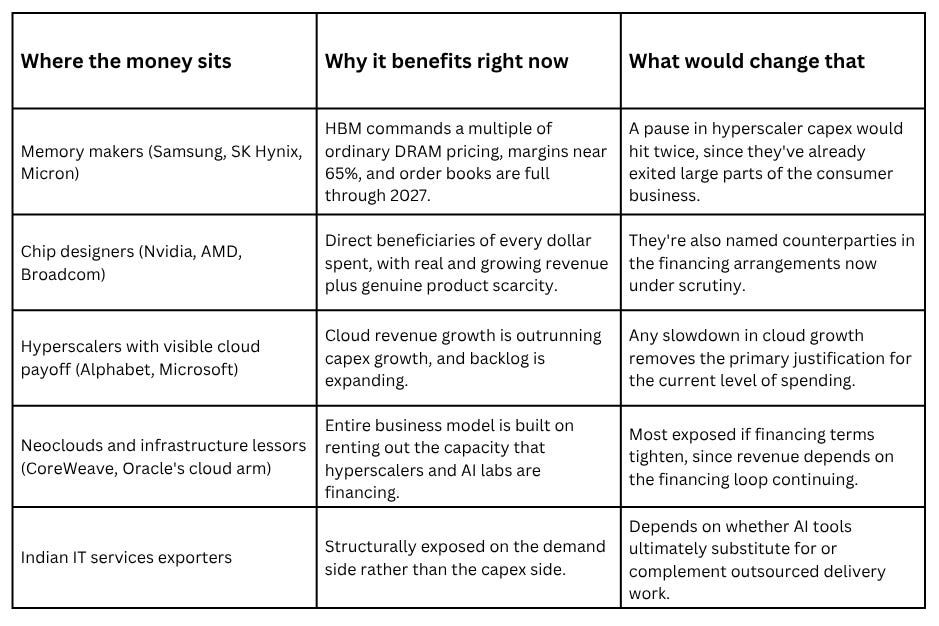

Who wins if the spending keeps going, and who loses either way 🏆

Not every company touched by this debate is exposed the same way, and the differences matter more than the headline Nasdaq number suggests.

The memory makers are living through what their own executives have called a golden era, with gross margins in the 63 to 67% range, comfortably ahead of even TSMC’s foundry margins, because they can charge AI customers premium prices for HBM while consumer-grade memory runs short everywhere else. That golden era is also their biggest vulnerability. Samsung, SK Hynix and Micron have walked away from large parts of the ordinary consumer memory business to chase AI margins, which means a pause in AI infrastructure spending would hit them on both sides at once.

Nvidia’s own numbers make the bull case look strong in isolation. Its most recent quarterly revenue rose 85% year on year to $81.6 billion, with the data centre business alone up 92% to $75.2 billion. The complication is that Nvidia is also the most direct counterparty in nearly every circular financing arrangement under scrutiny, so its results are simultaneously the best evidence that AI demand is real and the hardest evidence to take entirely at face value.

Among the hyperscalers themselves, the market has become much less forgiving about who gets credit for spending and who gets punished for it. Alphabet’s cloud division posted strong double-digit growth with an expanding enterprise backlog and was rewarded. Microsoft’s AI revenue line grew sharply, and it was rewarded, too. Meta grew revenue 33% in its most recent quarter and was punished anyway, because investors read its capex increase and accompanying capital raise as a company spending on hope rather than showing a visible near-term payoff. Show the market cloud revenue growing faster than capex, and the bull case holds. Raise capex without showing where the extra revenue comes from, and the stock gets sold regardless of how the broader AI story is going.

Illustrative framework based on public reporting. Not investment advice. Individual company exposure varies.

What this means if you’re an Indian investor in US tech 🇮🇳

On June 18, Accenture trimmed its full-year revenue growth guidance by exactly one percentage point, from a 3 to 5% range down to 3 to 4%. Its stock fell nearly 18% on Wall Street the same day, reportedly its steepest single-day drop as a public company. By the next morning in India, the damage had already crossed an ocean. The Nifty IT index sank by close to 6%, hitting a more than three-year low. Infosys fell as much as 8% intraday to around Rs 1,034, its lowest level in five years. TCS fell over 6% to around Rs 2,060, near a six-year low. HCL Tech, Wipro and Tech Mahindra all fell between 3 and 7%. By some reports, Indian IT stocks lost more than Rs 1.35 lakh crore in market value in a single session, because of one percentage point in an American consulting firm’s guidance.

That single day was the sharpest expression of a trend that’s been building all year. The Nifty IT index is down roughly 29 to 32% so far in 2026, against a high single-digit decline for the broader Nifty 50, and the combined weight of India’s five largest IT exporters in the Nifty 50 has fallen below 7.6%, the lowest level since at least 2002. At its peak more than two decades ago, the same cohort accounted for over a fifth of the index. IT has slipped to the fifth-largest sector in the Nifty 50, behind financials, consumer discretionary, energy, and industrials.

This isn’t only a market story. India’s top five IT firms reportedly cut headcount on a net basis in the financial year that ended in March, having added meaningfully more the year before, and gross hiring across the top five firms has fallen well below the average of the previous five years, with TCS alone guiding to noticeably fewer campus hires this year than its recent norm. Every part of the AI capex story that reads as an infrastructure opportunity on the US side of your portfolio is, on the Indian side, showing up as fewer campus placements, fewer promotions, and fewer new positions at the companies that have employed a generation of Indian engineers.

The two sides of this trade can sit in the same portfolio without you noticing. If you hold a broad US equity index fund through Winvesta alongside Indian IT stocks at home, you’re simultaneously long the infrastructure buildout that’s putting pressure on the outsourcing model, and long the outsourcing companies absorbing that pressure. Layered on top of that, anyone holding what looks like a diversified US index fund is, in practice, holding a concentrated AI bet whether they realise it or not. The Magnificent Seven alone account for roughly 32 to 35% of the S&P 500’s market value, up from around 12% a decade ago, and AI-linked names more broadly make up something closer to a quarter to a third of the index. The diversification a typical index fund investor assumes they’re getting and the concentration they’re actually carrying are two different things right now, and the gap between them is exactly what this entire debate is about.

The currency dimension adds one more layer. The rupee touched a record low near 96.8 against the dollar in May before recovering to around 94.3-94.5 by late June as oil prices fell back from their Iran war highs. If the AI trade cracks hard, the most likely accompanying scenario, based on what just happened on June 17, is the Federal Reserve holding rates higher for longer rather than cutting, which tends to support the dollar in the near term. That would mean a US tech sell-off and a firmer dollar showing up at the same time, squeezing rupee returns from both the price and currency sides together rather than one offsetting the other.

The five signals that actually tell you which way this breaks 🧭

Q2 2026 earnings season, landing through late July, is the first real test of whether the June scare changes anyone’s spending plans. Watch capex guidance specifically from Meta, which faces the sharpest investor scrutiny on return on spending, and watch whether AWS, Azure and Google Cloud can keep growing revenue faster than their owners are growing capex. That gap, not the headline spending number, is the one number that tells you whether the bull case is intact.

OpenAI and Anthropic’s IPO timing functions as a live sentiment gauge for the whole sector, given how much of the financing web runs through OpenAI specifically. A further delay, or a listing that prices meaningfully below the trillion-dollar figure Sam Altman has reportedly been holding out for, would be read as a verdict on the entire structure. A clean listing, alongside Anthropic’s reported move toward its first profitable quarter in Q2 2026, would do the opposite.

Memory prices and HBM supply are the closest thing to an independent lie detector here. If DRAM and HBM prices keep climbing through the back half of 2026, that’s continued evidence of demand outrunning supply. If they crack, particularly once Micron’s new Idaho fab or SK Hynix’s Yongin cluster bring on capacity closer to 2027 and 2028, that eases the one part of this story that has nothing to do with circular financing.

The Fed’s path under Kevin Warsh matters more to this trade than most investors currently price in. Roughly half the committee now sees a 2026 rate hike as more likely than a cut, a reversal from where things stood in March. Any data that pushes that further toward an actual hike raises the discount rate applied to exactly the kind of long-duration, spend-now, profit-later companies that dominate the AI trade.

Indian IT’s own Q1 FY27 results, due from Infosys and TCS in July, will show whether the Accenture-driven selloff was a one-off scare or the start of a deeper repricing. Deal win commentary, and revenue growth guidance from both companies will move Nifty IT more than almost anything else over the following month.

If this changed how you see the AI trade, pass it on.

The bottom line 🏁

The honest case against calling this a repeat of 2000 is specific, not vague reassurance. One widely cited analysis put the Nasdaq 100’s trailing multiple at roughly 33 times earnings, compared with close to 60 times at the March 2000 peak. A separate Fidelity analysis found the Magnificent Seven trading around 28 times forward earnings, less than half the roughly 66 times the seven largest US stocks by market cap commanded in 1999. The hyperscalers funding this buildout are, even with falling free cash flow, still generating real operating profit, unlike most of the infrastructure builders of the dot-com era who were burning cash with no revenue at all. And the physical assets being built- chips, data centres, power contracts- are largely redeployable rather than the fibre optic cable left dark and unused after 2001.

The honest case for genuine concern is equally specific. A relatively small group of companies is simultaneously each other’s biggest customers, biggest suppliers, and biggest investors, which means trouble at any one node travels quickly to the rest. Free cash flow at the companies doing the spending is falling even as the spending itself accelerates. And the market, after the June scare, has made clear it will punish any company that raises capex without a correspondingly visible payoff, which leaves very little room for disappointment from here.

The useful distinction for your own portfolio is between two different questions that keep getting collapsed into one. Is the underlying technology overhyped? Probably not, and the memory chip shortage is independent proof that real, paying demand for compute exists well beyond what any circular financing arrangement could fake on its own. Are the specific financing structures and valuations built around that technology fragile? That’s a genuinely open question, and the answer isn’t the same for every company sitting inside the loop.

The whiplash week that opened this piece- a brutal selloff followed five days later by a sharp rally in the exact same stocks- is the market itself admitting it hasn’t decided. Until it does, the more useful move is to know what you actually own, rather than guessing which way it breaks. A US index fund is not the diversified holding most people assume it is right now, and an Indian portfolio that pairs that index fund with domestic IT stocks is running both sides of this exact debate at once.

By the numbers

$450 billion to $700 billion, the range of estimates for combined 2026 capital expenditure across the major US hyperscalers, depending on which companies are included, up 60 to 80% from 2025

$800 billion+, the estimated scale of circular financing commitments across the Nvidia, OpenAI, Oracle, Microsoft, AMD and CoreWeave web, per various 2026 analyses

Roughly 90%, the rise in DRAM prices in the first quarter of 2026 alone, as memory makers shift capacity toward AI chips

32 to 35%, the Magnificent Seven’s share of S&P 500 market value, up from around 12% a decade ago

29 to 32%, the Nifty IT index’s decline so far in 2026, against a high single-digit decline for the broader Nifty 50

Below 7.6%, the combined weight of India’s top five IT exporters in the Nifty 50, the lowest since at least 2002

3.8%, the Federal Reserve’s median year-end 2026 rate projection after its June meeting, up from 3.4% in March, implying a possible hike rather than a cut

2027, the year OpenAI is now reportedly leaning toward for its IPO, pushed back from initial 2026 plans

All figures are directional estimates based on public reporting as of late June 2026. Individual company outcomes vary.

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.