Tesla (TSLA): A slowing carmaker priced as a robotaxi and robotics company

Analysing Tesla meant counting cars and arguing about the next delivery number. Not anymore. The car business shrank for a second straight year in 2025, Tesla lost the global electric-vehicle crown to BYD, and yet the stock is worth roughly $1.5 trillion, valued almost entirely on a robotaxi service that is still a pilot, full self-driving software, and a humanoid robot that does not ship yet. That is why we built Winvesta Crisps: to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Today, Tesla reports its second-quarter delivery numbers, and most retail investors will treat that single figure as the verdict on the company. It is the wrong number to obsess over. The delivery count Tesla releases on July 2 is a unit tally, not a financial result, and the full second-quarter financials will not be available until the earnings call later in July. More to the point, deliveries no longer explain why Tesla trades where it does.

Here is the gap that matters. Tesla’s reported business is a car company whose volumes fell in 2024 and again in 2025, plus a fast-growing energy storage arm and a sticky services line. The stock, by contrast, is priced on what Tesla might become: an autonomy and robotics platform that turns millions of existing cars into a software-driven robotaxi network and sells humanoid robots by the million. Both descriptions are true at the same time. The investing question is not whether Tesla makes good cars; it clearly does, but whether the market has correctly priced a venture-style bet on autonomy and robots that is still mostly unproven, sitting on top of a core car business that is going backwards.

🚗 What Tesla actually is in 2026

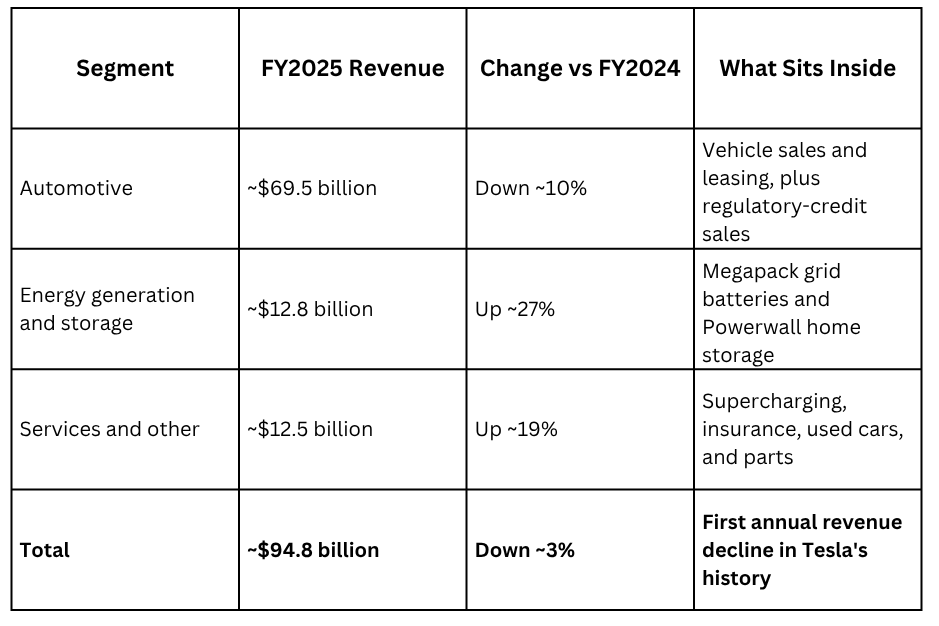

Tesla reports two operating segments: automotive and energy generation and storage. Inside those sit three revenue lines that behave very differently from one another. Automotive is still the giant, generating roughly $69.5 billion in 2025, per Tesla’s Q4 2025 shareholder update. Energy generation and storage, built on the Megapack grid battery and the home Powerwall, grew to about $12.8 billion. Services and other, which includes Supercharging, insurance, used-vehicle sales and parts, reached roughly $12.5 billion. On top of these reported lines sits the part of Tesla that has no revenue line of its own yet: full self-driving software, the Robotaxi service, the Dojo and AI-chip effort, and the Optimus humanoid robot.

The way Tesla talks about itself has shifted to match. On the most recent earnings call, CFO Vaibhav Taneja described a strategy where the company now treats full self-driving as the product and the vehicle as the delivery mechanism, per commentary reported by CoinDCX and TIKR. Through 2025, as deliveries fell, Elon Musk steered investor attention toward Robotaxi, Optimus and artificial intelligence rather than the car volumes, a pivot noted across the company’s last several earnings calls.

The logic the bulls are buying is straightforward to state and very hard to prove. Tesla has put more than nine million vehicles on the road, per its Q1 2026 operational summary, many of them carrying the cameras and compute the company says it needs for autonomy. If full self-driving crosses from supervised assistance into genuinely unsupervised driving, that installed base becomes, in theory, a robotaxi fleet that can be switched on by software. Add a humanoid robot aimed at factory and commercial work, and Tesla starts to look less like a carmaker and more like an applied-AI company that happens to manufacture its own hardware. That is the story in the price. The rest of this piece is about how much of it is real today.

🧩 Segment breakdown: where the money actually comes from

The headline number for 2025 declined. Total revenue slipped about 3% to $94.8 billion, Tesla’s first annual revenue drop, per the company’s full-year results. The mix beneath that flat-to-down top line is where the story gets more interesting, as the three lines move in different directions.

Source: Tesla Q4 2025 shareholder update and full-year earnings release. Segment figures are as reported by Tesla. Automotive revenue includes sales of regulatory credits, a high-margin line that is shrinking as US electric-vehicle incentives are rolled back.

Two things stand out. First, automotive did the damage, falling about 10% as volumes dropped and Tesla leaned on price to defend share. Second, the two smaller lines are quietly carrying the growth. Energy storage deployed a record 46.7 gigawatt-hours in 2025, up 49% year over year, per Tesla’s results, and that segment is no longer just selling batteries. In late June, Tesla, Sunrun and Renew Home announced a plan to aggregate more than 16 gigawatts of home energy capacity into a virtual power plant for utilities and data centres, per reporting on the partnership, a sign that energy is becoming a grid-services business as well as a hardware one.

Services and other has compounded for years on the back of an expanding car fleet: more cars on the road means more Supercharging revenue, more insurance, more used-vehicle flow and more out-of-warranty work. It is the most predictable line in the company and the least discussed.

Consider Rohan, a product manager in Pune who bought a few Tesla shares in 2023 because he liked the cars. Two years on, the part of his investment that grew was not the cars at all. It was the battery and grid-services business and the services attached to the existing fleet, lines he never thought about when he hit buy. The headline he keeps watching, deliveries, is the one that went backwards.

🤖 The core bet: robotaxi, full self-driving and a humanoid robot

This is the section that makes or breaks the bull case, and it is worth being precise about what exists today versus what is promised.

Start with Robotaxi. Tesla launched a paid, driverless ride service in Austin in mid-2025 and expanded it to Dallas and Houston in April 2026, using Model Y vehicles, per the company and Electrek. The service runs inside tight geofenced zones, and the fleet is small. Independent trackers and reports put Tesla’s robotaxi count in the low hundreds, and the company does not disclose a weekly trip figure. Tesla also lacks the permits required to run a driverless robotaxi service in California, where its current offering is human-driven, per coverage of the rollout. Management has guided to operating in roughly a dozen US metros by the end of 2026 and to volume production of the purpose-built Cybercab in the second half of the year, both of which are targets rather than shipped facts.

Then there is full self-driving, the software layer that is already generating something today. Tesla reported 1.28 million FSD subscriptions in the first quarter of 2026, per its earnings release, though that figure counts everyone who has bought the package, not only active monthly subscribers, a nuance Electrek and others have flagged. In late June, Tesla began rolling out a version of FSD v14 to older Hardware 3 cars, extending the software to millions of existing vehicles, per reporting from 24/7 Wall St. Tesla has said those older cars cannot run unsupervised driving without hardware changes, so the rollout is about engagement and subscription revenue, not autonomy. Broader expansion into China and Europe is targeted for 2026, subject to regulators, with an EU technical committee discussion on FSD approval flagged for late June.

The third leg is Optimus, the humanoid robot. Tesla has begun preparing production lines, with analysts at Cantor Fitzgerald modelling a Gen 3 ramp in Fremont in the second half of 2026 and only modest initial volumes, on the order of a few thousand units in 2027 rising over the following years, at a starting cost well above the roughly $20,000 Tesla has talked about at scale. Tesla has also said it completed the design of its next-generation AI inference chip and is pursuing a chip-fabrication partnership with SpaceX, per its Q1 2026 update. These are early-stage programmes.

Why does any of this support a $1.5 trillion valuation? Because the price targets that justify the stock are built on these bets paying off. ARK Invest has a 2029 target of $2,600 per share predicated on Optimus meeting production projections, and Wedbush has floated a $2 trillion market-capitalisation case conditional on commercial deployment of Optimus, per their published notes. Morgan Stanley has described the stock as essentially forward-valued, meaning the current business does not support the price on its own. That is the honest summary: the core bet is real, the ambition is enormous, and almost none of it is proven at scale yet.

Want to add Tesla to your portfolio? Trade TSLA directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.