Tariffs 101

What they are, how they work, and what they mean for your money

Building a global portfolio from India meant navigating a relatively stable world order. Not anymore. A single tariff announcement can now move global markets overnight, rewire supply chains across continents, and change the competitive landscape of every company you hold.

That’s why we built Winvesta Crisps — to decode what’s actually reshaping the world economy, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Think tariffs are just a nerdy policy detail that economists argue about on television? Think again. A single tariff announcement in Washington has been enough to wipe trillions off global markets overnight, spike prices at your local store, and redraw the map of which companies win and which ones bleed. In 2025 and into 2026, tariffs have gone from a background policy tool to the single biggest macro force shaping global portfolios — including yours.

If you’ve been watching markets yo-yo every time a trade headline drops and wondering why, this one’s for you.

What exactly is a tariff? 💡

A tariff is a tax that a government places on goods imported from another country. When a US company buys steel from China, for example, and the US government has imposed a 25% tariff on Chinese steel, that company pays 25% of the steel’s value as a tax to the US government at the port of entry.

Simple enough on paper. But here’s the part most people miss: the importing company doesn’t just absorb that tax quietly. It passes it on — to manufacturers, then to retailers, then to consumers. You end up paying more for appliances, cars, electronics, and groceries without ever seeing the word “tariff” on your receipt.

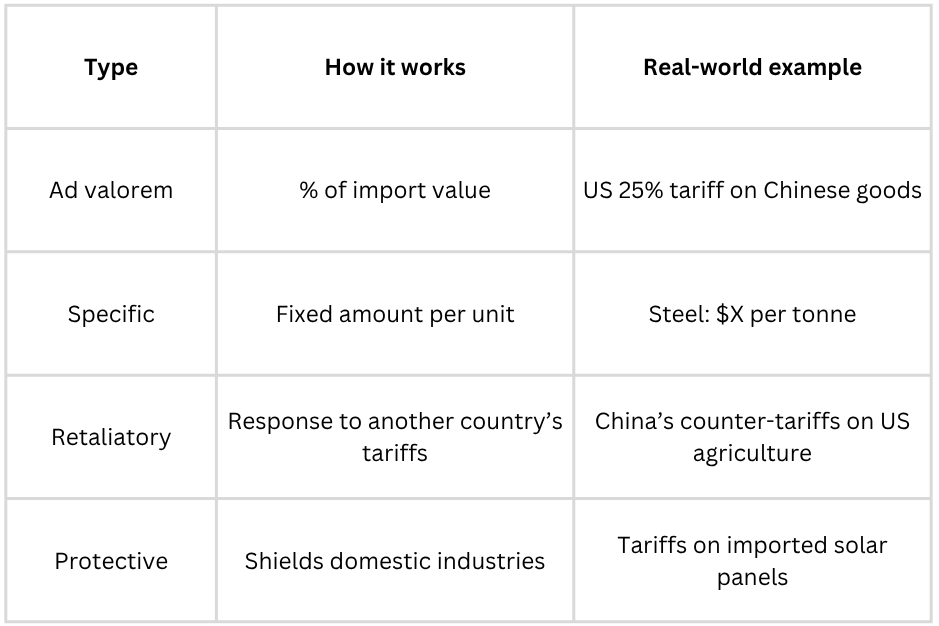

There are a few key types of tariffs worth knowing:

Ad valorem tariffs are calculated as a percentage of the value of the imported good, the most common kind. If a pair of shoes worth $50 is subject to a 20% ad valorem tariff, the importer pays an extra $10 per pair.

Specific tariffs are a fixed dollar amount per unit, regardless of price. A $5 tariff per tonne of imported wheat, for instance.

Retaliatory tariffs are what happen when Country B hits back after Country A fires the first shot. This is how trade skirmishes turn into full-blown trade wars — and it’s what rattled global markets repeatedly from 2018 through 2025 and beyond.

Understanding which type is in play matters — because ad valorem tariffs during an inflation spike are especially nasty for consumers.

How tariffs ripple through the economy 🔧

Here’s what most financial news coverage skips: Tariffs don’t just affect the targeted industry. They send shockwaves far beyond the initial point of impact, touching inflation, interest rates, corporate earnings, and investor sentiment all at once.

The inflation channel

When tariffs raise the cost of imported inputs — such as steel, semiconductors, and chemicals — manufacturers face higher production costs. Those costs flow downstream. The US National Bureau of Economic Research has found, in multiple analyses of the 2018–2019 tariff rounds, that the bulk of the tariff burden was borne by domestic importers and consumers, not by foreign exporters. In other words, tariffs often function as a tax on your own country’s consumers.

In 2025, the US average effective tariff rate reached historically elevated levels not seen in decades, and inflation expectations adjusted accordingly, per Reuters and Bloomberg reporting.

The earnings channel

For listed companies, tariffs hit in two ways simultaneously. Input costs rise (squeezing margins) while consumer demand may soften (squeezing revenues). That double-squeeze is what analysts call a “margin compression event” — and it tends to hurt mid-cap industrials and consumer discretionary names hardest.

The interest rate channel

Here’s the tricky part: Inflation from tariffs puts central banks in an uncomfortable position. The Federal Reserve and other central banks typically raise rates to fight inflation — but tariff-driven inflation is a supply-side shock, not a demand-side one. Raising rates to fight it risks strangling growth without actually fixing the supply problem. This is the “stagflation trap” that economists warned about repeatedly in 2025.

The confidence channel

Perhaps the most underappreciated channel. Businesses delay investment decisions when they can’t model their input costs with confidence. Supply chains get restructured. Long-term contracts get renegotiated. This drags on GDP growth in ways that don’t show up immediately in headline numbers, but compound over quarters.

Why governments use them — and why they often backfire 🎯

Governments reach for tariffs for several distinct reasons, and it’s worth separating the legitimate uses from the ones that tend to blow up in everyone’s face.

The legitimate case

Protecting infant industries is the classic economic justification. When a domestic industry is too young to compete against established foreign players, a temporary tariff can give it breathing room to develop scale and efficiency. South Korea’s semiconductor sector arguably benefited from exactly this kind of industrial policy in its early years.

National security is another defensible ground. Keeping some strategic manufacturing capacity at home — whether in defence, pharmaceuticals, or critical minerals — reduces vulnerability during crises. The COVID-19 pandemic made this argument viscerally real when countries discovered they couldn’t manufacture their own PPE.

Correcting unfair practices — responding to foreign government subsidies or dumping (selling below cost to undercut competitors) — is also a recognised purpose under WTO rules.

Where it goes wrong

Retaliation spirals are the most common failure mode. When the US hits Chinese goods, China hits American soybeans. American farmers suffer. Beijing doesn’t back down. The targeted sector ends up collateral damage in a political standoff. This played out with near-clockwork precision in the 2018–2019 and 2024–2025 rounds.

Domestic inefficiency is the longer-run cost. Protected industries don’t always use their shelter to become competitive — sometimes they simply become more dependent on protection. Consumers pay above-market prices indefinitely. Downstream industries that rely on the protected input lose competitiveness globally.

Diplomatic fallout extends beyond the targeted trade. Tariff disputes have repeatedly poisoned broader diplomatic relationships, slowing cooperation on everything from climate policy to security agreements.

The honest assessment: Tariffs are a blunt instrument that can serve narrow purposes well, but tend to produce large unintended consequences when used broadly or sustained over long periods.

🚀 Join 60,000+ investors — become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Winners and the bruised: Sectors in the crossfire 🏆

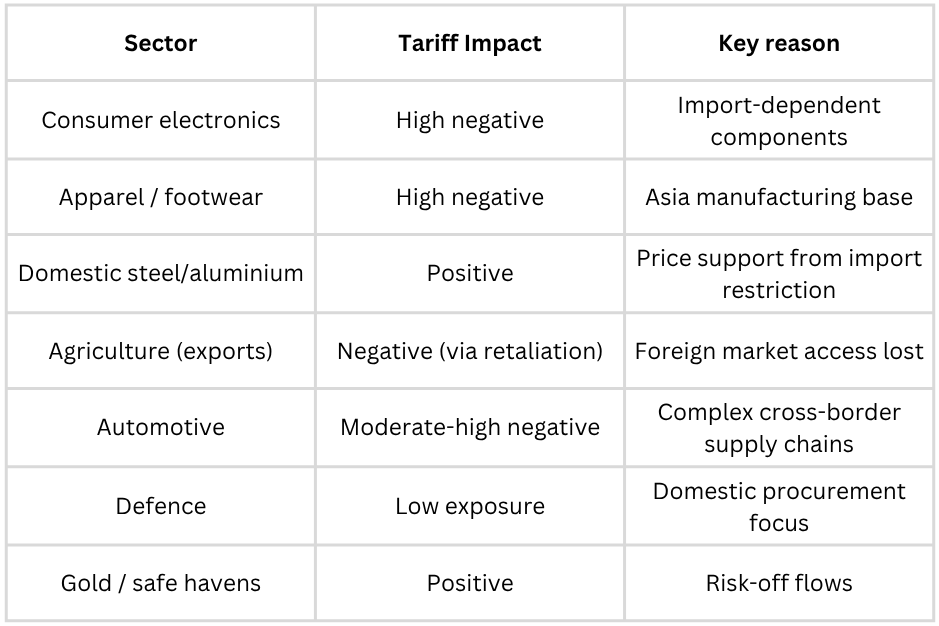

Not all sectors are created equal when tariffs hit. Understanding the exposure map is one of the most practical things an investor can do in a tariff-heavy environment.

Sectors that tend to get hurt

Consumer electronics and technology hardware face some of the most acute pressure. Global supply chains for chips, displays, and components are deeply intertwined with Asia, China and Taiwan in particular. When tariffs target these imports, product costs rise, and margins compress across the board, from smartphones to data centre equipment.

Consumer discretionary — apparel, footwear, and furniture are heavily import-dependent. Brands that manufacture primarily in Asia and sell in the US face a direct cost squeeze. Budget-conscious consumers trade down, premium brands lose pricing power, and margins fall.

Agriculture and food exports are often hit hardest by retaliatory tariffs from trading partners. When China restricts US soybean imports or the EU retaliates against American whiskey, domestic producers face collapsed demand in export markets, with few short-term alternatives.

Automobile manufacturers operating global supply chains face parts costs rising from multiple directions simultaneously — steel, aluminium, and electronic components all affected at once.

Sectors that can hold up — or even benefit

Domestic industrials and steel/aluminium producers are the clearest direct beneficiaries. Higher prices for imported metals translate directly into pricing power for domestic producers. US Steel and domestic aluminium smelters saw revenue tailwinds during the 2018–2019 tariff round.

Defence and aerospace tend to be insulated, as their procurement is largely domestic by design.

Energy is a mixed picture. Oil and gas trade flows are relatively tariff-exempt under most frameworks, though equipment and components for the sector can be affected.

Gold and other safe-haven assets typically see inflows during trade-war uncertainty as investors seek protection from currency and equity volatility.

Domestic-focused companies — businesses whose revenues are primarily domestic and whose supply chains don’t cross borders heavily — are structurally more insulated than global multinationals.

Someone shared this with you? If this changed how you see the global economy and what’s driving markets, pass it on.

History’s playbook: What past trade wars taught us 📜

Tariff wars are not new. They’ve played out before, and the historical record carries lessons that current events are busy repeating.

Smoot-Hawley (1930): The textbook warning

The US Smoot-Hawley Tariff Act of 1930 raised tariffs on over 20,000 imported goods to record levels, intending to protect American farmers and manufacturers during the early Great Depression. The result was catastrophic. Trading partners retaliated. US exports collapsed. Global trade contracted sharply. Most economic historians now view the Smoot-Hawley Tariff Act as having deepened and prolonged the Depression, not mitigated it. It remains the definitive cautionary tale — still cited in virtually every serious trade policy discussion, per Bloomberg.

US-China round one (2018–2019): The managed escalation

The first major tariff confrontation of the modern era saw the US and China exchange successive rounds of tariffs covering roughly $360 billion in bilateral trade by late 2019. US equity markets saw repeated sharp selloffs on escalation announcements, per Reuters. A “Phase One” deal in early 2020 paused the escalation but left most tariffs in place. Key lesson: financial markets hate tariff uncertainty even more than tariff levels. Once a tariff is in place and priced in, markets can adapt. It’s the back-and-forth escalation that creates lasting volatility.

2024–2025: The second wave

The sweeping “reciprocal tariff” framework announced in 2025 represented the most significant disruption to global trade architecture since the Smoot-Hawley Tariff Act, per multiple economic research bodies. Average US effective tariff rates reached levels not seen in roughly a century. Equity markets repriced accordingly — with growth and technology stocks under the most pressure, and defensive sectors outperforming on a relative basis.

The consistent historical pattern: early escalation hurts equities broadly; Defensive and domestic-facing sectors outperform; the eventual resolution (or stabilisation) provides relief, but supply chain restructuring takes years to play out fully.

What this means for Indian investors 🇮🇳

For Indian investors with exposure to US equities through Winvesta, the tariff landscape creates specific dynamics worth understanding — beyond just reading headlines and reacting.

Direct effects on US portfolios

If you hold US tech names, consumer discretionary stocks, or globally integrated manufacturers, tariff headwinds are already embedded in analyst earnings estimates. The key question is whether the actual impact is better or worse than what’s priced in. Consensus estimates for affected sectors in 2025 were repeatedly revised lower as tariff reality exceeded initial projections, per Bloomberg.

If you hold domestic-oriented US companies — think utilities, US-focused financials, domestic consumer staples — the tariff impact is relatively contained.

The currency dimension

Tariff wars introduce meaningful currency volatility. Dollar strength or weakness during trade conflicts affects the rupee-dollar exchange rate, which in turn affects the real returns you earn on USD-denominated assets when converting back to INR. Keeping an eye on USD/INR and maintaining some currency awareness in your portfolio construction is prudent.

India’s own positioning

India navigated earlier rounds of US tariffs with relatively lower direct exposure than China, Vietnam, or Mexico — but that picture has shifted. By 2025, the US had imposed substantial penalty tariffs on India in certain product categories, making Indian exporters more directly in the line of fire than before. Indian sectors such as IT services remain largely exempt from US goods tariffs; pharmaceuticals and textiles carry greater direct exposure and warrant closer monitoring.

Three things to watch

Tariff escalation or de-escalation headlines — new announcements still move markets sharply. Building in some volatility tolerance and avoiding over-leveraged positions in highly exposed sectors is sensible.

Corporate earnings calls — listen for what management teams say about input cost pass-through, supply chain adjustments, and demand sensitivity. The guidance language often tells you more than the headline numbers.

The Fed’s response — if tariff-driven inflation keeps headline CPI elevated, the Fed stays higher for longer. That puts continued pressure on long-duration growth stocks. Watch Fed communications closely alongside trade headlines.

Common mistakes investors make in a tariff environment

Panic-selling broad index funds. Tariff shocks are real but typically transitory in their market impact. Long-term index fund investors who sold during the 2018–2019 trade war often missed the subsequent recovery.

Treating all “tech” as equally exposed. Software companies generating primarily domestic revenues (cloud, SaaS) are structurally different from hardware manufacturers dependent on Asian supply chains. Lumping them together produces poor investment decisions.

Chasing “tariff winners” is too late. Domestic steel stocks, for instance, often rally sharply on tariff announcements — but then consolidate or reverse as the initial sentiment fades and fundamental reality catches up. Buying after a 30% tariff-driven surge is rarely the right move.

Ignoring second-order effects. A retailer might not import directly, but if its key suppliers do, the cost eventually shows up in its P&L. Reading through the supply chain matters.

The bottom line 🏁

Tariffs are not a temporary blip. They’ve become a structural feature of the global investment landscape — and understanding them is now a basic competency for any serious investor, not just an optional deep-dive.

The key things to hold onto: tariffs raise costs for domestic consumers and businesses more than they hurt foreign exporters. They create sectoral winners and losers that are mostly predictable once you understand the exposure map. They tend to spark retaliation cycles that outlast the original political intent. And history has been pretty consistent — prolonged, broad-based tariff wars tend to drag on economic growth while creating inflationary pressure, a combination that no central bank handles gracefully.

For your portfolio: stay clear-eyed about which holdings have meaningful tariff exposure, resist reactive trading on every headline, and remember that supply chain restructuring takes years — the companies that navigate it strategically are the ones worth holding through the volatility.

The trade war isn’t over. But now you know exactly what you’re watching — and why it matters.

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.