Stagflation: The market’s scariest word, and what investors should actually do about it

Earlier, betting on steady growth and low inflation may have worked. Not anymore. A confluence of tariff shocks, sticky price pressures, and slowing GDP growth is rewriting the rules of portfolio management, and the investors who understand stagflation before it’s officially declared are the ones who’ll be best positioned when the dust settles.

That’s why we built Winvesta Crisps, to break down the macro forces that actually move your portfolio, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors know how to handle a recession, pull back, go defensive, and wait it out. Most also know how to handle inflation, lean into commodities, shorten duration, and stay nimble. But what happens when both show up at the same time, and the usual playbook stops working? That’s stagflation. It’s rare, it’s nasty, and right now, it’s the word economists are whispering with increasing urgency. If you’re an investor who hasn’t thought seriously about this scenario, today’s the day to start.

But what exactly is stagflation? 🤔

The word itself is a portmanteau, “stagnation” meets “inflation.” In plain English: the economy is barely growing (or contracting), unemployment is rising, and prices are still going up. All three at once.

That’s the nightmare scenario, because the standard policy toolkit breaks down completely.

Here’s why it’s so dangerous:

To fight inflation, central banks raise interest rates, which slows growth and kills jobs even further.

To fight a recession, central banks cut rates and stimulate, which pumps more fuel onto the inflation fire.

It’s a trap. You can’t fix one problem without making the other worse. That’s what makes stagflation so uniquely destructive, and so feared by policymakers and investors alike.

The textbook definition:

Stagflation = High inflation + Slow or negative GDP growth + Rising unemployment

Why are we talking about this now? The 2025–26 context 🗓️

This isn’t just an academic exercise. Several forces colliding right now have investors genuinely concerned.

1. Tariff-driven inflation: The wave of import tariffs introduced since early 2025 has pushed up costs for goods ranging from electronics to apparel to industrial components. These aren’t demand-driven price hikes; they’re cost-push inflation, meaning consumers pay more even as growth slows. That’s a stagflation-flavoured setup.

2. Slowing growth signals: Consumer spending has softened in recent quarters. Manufacturing PMIs in the US and Europe have spent extended periods below 50 and only recently edged back toward the expansion line. Business investment has stalled as companies wait for policy clarity. GDP growth forecasts for 2026 remain modest and face meaningful headwinds, even as some recent upgrades reflect AI-driven investment and partial tariff easing.

3. The Fed’s impossible position: The Federal Reserve wants to cut rates to support growth, but persistent inflation, still running above the 2% target, prevents it from moving as aggressively as markets would like. That tension is exactly the kind of stalemate that characterised stagflation periods historically.

To be clear: Today’s data don’t show full-blown stagflation. Growth has been surprisingly resilient, and inflation has cooled meaningfully from its 2022 peaks. But the mix of tariff shocks, sticky-ish inflation, and policy constraints is rhyming with past stagflationary episodes more than investors are used to, and that’s exactly why the playbook is worth understanding before the consensus catches up.

The last time this happened: The 1970s playbook 📜

The definitive stagflation era in modern history was the United States in the 1970s. Understanding what happened then is the clearest lens we have.

The setup:

The 1973 OPEC oil embargo sent energy prices through the roof.

US GDP growth turned negative. Unemployment climbed above 9%.

Inflation hit double digits, peaking above 14% by 1980.

The S&P 500 delivered essentially zero real returns through the entire decade, once you strip out inflation.

What worked:

Commodities: Oil, gold, and agricultural goods surged as inflation ran hot.

Real assets: Real estate held up as a store of value.

Short-duration bonds: Long-term bonds were destroyed by inflation, but short-term paper could be rolled over as rates rose.

Energy stocks: The one sector of the stock market that genuinely outperformed.

What didn’t:

Rising discount rates crushed growth stocks and tech.

Long-term bonds were a disaster. Holding a 30-year Treasury in the 1970s was one of the worst investments you could make.

Consumer discretionary collapsed as purchasing power eroded.

The resolution eventually came from Fed Chair Paul Volcker, who raised interest rates to a staggering 20% in 1980, deliberately inducing a painful recession to break inflation’s back. It worked, but it took years of pain to get there.

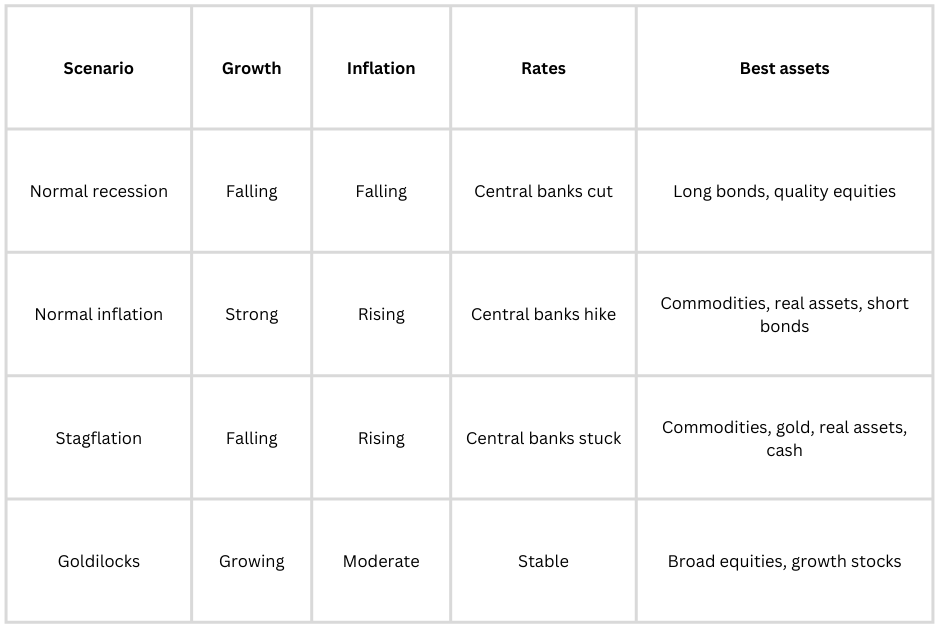

How stagflation is different from a normal recession ⚖️

This distinction matters enormously for how you position your portfolio.

The key insight: In a normal recession, bonds save you. In stagflation, they don’t because inflation is still eating away at fixed payments. The safe haven playbook changes entirely.

The sectors that historically survive stagflation 🏆

Not all sectors suffer equally. History gives us a reasonably clear hierarchy.

Outperformers

Energy: When stagflation is driven by supply shocks (like an oil embargo or tariff-induced supply chain disruption), energy companies are often the source of the inflation, meaning they’re collecting the higher prices, not paying them. Energy stocks were the standout winners of the 1970s stagflationary period.

Gold and other precious metals: They are a classic hedge against stagflation. It holds real value when fiat currency is being eroded, and it doesn’t depend on economic growth for its appeal. During the 1970s, gold rose from roughly $35 an ounce to over $800 by 1980.

Commodities: Agricultural commodities, industrial metals, and raw materials tend to perform well as cost-push inflation drives up their prices. Commodity producers benefit from the same logic as energy companies.

Utilities and infrastructure: Their revenues are often inflation-linked (regulated pricing), their dividends are real and recurring, and their demand doesn’t collapse even when consumers cut back on discretionary spending.

Healthcare: Demand for healthcare is largely non-discretionary; people don’t stop needing medical care because the economy is slow. Defensive earnings give this sector relative resilience.

Underperformers

High-multiple growth stocks: When interest rates stay elevated or rise further, the present value of future earnings gets hammered. Growth stocks, whose value depends heavily on earnings years away, suffer disproportionately.

Consumer discretionary: When real wages are squeezed by inflation, consumers cut non-essential spending first. Restaurants, luxury goods, travel, and entertainment are vulnerable.

Long-duration bonds: As painful as it sounds, the classic “safe haven” of long bonds becomes a trap in stagflation. Inflation relentlessly erodes the real value of fixed-coupon payments.

Banks and financials: Caught in the squeeze between rising credit defaults (bad economy) and compressed net interest margins, financial stocks tend to lag during genuine stagflationary periods.

If this changed how you think about your portfolio, share it with your investing circle.

How to think about your portfolio right now 🧠

A few frameworks that actually hold up under stagflationary pressure.

1. Lean into real assets

Things with intrinsic value — commodities, real estate, infrastructure, natural resources, act as inflation shields. They don’t need a growing economy to hold their value; they need inflation to be real.

2. Shorten your bond duration

If you hold bonds, shift toward shorter maturities. Short-term bonds reprice quickly as rates move, giving you optionality. Long-term bonds lock you into a fixed rate while inflation eats it away.

3. Think internationally

Some markets and currencies benefit when the US dollar is under pressure. Commodity-exporting economies, think Brazil, Australia, Canada can outperform in environments of rising commodity prices and weak US growth.

4. Revisit your growth-stock concentration

High-multiple tech and growth names built their valuations in a low-rate, high-growth world. That world looks different now. It doesn’t mean exiting tech entirely, but being thoughtful about what you’re paying for and why matters more than ever.

5. Don’t panic into cash, but don’t ignore it either

Cash feels uncomfortable when inflation is high, because it’s losing real value. But in a stagflationary recession, having dry powder to buy assets at distressed valuations can be genuinely powerful. A small but deliberate cash position is a real strategic tool.

The indicators to watch 🧭

You don’t need to wait for economists to declare stagflation officially. Watch these signals:

CPI and PCE data: Is inflation staying sticky above 3–4% even as growth slows?

GDP revisions: Two consecutive quarters of negative growth are the technical recession threshold. Watch closely.

Unemployment claims: Rising jobless claims alongside persistent inflation are the clearest signs of stagflation.

Fed language: When Fed minutes start using words like “difficult tradeoffs” or “supply-driven inflation”, that’s the signal they see the trap too.

Yield curve: An inverted yield curve already flags recession risk. If long yields remain elevated even as the curve re-steepens, inflation expectations haven’t come down.

Real wages: If nominal wages are rising but real wages (after inflation) are falling, consumers are being squeezed, even if the headline numbers look okay.

What investors get wrong about stagflation ⚠️

Mistake 1: Treating it like a normal recession. The instinct in a downturn is to buy bonds and defensive equities. In stagflation, bonds may not save you, and even quality defensives get squeezed by higher borrowing costs and margin pressure.

Mistake 2: Waiting for “official” confirmation. By the time stagflation is declared and consensus is formed, the best positioning moves have already played out—the market prices in macro shifts months ahead of official data.

Mistake 3: Going all-in on gold. A genuine stagflation hedge, but it’s also volatile, pays no income, and can underperform for long stretches. It should be a part of a diversified strategy, not the whole strategy.

Mistake 4: Assuming it’s permanent. The 1970s eventually ended. Stagflation, like all macro regimes, is cyclical. The investors who positioned defensively for the storm, but kept enough exposure to participate in the recovery, came out best.

The bottom line: Don’t fear it, understand it 🏁

Stagflation is a genuinely difficult environment. The usual rules bend. The standard playbook gets thrown out. But it’s not a scenario without a strategy; it just requires a different one.

The investors who navigated the 1970s best weren’t the ones who panicked or buried their heads. They were the ones who understood what was happening mechanically, adjusted their exposure toward real assets and away from rate-sensitive growth stories, kept their time horizon long, and didn’t get shaken out by the volatility along the way.

If the current mix of sticky inflation, tariff pressure, slowing growth, and a stuck central bank starts to crystallise into something more sustained — knowing this playbook in advance puts you meaningfully ahead of the crowd that’s still wondering why bonds aren’t working.

Understanding the “scary” scenarios is exactly what separates disciplined, long-term investors from those who get caught off guard.

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.