Should you follow Greg Abel’s first Berkshire letter?

Or is this just expensive nostalgia?

Most investors read Abel’s letter and felt reassured. Meanwhile, Berkshire’s trading at near the top of its decade-long valuation range, capital is fleeing the sectors Abel loves, and Apple — which makes up around a fifth to a quarter of the equity portfolio — is doing all the heavy lifting. The comfort was everywhere. The context was nowhere.

That’s why we built Winvesta Crisps — to decode what’s actually driving the stocks you own, in plain language, before the consensus catches up.

60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in your spam folder.

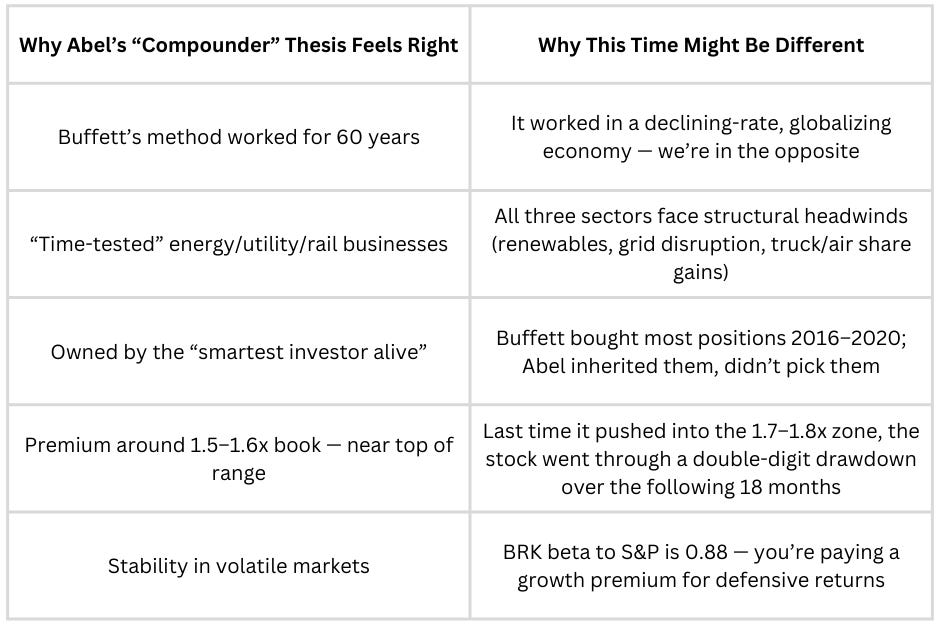

Greg Abel just sent his first shareholder letter as Berkshire Hathaway’s CEO, highlighting four stocks he expects will “compound over decades.” If you own BRK.B directly or through India-focused US equity funds, you probably felt a wave of relief reading it. The Oracle has a successor who sounds... almost like the Oracle.

But here’s what nobody’s talking about: Berkshire trades at around 1.5–1.6x book value right now — near the upper end of its last-decade range (which has spanned roughly 1.0–1.8x). And those four “compounder” stocks Abel loves? Three of them have posted negative alpha versus the S&P 500 over the past 18 months. So are you buying into Abel’s vision, or are you paying a Warren Buffett premium for a Greg Abel portfolio?

🎯 First, let’s see if you’re actually Priya

Priya, 38, product manager at a fintech startup in Pune.

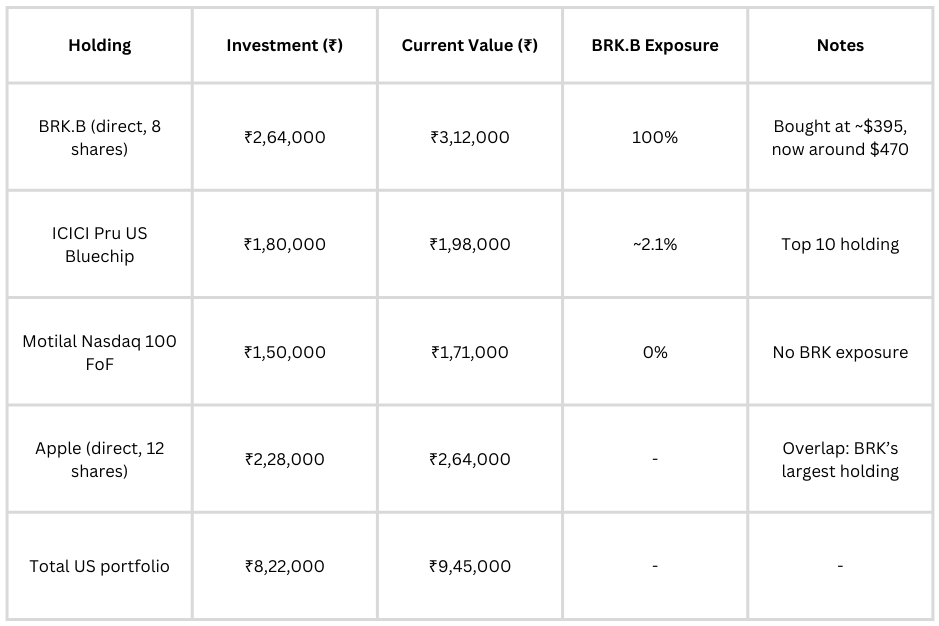

She’s been building her US equity portfolio for four years through a mix of direct stocks and Indian mutual funds with US exposure. She bought 8 shares of BRK.B in early 2024 at around $395, thinking she was getting “Buffett at a discount.” She also owns ICICI Pru US Bluechip Equity Fund and Motilal Oswal Nasdaq 100 FoF.

Here’s what Priya’s portfolio actually looks like:

Priya’s hidden reality: She thinks she owns ₹3.12 lakh of Berkshire. But she actually has ₹3.16 lakh in BRK.B exposure when you account for fund overlap. More importantly, she owns ₹2.64 lakh of Apple directly — and Apple is Berkshire’s largest equity holding, often around 20–30% of its public stock portfolio by value in recent filings.

So Priya effectively has substantial combined exposure to Berkshire’s strategy (direct BRK + Apple + fund overlap). That’s not diversification — that’s a concentrated bet on one investment philosophy now being executed by a 62-year-old who hasn’t yet been tested in a full bear-market cycle as CEO.

What happened to Priya in the April 2024 tech drawdown? When Apple dropped 12% on China fears, her portfolio fell 8.3% in two weeks — twice the Nifty’s dollar-adjusted decline — because her “diversified” US holdings were all dancing to Berkshire’s tune.

📊 What ETF flows actually tell you

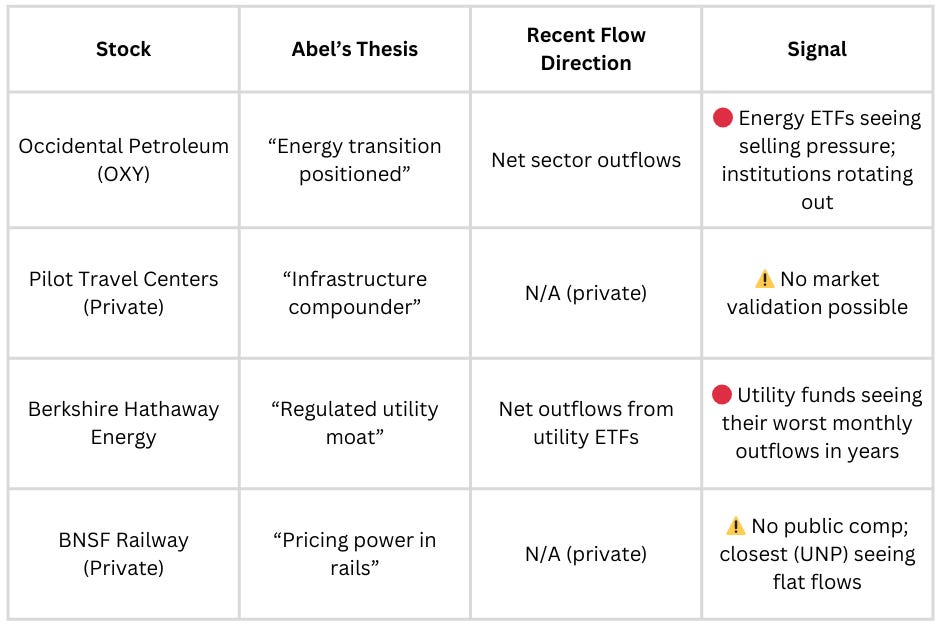

Berkshire isn’t heavily owned through thematic ETFs (it’s too unique), but the stocks Abel highlighted in his letter are flowing in different directions. This tells you whether the market actually agrees with his “compounder” thesis.

Here’s what happened to the four stocks Abel called out in his letter:

Here’s the problem: Two of Abel’s four “compounders” are private (no price discovery), and the two public-adjacent sectors are seeing capital leave.

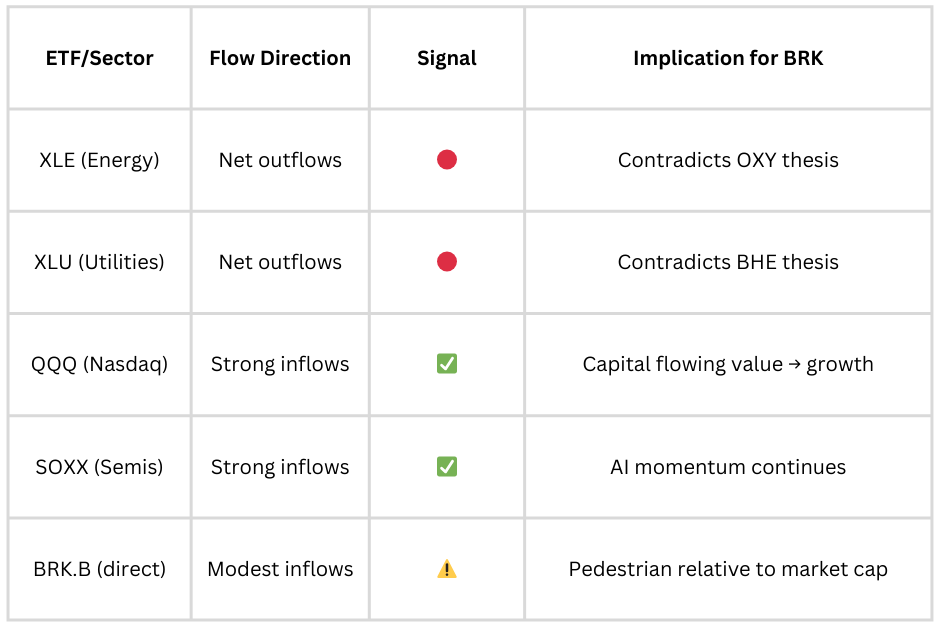

Now let’s look at where money IS actually going in March 2026:

The divergence is screaming: The market is rotating INTO the exact stocks Berkshire underweights (AI, semis, growth tech) and OUT of the sectors Abel just doubled down on in his letter.

BRK.B’s own inflows are modest relative to its roughly $950 billion market cap — tiny compared to the percentage-of-market-cap flows going into names like NVDA or even XOM.

Translation: Berkshire is getting “legacy continuity” inflows (people who liked the letter and feel comforted by Abel sounding like Buffett), NOT “conviction compounder” inflows.

🧠 The psychology trap

Abel’s letter was a masterclass in continuity signalling. He used Buffett’s phrase “buy wonderful businesses at fair prices” verbatim. He quoted Charlie Munger. He even structured the letter with the same railroad-insurance-energy order Buffett used for 40 years.

And that’s EXACTLY why it feels so comforting to hold BRK.B right now. You get to tell yourself: “The philosophy hasn’t changed. This is still Buffett’s Berkshire, just with a new nameplate.”

But here’s the uncomfortable question: What if continuity is exactly the wrong strategy for 2026?

Here’s the rational vs FOMO checklist. Be honest with yourself:

Rational reasons to own BRK.B:

You want S&P-like returns with 10–15% lower volatility

You believe energy/rails/utilities outperform tech over 10 years

You’d buy BRK.B at 1.2–1.3x book and are comfortable with current levels

You understand you’re buying a conglomerate holding company, not a growth stock

FOMO/emotional reasons:

“Buffett built the best track record ever, so Abel inherits that magic”

The letter made you feel like you’re in the smart-money club

You don’t want to sell and look dumb if BRK outperforms next year

Everyone says “just hold great companies forever”, and BRK feels like the ultimate version

If you checked more boxes on the bottom than the top, you’re not investing in Berkshire — you’re investing in the idea of Berkshire.

🚀 Want to trade BRK.B and other US stocks from India? Join 60,000+ investors on the Winvesta app and get direct access to US markets.

💡 Three realistic scenarios for Priya’s portfolio

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.