Salesforce (CRM): The agentic enterprise play hiding inside the world’s biggest CRM

The bear case on Salesforce was that it would get disrupted by smaller, nimbler SaaS challengers undercutting its pricing. Today, the bear case is the opposite: that AI will do the work humans used to buy software licences to assist with, hollowing out per-seat subscription economics across the entire enterprise software category. Neither version of the bear case has killed the business. In FY2026, Salesforce generated $14.4 billion in free cash flow, returned 99% of it to shareholders, and booked 29,000 Agentforce AI deals. The market’s fear and the financial reality are not pointing in the same direction.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

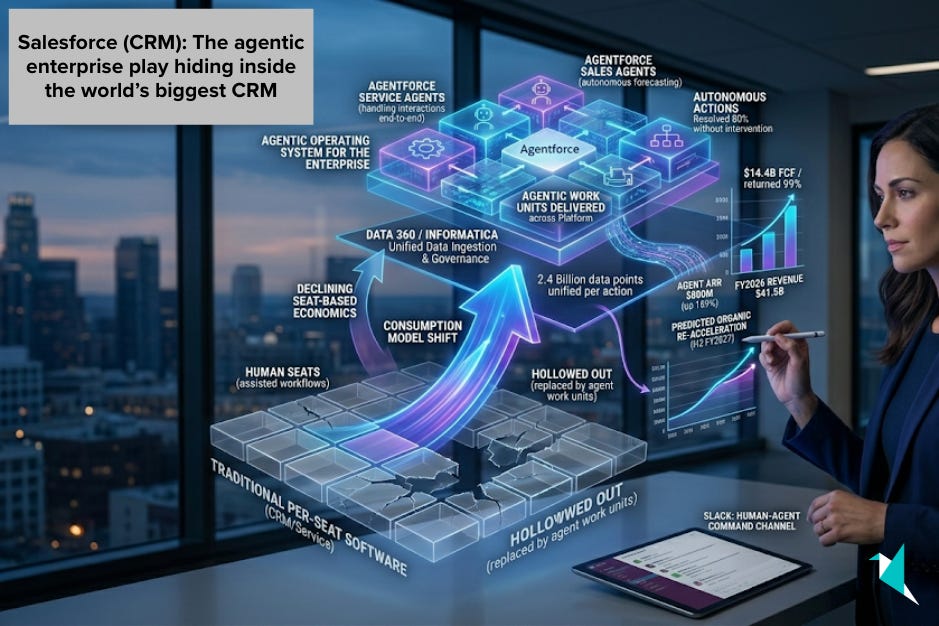

Most investors still think of Salesforce as the company that sells seats of CRM software to sales teams. That framing is accurate and dangerously incomplete. The stock has fallen around a third year to date as of early May 2026, per MarketBeat, weighed down by a market narrative that AI disrupts per-seat software models and Salesforce is squarely in the crosshairs. What that narrative misses is the deeper transformation underway: Salesforce is deliberately engineering a second revenue layer inside its existing customer base, one priced not by how many humans use the software but by how much work AI agents actually do on behalf of those customers.

Salesforce reported $41.5 billion in FY2026 revenue; its Q4 growth of 12% year-over-year was the fastest in two years; and Agentforce's annual recurring revenue hit $800 million, up 169% in a single year, per the company’s Q4 FY26 earnings release. Free cash flow reached $14.4 billion, up 16%. The company authorised $50 billion in share repurchases and returned $14.3 billion to shareholders, equal to 99% of FY2026 free cash flow. The operational story is strong. The valuation story is complex. And the strategic story, the one about what Salesforce is actually becoming, is being almost entirely missed by the market.

🔄 Business model 2.0: From seat licences to the operating system for the agentic enterprise

Salesforce spent two decades building one of the most defensible businesses in enterprise software: a cloud-based CRM platform so deeply embedded in the sales, service, and marketing workflows of large organisations that replacing it requires years, significant capital, and a tolerance for disruption that most enterprises lack. That moat is real. It generates $39.4 billion in subscription and support revenue, per Salesforce’s FY2026 earnings release, from customers who have trained their operations around the platform.

What the company is now doing is layering a second economic model on top of that installed base. The traditional model charges per human user, per month: a sales representative, a service agent, a marketing manager. The new model charges for outcomes delivered by AI agents, measured in conversations handled, actions taken, or credits consumed. The installed base is the distribution. The AI agents are the monetisation surface.

The shift matters because it changes the economics of Salesforce’s relationship with every existing customer. A customer who previously purchased 500 service agent seats to handle inbound support queries now has the option to deploy Agentforce to handle a large portion of those interactions autonomously. Salesforce internally deployed Agentforce across its customer support organisation, handling hundreds of thousands of interactions, with more than 80% resolved autonomously. That drove tens of millions of dollars in annual savings and allowed the reallocation of several hundred support workers to higher-value tasks, as described by Salesforce in earnings commentary and case studies.

For Salesforce as a vendor, this creates an unusual dynamic. The AI deployment simultaneously reduces the customer’s need for human seats while creating new consumption revenue from the AI agents themselves. The company is betting that the total value delivered, and therefore the total contract size, grows even as the mix shifts from seats to consumption. The market is sceptical. That scepticism is priced into the stock.

Consider Kavya, a product manager at a Bengaluru-based fintech who has been running Salesforce Service Cloud for her customer support team for three years. Her organisation recently piloted Agentforce to handle tier-one queries, including password resets, KYC status checks, and account limit questions, which account for roughly 60% of inbound volume. The AI handles those interactions autonomously. Her team of 12 is now focusing on escalations and complex cases. Her Salesforce bill has not shrunk. It has grown, because she added Agentforce consumption credits on top of her existing seats. That is the dynamic Benioff is betting on at scale.

🧩 Revenue breakdown: Six clouds and a growing AI layer

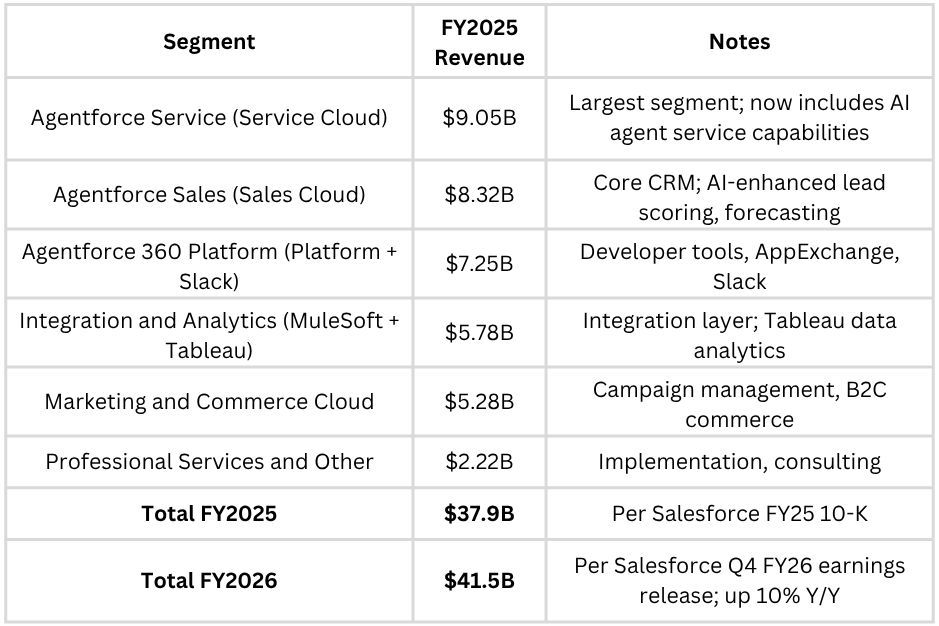

Salesforce reports subscription revenue across five major product lines plus a professional services segment. The table below uses FY2025 figures, which are the most granular publicly available sub-segment breakdown per Salesforce’s FY2025 10-K. FY2026 total subscription and service revenue is sourced from the FY2026 earnings release.

Note: Salesforce renamed its service offerings to Agentforce-branded names in Q3 FY2026. There were no changes in how revenue is allocated between these segments following the rename.

The headline shift within these numbers is structural. Service Cloud overtook Sales Cloud as the largest single revenue line in FY2024 and has remained so, reflecting that customer service automation is the most immediate use case for Agentforce deployments. When enterprises start with AI agents, they overwhelmingly start in the contact centre, where the volume of repetitive interactions is highest, the ROI of automation is most measurable, and the regulatory complexity is lowest compared to sales or financial workflows.

Platform revenue, which includes Slack, matters for a different reason. Slack is being repositioned as the interface layer through which humans and AI agents interact in shared channels, functioning as the command centre for the agentic enterprise. Benioff has described this positioning explicitly on multiple earnings calls. If Agentforce agents increasingly operate through Slack channels, then Slack’s value to the enterprise compounds with every new agent deployed.

The Agentforce AI layer itself generated $800 million in ARR as of Q4 FY2026, and combined with Data 360 (including Informatica Cloud ARR of $1.1 billion), the broader AI and data platform reached $2.9 billion in ARR, up over 200% year-over-year, per Salesforce’s Q4 FY26 earnings release.

Want to add Salesforce to your portfolio? Trade CRM directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

⚡ Agentforce and Data 360: The core strategic bet

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.