Recession signals: The economic warning signs every investor should know

Buying every dip and holding forever was the playbook. Not anymore. In a world where tariff shocks, rate cycles, and macro surprises can erase months of gains in days, knowing how to read recession signals isn’t just for Wall Street economists; it’s the skill that separates investors who survive drawdowns from those who panic-sell at the bottom.

That’s why we built Winvesta Crisps, to decode the macro forces shaping the markets you invest in, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Every bull market eventually ends. But what separates the investors who position themselves ahead of a downturn from those who watch their portfolios bleed in slow motion? It comes down to one thing: knowing what to watch — before the headlines catch up.

Right now, in April 2026, recession risk is back on everyone’s lips. No official recession has been declared — reputable commentators are split between “soft landing” and “meaningful slowdown” camps — but tariff shocks have rattled global supply chains, consumer confidence is wobbling, and equity markets have sold off sharply in recent weeks. Whether or not a recession materialises, the warning signs are worth understanding now. Recessions rarely arrive without a trail — in bond markets, employment data, manufacturing surveys, and consumer spending patterns — for months before the economy officially tips over.

This edition of Winvesta Crisps breaks down exactly what those signals look like, what they mean for your money, and how to use them to stay a step ahead.

What exactly is a recession? 🤔

The textbook definition is deceptively simple: two consecutive quarters of negative GDP growth. The National Bureau of Economic Research (NBER) in the US — the official arbiter of recession dating — goes further, defining it as a significant decline in economic activity spread across the economy, lasting more than a few months, visible in GDP, income, employment, industrial production, and retail sales.

But here’s what most people miss: by the time a recession is officially declared, it’s usually already been underway for months. The NBER called the start of the 2008 recession in December 2008, but the economy had actually peaked in December 2007. Markets had already fallen by roughly 40% before the official declaration landed.

This lag is precisely why forward-looking indicators — the ones that sniff out trouble before it shows up in the GDP report — matter so much.

The yield curve: Wall Street’s recession crystal ball 📉

If you could only watch one recession indicator for the rest of your investing life, most economists would point you to the yield curve — specifically, the spread between the 10-year US Treasury yield and the 2-year (or sometimes 3-month) Treasury yield.

Here’s the logic. Normally, long-term bonds pay higher interest than short-term ones — investors demand more compensation for locking up money for longer. When that relationship flips — when short-term yields rise above long-term ones — it’s called an inverted yield curve, and it’s historically been one of the most reliable recession precursors on record.

Why does inversion matter?

It signals that markets expect the Federal Reserve to cut rates sharply in the future, which typically happens because the economy is weakening.

Banks, which borrow short and lend long, see their margins squeezed. They pull back on lending. Credit tightens. Growth slows.

The 10-year/2-year spread inverted meaningfully before each of the last several US recessions. It’s not perfect timing — the lag between inversion and recession onset can range from several months to well over a year — but as a directional warning sign, it has a strong track record.

What to watch: When the 10-year yield drops meaningfully below the 2-year, pay attention. When the curve starts to “uninvert” (spreads start widening again), that can paradoxically be when recession risk is at its highest — banks are pricing in rate cuts because things are already deteriorating.

Someone shared this with you? If this changed how you see markets and macro, pass it on.

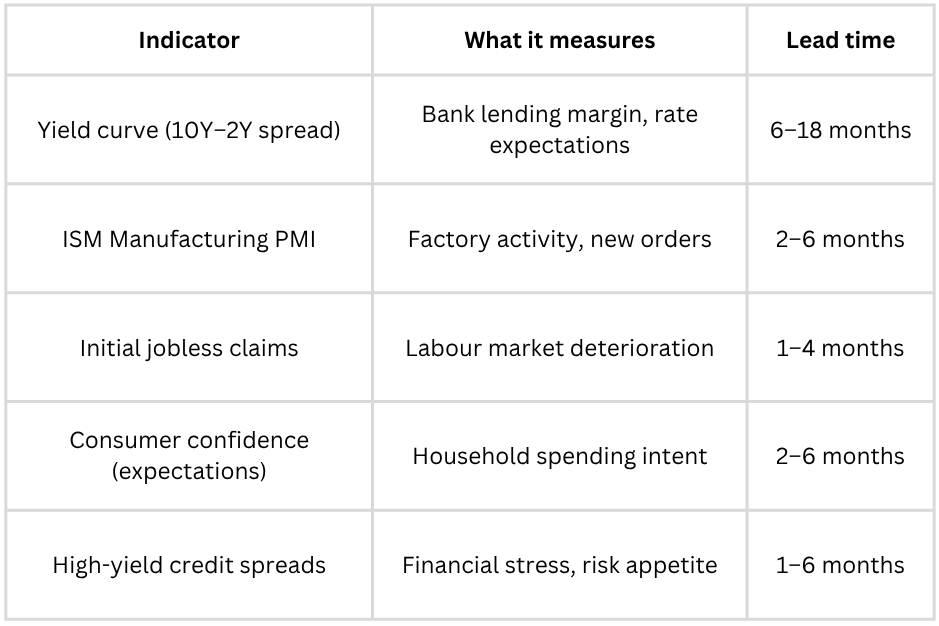

Five other indicators that flash red before it’s too late 🔍

The yield curve gets most of the press, but sophisticated investors watch a whole dashboard of signals. Here are five others worth tracking:

1. The ISM Manufacturing PMI

The Institute for Supply Management’s Purchasing Managers’ Index surveys manufacturing executives about new orders, production, employment, and supplier deliveries. A reading above 50 signals expansion; below 50 signals contraction.

Manufacturing tends to be cyclically sensitive — it often rolls over before the broader economy does. Several months of sub-50 PMI readings, especially alongside deteriorating new orders, are a meaningful warning.

2. Initial jobless claims

Every week, the US Department of Labour releases the number of people filing for first-time unemployment insurance. This is one of the most real-time economic data points available — and it tends to trend upward well before unemployment rates (a lagging indicator) start rising.

A sustained, meaningful climb in weekly jobless claims from cycle lows is worth watching closely.

3. Consumer confidence surveys

The Conference Board’s Consumer Confidence Index and the University of Michigan’s Consumer Sentiment Index both measure how households feel about current conditions and their expectations for the next 6-12 months. Consumers drive roughly two-thirds of US GDP.

When confidence turns sharply lower — especially in the “expectations” sub-components — spending slowdowns typically follow. Watch for multi-month deterioration, not just one noisy reading.

4. The LEI (Leading Economic Index)

The Conference Board’s Leading Economic Index aggregates 10 forward-looking components: manufacturing hours, building permits, credit spreads, stock prices, new orders, and more. It’s designed explicitly to lead the economic cycle by several months.

Six consecutive months of decline in the LEI has historically been a common precursor to recession — though it’s worth noting that the 2022–24 period showed extended LEI weakness without an immediate NBER-declared recession, so treat it as a probabilistic signal, not a hard rule.

5. Credit spreads

High-yield (or “junk”) bond spreads — the extra yield investors demand to hold riskier corporate debt versus US Treasuries — are a real-time gauge of financial stress. When spreads widen sharply, it means credit markets are pricing in higher default risk, tighter financial conditions, and economic slowdown. Stock markets typically follow.

Note: Lead times are directional estimates based on historical patterns. They vary across cycles.

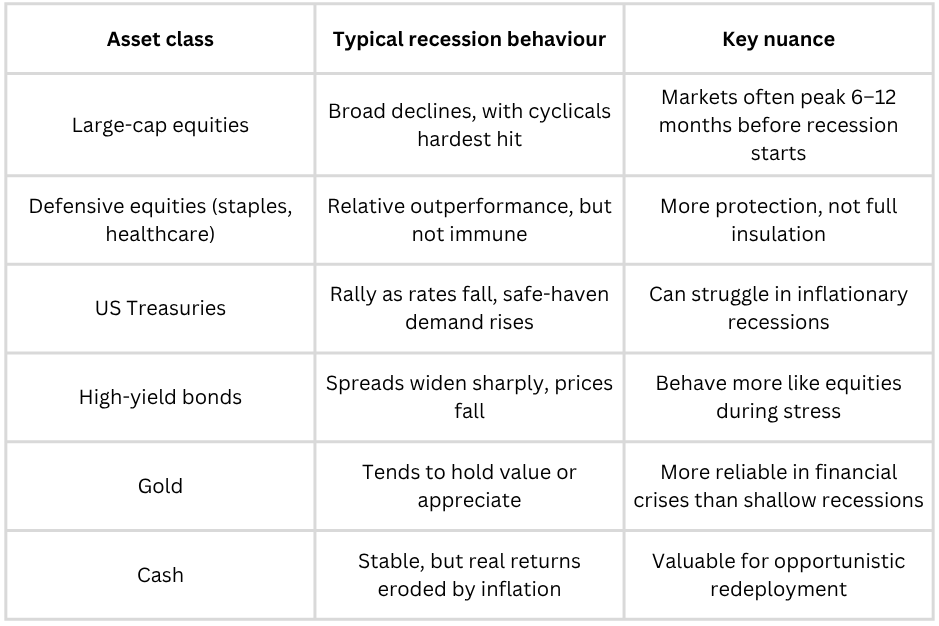

Recessions and your portfolio: What history shows 💼

Not all assets react the same way when the economy contracts. Understanding the historical playbook helps you think about positioning — even if no two recessions are identical.

Equities broadly fall during recessions, but the timing and magnitude vary significantly. Markets often begin declining 6–12 months before a recession is officially declared, pricing in the slowdown ahead of the GDP data. The steepest drops have historically occurred in cyclical sectors — consumer discretionary, industrials, financials — while defensive sectors like consumer staples, healthcare, and utilities have tended to hold up better.

Bonds (particularly US government bonds) have historically been a safe-haven destination during recessions. As rates fall and investors seek safety, Treasury prices rise. This is the classic “risk-off” rotation. However, in inflationary recessions — sometimes called stagflation — this dynamic can break down, since high inflation keeps yields elevated even as growth falters.

Gold has frequently benefited from recession-driven uncertainty. It doesn’t always rally in a straight line, but as a store of value and crisis hedge, it’s attracted flows during episodes of significant market stress.

Cash and short-duration bonds have historically provided capital preservation during equity drawdowns, giving patient investors “dry powder” to redeploy when valuations compress.

Illustrative historical patterns are not a guarantee of future performance.

🚀 Want to position your portfolio ahead of macro shifts? Trade US stocks and ETFs directly from India on the Winvesta app, no US bank account needed!

Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Leading vs Lagging: The timing trap most investors fall into ⏰

One of the most common mistakes investors make is confusing leading indicators — which anticipate economic turns — with lagging indicators, which confirm what has already happened. Acting on lagging data is like driving while only looking in the rear-view mirror.

Leading indicators move before the economy turns. Yield curve, LEI, manufacturing PMI, consumer expectations, credit spreads — these are all leading. They’re noisier and less certain, but they give you early warning.

Coincident indicators move roughly in line with the economy — GDP, industrial production, and personal income. These confirm you’re in a recession, usually in real time.

Lagging indicators confirm a trend after it’s well established — the unemployment rate, for instance. The headline unemployment rate typically peaks well after a recession has already ended. By the time it’s making headlines, the worst is usually over.

The practical implication: When recession fears are rising, it’s worth paying more attention to leading indicators than to the unemployment rate or the most recent GDP print. The leading indicators are telling you where the economy is going; the lagging ones are telling you where it’s been.

How Indian investors in US markets should think about this 🌏

For Indian retail investors accessing US markets through platforms like Winvesta, there are a few layers of complexity beyond just tracking the economic cycle.

Currency dynamics matter. During US recessions, the dollar often strengthens initially as investors flee to safety — which can actually benefit Indian investors holding dollar-denominated assets, at least in rupee terms. However, if a recession is severe enough to prompt aggressive Fed rate cuts, the dollar can weaken significantly, which reduces the rupee-denominated value of your US holdings.

Your investment horizon is your biggest edge. If you’re investing in quality US companies or index ETFs with a multi-year horizon, short-term recession drawdowns — painful as they feel — are historically part of the journey to strong long-term returns. The investors who came out ahead after the 2008 financial crisis and the 2020 COVID crash were the ones who stayed invested or added during the depths.

Diversification across cycles is your structural protection. No single asset class dominates across all environments. A mix of broad US equity exposure, some allocation to defensive sectors or dividend-paying stocks, and possibly a small allocation to gold-linked instruments can smooth out the ride during recessionary periods without sacrificing long-term growth potential.

Watch for LRS and tax implications. For Indian investors using the Liberalised Remittance Scheme to invest in US markets, sudden portfolio restructuring during volatile periods can have tax and forex timing implications. Think through rebalancing moves carefully rather than reacting impulsively to headlines.

Common mistakes to avoid when recession fears rise ⚠️

Knowing what to look for is only half the battle. Knowing what not to do when recession signals start flashing is equally important.

1. Panic-selling at the bottom

Markets typically price in recessions well before they arrive — and recover well before they officially end. Investors who wait for the “all-clear” signal from official data often miss the sharpest early phases of the recovery—selling into a drawdown locks in losses and risks missing the rebound.

2. Treating every yield curve inversion as an immediate sell signal

The yield curve has inverted before each recent US recession — but the timing has been highly variable. Investors who shorted the market immediately upon every inversion have frequently sat out extended bull markets while waiting for the recession to materialise.

3. Confusing short-term pain with structural collapse

Not every recession leads to a multi-year bear market. Some are sharp and shallow; others are deep and prolonged. Before repositioning aggressively, it’s worth assessing whether the situation is a cyclical slowdown or a systemic financial crisis — the playbook is very different.

4. Over-rotating into cash and missing the recovery

Building a cash buffer during heightened uncertainty is sensible. But moving entirely to cash when recession fears peak — often exactly when markets are at their cheapest — has historically been one of the most costly mistakes long-term investors make.

5. Ignoring signals entirely because “this time is different”

Every cycle brings arguments that the old indicators no longer apply. Sometimes those arguments have merit. But dismissing consistent, multi-indicator warning signals because the economy “feels strong” has repeatedly burned investors.

The bottom line 🏁

Recessions are a feature of the economic cycle, not a bug. They’ve happened before, they’ll happen again, and the investors who understand the warning signs are far better positioned than those who react purely to headlines.

The yield curve, the ISM PMI, jobless claims, consumer confidence, and credit spreads are not magic — no indicator predicts anything with certainty. But together, they paint a picture of where the economic cycle is headed, and they tend to paint it months before the official GDP data catches up.

The most useful takeaway from any study of recession indicators isn’t a specific trade — it’s a mindset shift. Instead of reacting to economic data after it’s reported, build the habit of watching the leading signals that precede it. Instead of panicking when the headlines get scary, understand which part of the cycle you’re actually in. And instead of trying to perfectly time the market, position your portfolio for resilience across cycles.

The investors who do that consistently rarely need to predict recessions precisely. They just need to be prepared for the possibility — and history suggests that preparation is where the real edge lives.

📊 Stat block

Average US recession duration (post-WWII): roughly 10 months

Average S&P 500 peak-to-trough decline during recessions: approximately 30–35%, directionally

Yield curve inversion to recession onset: historically ranged from around 6 months to over 18 months across recent cycles

ISM Manufacturing PMI threshold: readings below 50 for several consecutive months have historically aligned with economic contraction

Leading Economic Index: Six consecutive months of decline have been a consistent precursor to recession in prior cycles

All figures are directional estimates based on historical patterns. Individual cycles vary.

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.