Netflix stopped counting subscribers. Here’s what it’s counting instead.

Tracking a streaming stock used to mean scanning a single quarterly subscriber number and calling it done. Not anymore. When Netflix broadcasts live NFL games, airs WWE Raw every Monday evening, and delivers live boxing events to tens of millions of concurrent viewers, the comparison set shifts—away from streaming rivals and toward broadcast television, live sports networks, and global advertising platforms.

That’s why we built Winvesta Crisps—to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors still price Netflix against Disney+, Max, and Amazon Prime Video—measuring churn rates, content spend, and password-sharing holdouts as if subscriber count is the only number that matters. The reality is sharper. Netflix voluntarily retired subscriber reporting in early 2025, broadcast NFL games on Christmas Day, locked in a decade-long WWE Raw deal, and built one of the fastest-growing advertising platforms in streaming, per independent ad-industry estimates.

Based on management guidance and consensus expectations, it is now tracking toward mid-teens revenue growth, expanding operating margins, and very high double-digit growth in ad-tier users—delivering all of it without disclosing a single subscriber figure, instead framing the business around engagement hours, advertising revenue trajectory, and operating leverage. The company that invented binge-watching is quietly becoming something harder to categorise—and that shift is not a communications strategy. It is an accurate description of what the business is actually becoming.

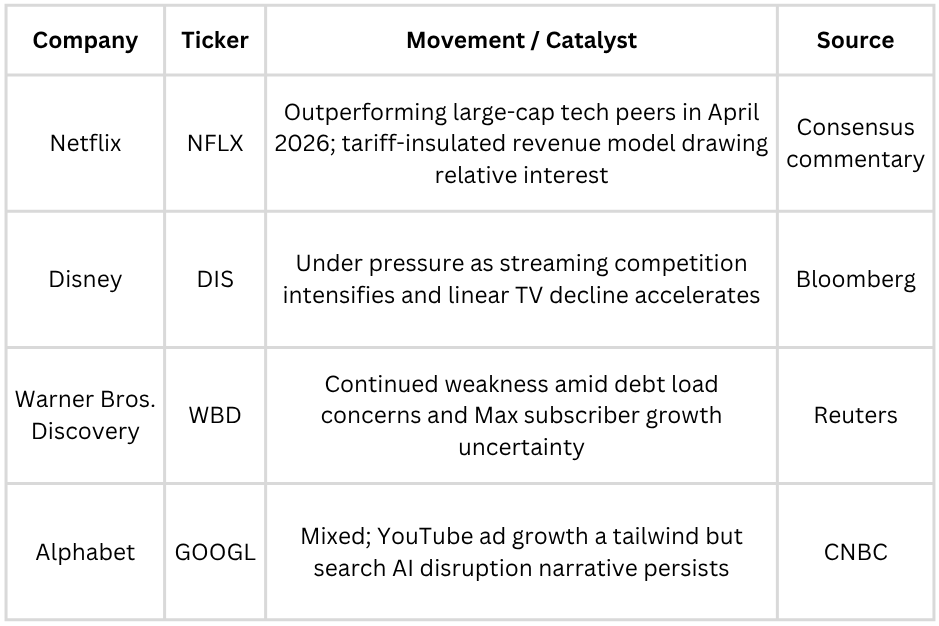

🔥 Top movers

Note: NFLX has shown notable resilience relative to most large-cap technology names through April 2026’s volatile tape. Its software-only revenue model offers a relative shelter from tariff-driven volatility compared with hardware-heavy peers—though this is an inference from Netflix’s business mix rather than management attribution. Price levels referenced throughout are approximate, drawn from guidance and consensus analysis. Exact share prices vary by session.

🍏 Current landscape

Netflix sits at a genuine inflexion point. The subscriber-growth phase of its story is largely complete. The harder, more interesting work now is monetising that audience more deeply—through advertising, live events, and international expansion.

The subscriber era is over: Netflix stopped reporting quarterly subscriber numbers beginning with Q1 2025, after announcing the change in its Q1 2024 shareholder letter, shifting analyst attention toward revenue per member, total engagement hours, and advertising revenue growth. Management’s view: engagement and monetisation are more accurate proxies for business health than raw headcount.

Advertising tier momentum: The ad-supported tier has expanded to tens of millions of monthly active users globally, with penetration highest in markets where Netflix has raggressively aised ad-free plan prices Ad revenues roughly doubled in 2024, per public reporting, with Netflix targeting another strong step-up in 2025—and early indications suggest high growth continues into 2026, though Netflix does not break out full ad revenue figures separately yet.

Live events as audience anchors: Netflix’s live programming—NFL Christmas Day games, WWE Raw from January 2025, high-profile boxing events—demonstrates the platform’s capacity to drive simultaneous peak viewership that on-demand streaming structurally cannot. Live events are not merely content; they are tools for audience concentration that create premium advertising inventory unavailable to pure-streaming rivals.

Tariff insulation: Unlike Apple, hardware-exposed technology names, or any company reliant on global supply chains, Netflix’s revenue is almost entirely software and service-based. Tariff volatility, which has pressured manufacturing-exposed US stocks, has had only a limited direct impact on Netflix’s cost structure—a structural advantage in the current macro environment that investors have noticed.

🌀 Turning the tables

How is Netflix repositioning from a subscriber-growth story into a multi-revenue-stream entertainment platform?

1. The advertising build

Netflix launched its ad tier in late 2022 with modest ambitions and has since built a full-stack programmatic advertising platform, hiring aggressively from Google, Meta, and traditional media buying firms. The company has deployed its own proprietary ad server—eliminating its dependence on Microsoft’s advertising infrastructure, on which it initially relied—and built first-party data capabilities that give it targeting precision comparable to the largest digital platforms, anchored in premium video content. Advertisers are shifting budgets from linear television to Netflix’s inventory, per industry reports.

2. Live events as a weekly habit flywheel

The WWE Raw deal—a roughly decade-long, multi-billion-dollar arrangement—is the clearest expression of Netflix’s live events strategy. WWE Raw brings a loyal, habitual audience to Netflix every Monday evening, creating a recurring viewing pattern that streaming drama cannot replicate. The NFL Christmas Day games in 2024 demonstrated that Netflix’s technical infrastructure can handle peak simultaneous viewership at scale—a capability that was previously uncertain. Management has signalled a continued appetite for additional live sports rights, per public commentary.

3. Gaming as a long-duration option

Netflix’s gaming vertical—mobile games bundled with subscription at no additional charge—has grown to around 100 titles as of recent disclosures, per company filings. However, engagement remains modest relative to the video library. Management frames gaming as a years-long investment, not a near-term revenue driver: optionality that deepens subscriber value without requiring standalone monetisation to justify its existence immediately.

✨ What is working?

Several structural advantages continue to compound in Netflix’s favour heading into the second half of 2026:

Pricing power: Netflix has implemented multiple price increases globally over the past two years—across both ad-free and ad-supported tiers—with minimal observable impact on churn, per management commentary. That pricing resilience reflects genuine consumer attachment to the content library that competitors have struggled to replicate.

Content efficiency: After years of concern about runaway content spend, Netflix has demonstrated improved efficiency—generating more engagement hours and retention impact per dollar of content investment than the prior cycle, per analyst estimates. The shift toward licensing and co-productions alongside original spend has helped.

Operating leverage: As revenue grows, fixed-cost content amortisation and technology infrastructure spread across a larger base—driving operating margin expansion toward the high-twenties to low-thirties percentage range over the medium term.

Password-sharing discipline: While the initial crackdown drove a discrete surge in subscribers in 2023–2024, the account management discipline it installed—combined with continued price increases—has more durably benefited revenue per unit of engagement.

Free cash flow compounding: Netflix’s free cash flow generation has expanded substantially, enabling share buybacks and content reinvestment without balance sheet stress. FCF margin has grown meaningfully over the past two years, per public reporting, giving management the flexibility to fund live events ambitions without compromising financial stability.

Want to add Netflix to your portfolio? Trade $NFLX directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors—become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

🚩 Key challenges ahead

Netflix’s transformation is not without genuine obstacles:

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.