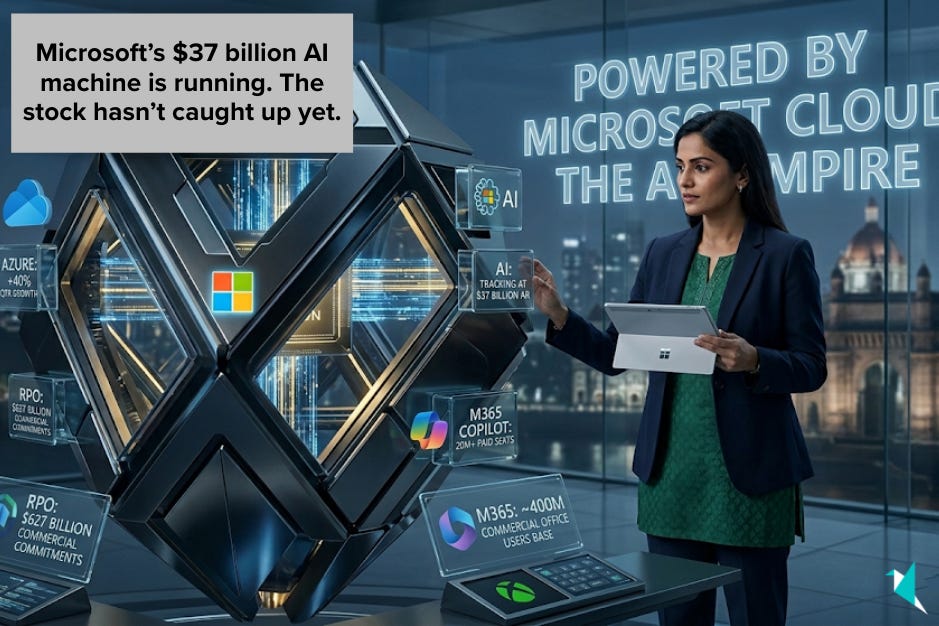

Microsoft’s $37 billion AI machine is running. The stock hasn’t caught up yet.

Owning Microsoft because of Windows and Office may have worked. Not anymore. The company that built its empire on productivity software has quietly become one of the most consequential AI infrastructure businesses on the planet. Azure just grew 40% in a single quarter. Copilot crossed 20 million paid seats. The AI business is tracking at $37 billion in annualised revenue, up 123% year over year. And the stock is still down mid-teens year to date as of late April 2026. That disconnect is what this article is about.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors still think of Microsoft as the company that makes Windows, Office, and Teams. That framing made sense in 2018. In 2026, it misses the entire growth story. The business that just reported a record quarter on April 29, $82.9 billion in revenue, EPS of $4.27, and Azure growing 40%, is increasingly an AI cloud infrastructure company with a massive productivity software flywheel attached.

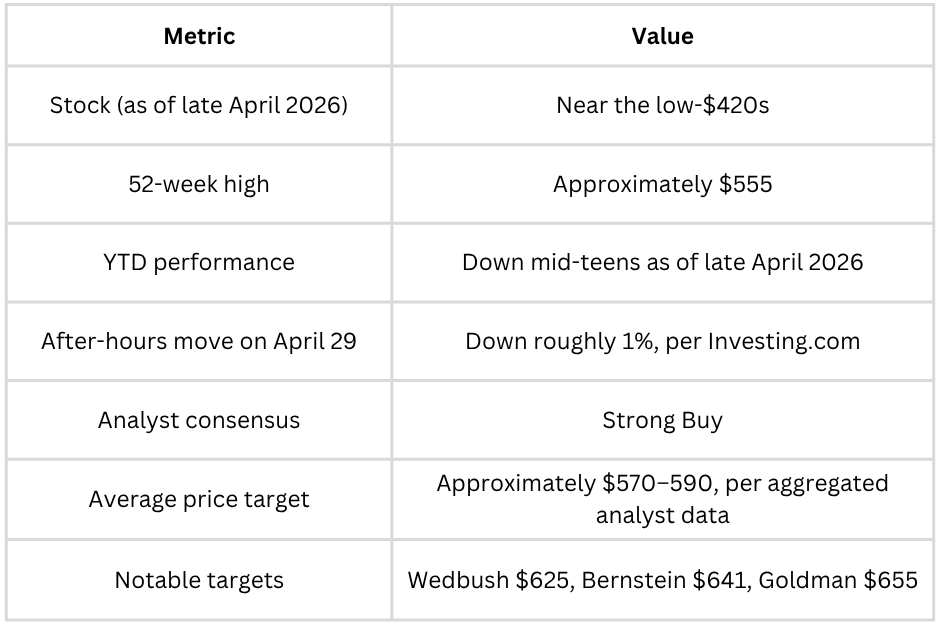

And yet the stock entered earnings down mid-teens year to date as of late April 2026, trading near the low-$420s, with analysts’ price targets averaging around $570. The market is fixated on a $190 billion capex bill and panicking. Investors who look past the spending to what it is building may find one of the more interesting setups in large-cap tech right now.

🔥 Top movers

Note: MSFT has underperformed the broader Nasdaq year-to-date through April 2026, weighed down by concerns about AI spending returns and the restructuring of its OpenAI relationship. Despite beating Q3 consensus on both revenue and earnings, the stock dipped after the results. The gap between strong fundamentals and a soft stock price is the central setup this article unpacks.

🍏 Current landscape

Microsoft is reporting into one of the most capital-intensive buildout cycles in technology history, and it is one of only three companies with the balance sheet to compete at the top.

The AI spending arms race is real and accelerating. Amazon, Alphabet, Meta, and Microsoft collectively guided toward roughly $725 billion in combined capital expenditure in 2026, per Bank of America estimates, after all four updated their forecasts in the same earnings week. The driver is not speculative capacity; it is genuine demand that is outpacing supply. CFO Amy Hood said on the earnings call that Microsoft expects to remain capacity-constrained on GPUs, CPUs, and storage through at least 2026, per CNBC. That is not a company building ahead of demand. That is a company struggling to build fast enough.

Memory and component prices have surged materially since late 2025. Hood attributed approximately $25 billion of the $190 billion 2026 capex guide to higher component pricing, per CNBC, a cost pass-through that is hitting every infrastructure provider simultaneously. Microsoft’s software-heavy revenue model means that while component costs are rising on the cost side, there is no meaningful tariff-driven supply chain exposure, the way hardware manufacturers face, a structural insulation that investors have started to notice.

Enterprise AI adoption has moved beyond experimentation to budget allocation. The $627 billion commercial remaining performance obligation, up 99% year over year, is the clearest evidence that large organisations are not testing Microsoft’s AI stack on monthly trials. They are making multi-year commitments. That is the most important number in the earnings release, and it is getting far less attention than the capex figure.

🏗️ What Microsoft actually sells now

Microsoft reports in three segments, and understanding which one is doing the heavy lifting matters more than most investors realise.

Intelligent Cloud is the engine. Azure and related services brought in $34.7 billion in Q3 FY2026, up 30% year over year, per the company’s earnings release. Azure specifically grew 40%, clearing the roughly 39% analysts had expected, per CNBC. This segment is running at a scale that puts it in direct competition with Amazon Web Services and Google Cloud.

Productivity and Business Processes are the flywheel. This segment, Office, LinkedIn, Dynamics, generated $35 billion in Q3, up 17% year over year, per Microsoft’s investor release. The key metric is no longer just Office seats. It is the Copilot attach rates. M365 Copilot now has over 20 million paid commercial seats, up from 15 million in January, and CEO Satya Nadella said on the earnings call that weekly engagement is approaching Outlook-like levels, per earnings commentary. That is a habit formation signal, not a vanity metric.

More Personal Computing, Windows, Xbox, Surface, Search, brought in $13.2 billion, down about 1% year over year. It is the legacy anchor. It matters for cash generation, not for the growth thesis.

The throughline: artificial intelligence is now embedded deeply enough to show up in the revenue numbers, not just in the product announcements. Microsoft Cloud revenue hit $54.5 billion for the quarter, up 29% year over year, per company filings.

🌀 Turning the tables

How is Microsoft repositioning from a productivity software vendor into a full-stack AI infrastructure and applications company?

Copilot is a new billing layer on top of everything Microsoft already owns

The Copilot story is more interesting than the seat count suggests. At roughly $30 per user per month, 20 million seats implies an annualised revenue stream of around $7 billion at US list prices, sitting on top of the existing M365 subscription base. But the more important dynamic is the shift toward agentic computing, AI agents that autonomously perform multi-step tasks rather than just answering questions. GitHub Copilot is moving from flat-fee subscriptions to a token-based consumption model starting June 2026, per GitHub’s official blog. The reason: agentic workflows consume dramatically more compute than simple code completions, and the old pricing model was not sustainable at the usage levels being generated. That shift mirrors what AWS did when it moved from reserved to pay-per-use, and it is structurally more valuable per power user over time.

Azure as the default infrastructure layer for the agentic era

Azure is the compute layer beneath most AI applications being built by enterprises globally. The $627 billion commercial RPO is the clearest signal: large enterprises are making multi-year commitments, not running experiments on monthly contracts. Cosmos DB, Microsoft’s cloud database product, grew 50% year over year, per earnings commentary. LinkedIn’s agentic products in talent solutions have crossed $450 million in annualised run rate, per management on the earnings call. AI monetisation is spreading across the entire platform, not concentrating in a single product line.

The OpenAI restructuring is a strategic clean-up, not a retreat.

Microsoft and OpenAI restructured their deal on April 27, ending the exclusive Azure lock-in, per CNBC. OpenAI can now serve customers on any cloud. But the new terms confirm Microsoft remains OpenAI’s primary cloud partner, and OpenAI products will ship first on Azure unless Microsoft cannot or chooses not to support the required capabilities. Microsoft retains a non-exclusive licence to OpenAI IP through 2032 and remains approximately a 27% diluted shareholder in OpenAI, per company filings. The market read this as weakness. The more accurate read: Microsoft exchanged exclusivity, which was always going to face regulatory scrutiny, for a long-term preferred-partner structure plus a large equity stake in the world's most valuable AI company. That is a cleaner position, not a lesser one.

Want to add Microsoft to your portfolio? Trade $MSFT directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

✨ What is working?

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.