Marvell (MRVL): the second name in AI’s custom-silicon duopoly

Five years ago, analysing Marvell meant counting hard-drive controllers and tracking which carrier had picked its 5G base-station chips. Not anymore. The company has reshaped itself into a designer of custom AI accelerators and the optical plumbing that ties hyperscale data centres together, to the point where one end market now drives three-quarters of revenue. When Nvidia’s CEO points at your stock on stage and calls it the next trillion-dollar company, the old spreadsheet no longer fits. That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors who know Marvell at all still file it under “networking chips,” a solid mid-cap that made transceivers and storage controllers. That label is now badly out of date. Today’s Marvell sits inside almost every large AI cluster being built, supplying two things those clusters cannot run without: custom silicon co-designed with the cloud giants, and the high-speed optical and switching components that move data between tens of thousands of chips. It is the smaller of the two companies that, between them, design the overwhelming majority of the world’s custom AI accelerators. The market spent most of the last year repricing that reality, and the stock more than tripled. The question now is not whether Marvell has become essential infrastructure. It has. The question is whether a valuation that assumes years of flawless execution leaves any room for what usually goes wrong in semiconductors.

🧩 What Marvell actually does today

Marvell is a fabless chip designer, meaning it designs the silicon and hands manufacturing to TSMC. Its products are the connective tissue of a data centre rather than the headline processor. Three families matter most.

The first is interconnect: the optical digital signal processors, coherent modules, retimers, and silicon photonics that move data between servers and between racks at 800 gigabits per second and now 1.6 terabits per second. As AI clusters grow from thousands of chips to tens of thousands, the volume of traffic between those chips grows faster than the chip count itself, which is why this is Marvell’s largest and fastest-growing product line within the data centre.

The second is switching: Ethernet switch silicon, such as the Teralynx family, that routes traffic, including a 102.4-terabit-per-second switch chip aimed at next-generation AI clusters, per Marvell’s product disclosures.

The third, and the reason the stock re-rated, is custom silicon: application-specific chips that Marvell co-designs with a hyperscaler to run that customer’s own AI workloads. Marvell supplies the design expertise, the intellectual property, and the advanced packaging know-how; the customer gets a chip tuned to its software rather than a general-purpose GPU.

Around that core sit storage controllers, Fibre Channel adapters, and the remaining carrier and enterprise networking business. Marvell has been deliberately narrowing its focus toward the data centre. In August 2025, it sold its automotive Ethernet business to Infineon for $2.5 billion in cash, per Marvell’s announcement, and in February 2026, it closed two acquisitions, Celestial AI (optical “photonic fabric”) and XConn (CXL switching), to deepen the interconnect roadmap, per its Q1 FY2027 filing.

For Indian readers, there is a direct connection most people miss: India is one of Marvell’s largest engineering bases. In a 2025 interview, the company said more than 20% of its global workforce sits in design centres in Pune, Bengaluru and Hyderabad, working on custom ASIC design, advanced process nodes and photonics. India is an R&D engine for Marvell rather than a sales market, but a meaningful share of the chips inside the global AI buildout is being designed by engineers in those three cities.

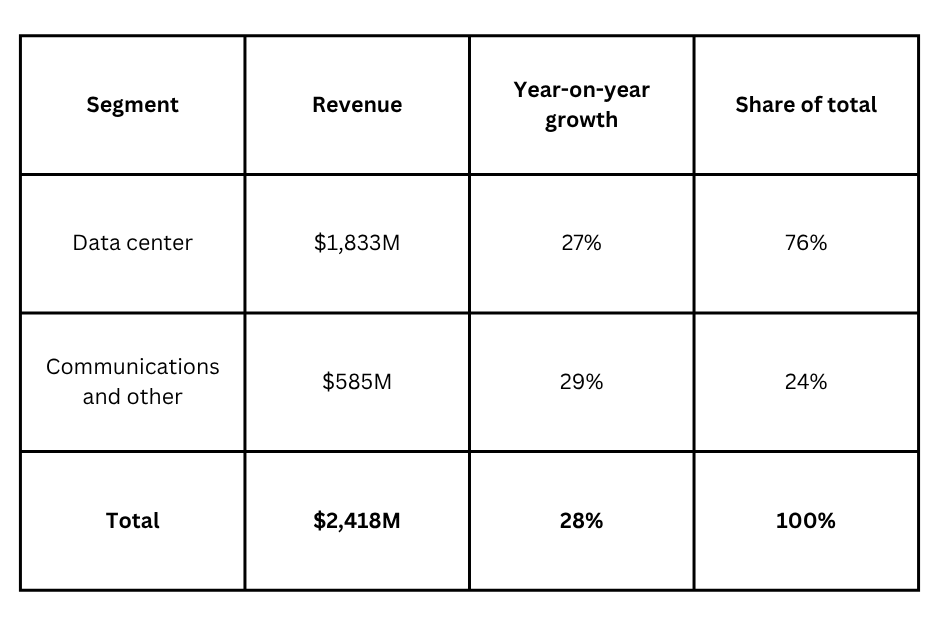

📊 The segment breakdown: one engine doing the work

Marvell now reports in two buckets, Data centre and Communications and other, having retired its older five-market split as the portfolio shifted. The concentration is the story.

Revenue by segment, Q1 fiscal 2027 (quarter ended 2 May 2026):

Source: Marvell Q1 FY2027 earnings release (27 May 2026). Figures are management-reported.

Within the data centre line, Marvell does not break out each product family by dollar amount every quarter, but management has described the order of importance: interconnect is the largest and fastest-growing segment, followed by switching, then custom silicon. The within-segment growth rates management gave for the current fiscal year are striking, and are guidance rather than reported results: interconnect revenue expected to grow more than 70% (raised from a prior 50%), switching products scaling toward a roughly $1 billion annualised run rate, and the data centre segment as a whole growing around 50%, per Marvell’s Q1 FY2027 call.

The full-year trajectory shows how fast the shape has changed:

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.