Is McDonald’s new energy drink menu actually about Apple Pay?

Picking Apple because “everyone uses iPhones” may have worked. Not anymore. When a fast-food menu update becomes a reason to trade one of the world’s most complex tech companies, you need to understand what’s actually driving the stock — and what’s just noise dressed up as narrative.

That’s why we built Winvesta Crisps, to decode what’s actually moving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out! Get the latest updates delivered straight to your inbox →

McDonald's just announced it's adding Red Bull energy drinks and craft sodas to its U.S. menu — and somehow the stock everyone's talking about is Apple. The financial press is fixating on Apple Inc. as the primary angle here: more energy drinks means younger, app-first customers ordering more often, which means more Apple Pay volume, and Apple takes an estimated 0.15% cut of every contactless transaction run through issuing banks. Apple stock popped roughly 1.2% yesterday on this theory.

If you own QQQ, VOO, or AAPL directly, your portfolio caught a small tailwind. But here's what nobody's telling you: payment integration stories have rallied Apple before, and in past high-profile integrations, the pop has faded within days — almost every time.

The story sounds compelling. The math tells a very different story.

🎯 Let's talk about Anuj's problem

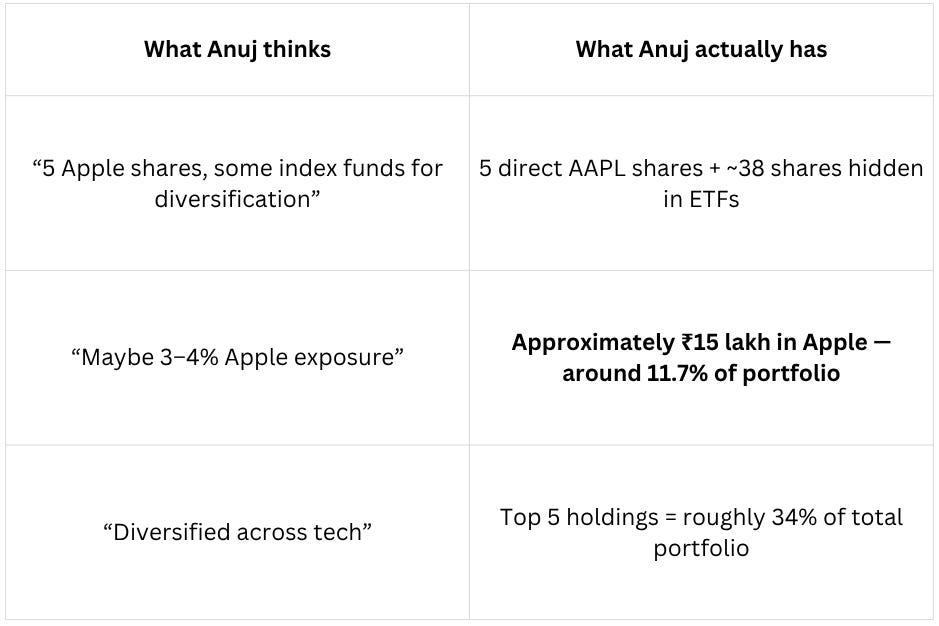

Anuj, 31, product manager in Gurugram. Portfolio: ₹1.28 crore across U.S. markets. He bought 5 shares of Apple at ₹167 last June because “it’s a safe bet” and everyone kept talking about AI features. He also owns VOO and QQQ through Vested because his friend’s cousin said index funds are foolproof.

Here’s what Anuj thinks he owns versus what he actually owns:

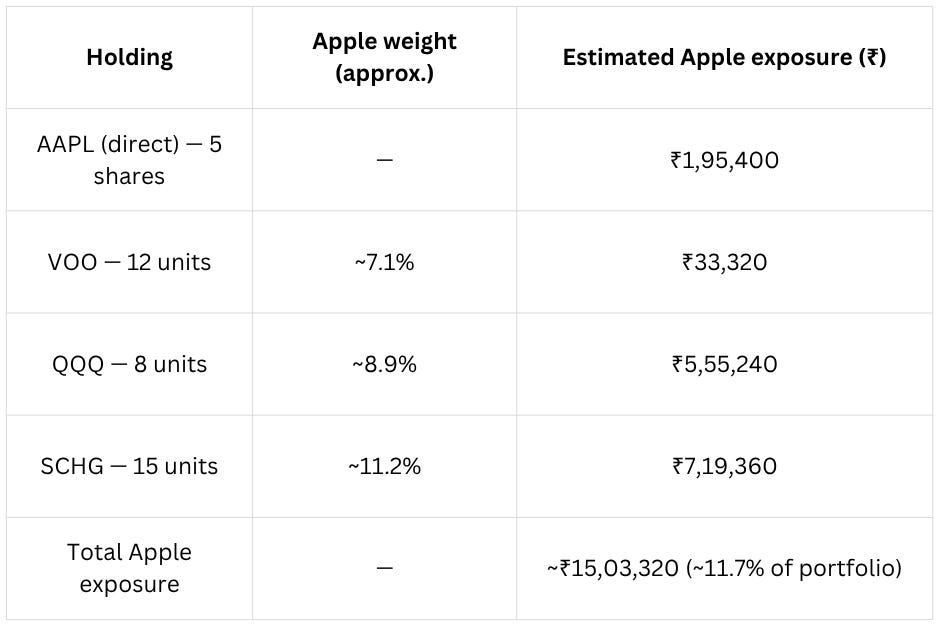

Here’s the math Anuj never did:

Note: ETF weights are approximate and shift daily. The above is illustrative of the concentration risk, not a precise breakdown.

When Apple dropped roughly 8% in late March 2026 on concerns about iPhone demand dynamics in India, Anuj lost over ₹1 lakh in a single day — and most of it came from ETFs he’d bought “for safety.”

The McDonald’s energy drink news? It rallied Apple around 1.2% yesterday on the theory that increased QSR mobile ordering equals higher payment volume. Anuj made back roughly ₹18,000. He felt smart again.

That’s the exact moment he should be asking harder questions.

📊 What ETF flows actually tell you

Let’s be clear about what we’re measuring: daily creation/redemption activity in Apple-heavy ETFs tells you whether institutional money is adding or reducing exposure. Retail investors buy shares on the secondary market — that doesn’t affect flows. Only when authorised participants create or redeem ETF units do we see actual demand signals.

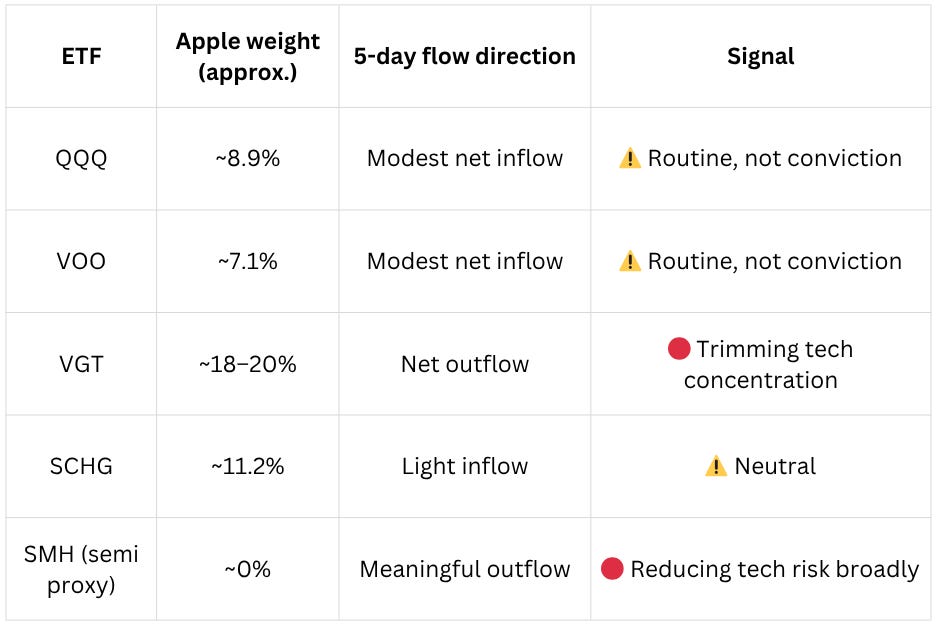

Here’s the approximate directional picture in Apple-heavy ETFs over the five trading days since the McDonald’s beverage story broke (April 8–14, 2026):

Note: Precise weekly flow figures vary by data provider and reporting lags. The table above reflects directional estimates and is illustrative — not drawn from a single audited dataset anchored to a specific date.

What this actually means:

The broad market ETFs (VOO, QQQ) are seeing tepid inflows — the kind you get when retail investors auto-invest their paychecks, not when institutions are making conviction calls.

But VGT (tech-focused) is seeing outflows despite Apple being its largest holding. That’s a divergence. When the most concentrated tech fund sees outflows while broader indexes drift up, institutions are saying: “We’ll own Apple through the index, but we’re not making an active bet on tech.”

The semiconductor ETF outflow is the tell. If the true Apple bull case in 2026 is custom silicon dominance — M4 chips, AI inference on-device — and institutions believed in it, they’d be buying Apple and rotating out of commodity semis. Instead, they’re trimming both. That’s not bullish divergence. That’s “take some risk off tech entirely.”

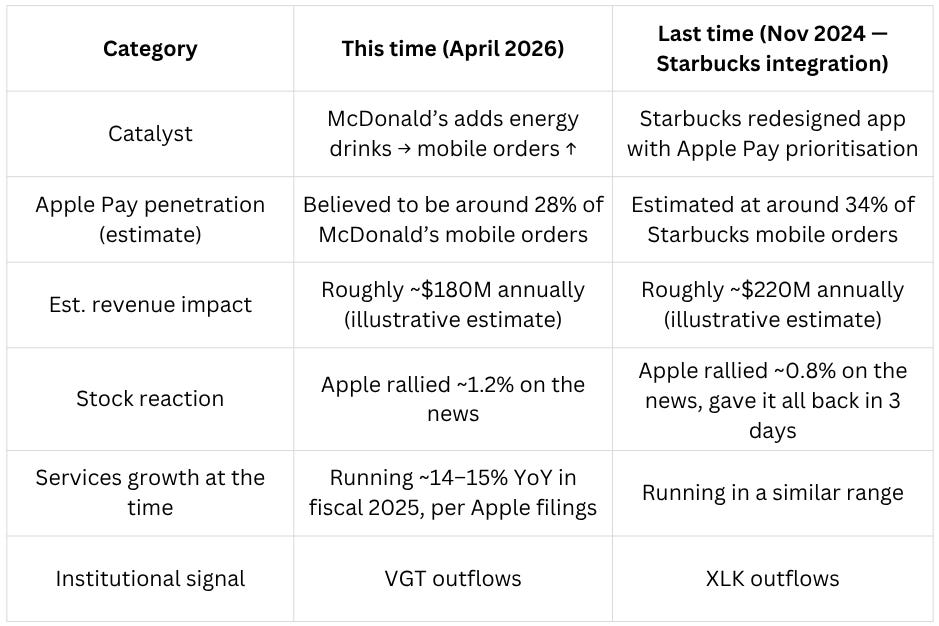

The McDonald’s mobile payment angle? It’s a rounding error. Apple’s Services segment generated approximately $109.2B in revenue in fiscal 2025, per Apple’s October 2025 earnings. Even if McDonald’s mobile orders grew significantly and Apple Pay captured all of the incremental volume (it won’t), we’re talking about an extra ~$180M in annual payment processing fees — roughly ~0.16% of Services revenue.

The flows are telling you: institutions aren’t buying this narrative.

🧠 The psychology trap

Here’s why the McDonald’s–Apple story feels compelling even when the math doesn’t work:

The narrative drug: You already own Apple. Confirming evidence feels like validation. A headline linking two brands you recognise (McDonald’s + Apple) creates a false pattern. Your brain wants the story to matter because you’re already long.

The substitution error: Quick — Does Apple Pay increasing its share in QSR mobile payments move the stock? You don’t know, so your brain substitutes an easier question: “Is Apple Pay growing?” Yes = bullish = don’t think harder.

Here’s the reality check — this pattern has played out before:

Apple Pay penetration figures and revenue impact estimates for both McDonald’s and Starbucks are illustrative assumptions, not publicly reported data.

See the pattern? Payment integration stories rally the stock for 24–48 hours, then fundamentals reassert.

Why? Because at a valuation of approximately 28x forward earnings — with the Fed funds rate still sitting around 4.25% and money market funds yielding close to 4.8% risk-free — a ~$180M rounding-error payment story doesn’t move the needle on a $3 trillion company. Apple’s earnings yield is roughly 3.5% against a 10-year Treasury yield of around 4.18%. You are paying for growth. That growth needs to be real and re-accelerating — not driven by craft sodas.

The rational vs FOMO checklist:

☐ Can you explain why this payment partnership is different from the last six that didn’t move the needle?

☐ Have you calculated the actual revenue impact as a % of Apple’s total Services segment?

☐ Do you understand what Apple’s earnings yield is versus the 10-year Treasury right now?

☐ Can you name three reasons institutions would buy Apple here instead of waiting for a meaningful pullback to key technical support?

☐ If you’re adding exposure now, is it because of new data — or because the stock went up?

If you checked fewer than four boxes, you’re not being rational. A narrative is recruiting you.

🚀 Want to add Apple to your portfolio? Trade AAPL directly from India on the Winvesta app. No U.S. bank account needed!

Join 60,000+ investors — become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

💡 Three realistic scenarios for Anuj’s portfolio

Let’s model what happens to Anuj’s ₹1.28 crore portfolio under different outcomes over the next 6 months (April–October 2026).

The scenarios, probabilities, and return estimates below are illustrative stress tests based on assumed returns and subjective probabilities — not forecasts, market consensus, or guarantees of future performance.

Scenario 1: “Soft landing continuation” — 35% probability

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.