Intel (INTC): The comeback trade hiding inside America’s semiconductor crisis

Everyone thinks Intel is a fading CPU company. It’s not. It’s a bet on whether the West can manufacture advanced semiconductors independently of Taiwan—backed by $8.5 billion in direct government funding, a foundry strategy that didn’t exist four years ago, and a process node roadmap that could match TSMC by 2025. The company is burning cash, cutting thousands of jobs, and losing the AI training race to Nvidia. And yet: Intel is the only company on Earth trying to simultaneously design leading chips, manufacture them domestically, and sell foundry services to competitors. That combination is either the most audacious turnaround in semiconductor history or the most expensive failure. Here’s why the answer hinges on three sentences in Intel’s next earnings call—not the headline numbers.

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in your spam folder.

The full-stack chipmaker, explained 🧩

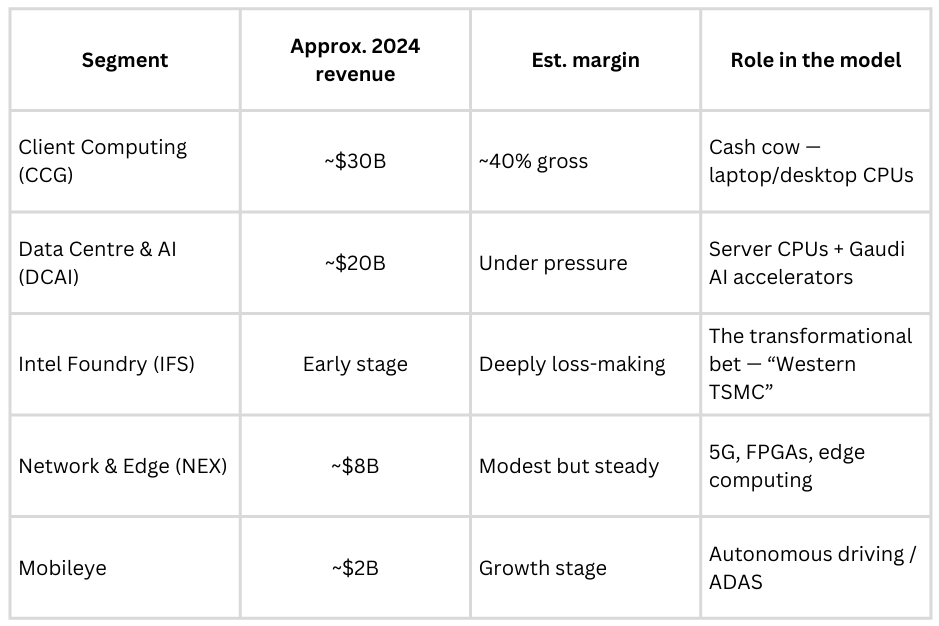

Intel doesn’t make most of its money from a single product anymore. It makes money across five distinct semiconductor businesses—each with different growth trajectories, margin profiles, and competitive dynamics.

Client Computing remains the largest segment—laptop and desktop CPUs that powered computing for decades. But PC volumes declined sharply in 2023 before stabilising in 2024, and the segment faces structural headwinds as cloud computing reduces PC dependency. Margins are still relatively strong, but growth has stalled.

Data Centre & AI was once Intel’s growth jewel,l but has faced brutal competition. Intel’s Xeon server chips still dominate traditional workloads, but AMD’s EPYC processors have grabbed meaningful market share, while Nvidia’s GPUs captured the AI training market almost entirely. Intel’s Gaudi AI accelerators launched as a response, targeting inference workloads at lower price points. CoreWeave’s rise underscores the problem: hyperscalers are buying Nvidia, not Intel, for AI infrastructure.

Intel Foundry Services is the transformational bet. Formally launched in 2021, IFS aims to turn Intel into a contract chip manufacturer for third-party U.S. customers. The US government is backing this with $8.5 billion in CHIPS Act direct funding (plus additional loans and tax credits), viewing Intel as strategically vital for domestic semiconductor supply. Intel is building fabs in Arizona, Ohio, and Germany. The economics are gruelling: foundry margins typically run 20–30% versus Intel’s historical 60%+. But if Intel hits its 18A process node targets—potentially matching TSMC’s 3nm class—it could attract major fabless customers.

Network & Edge covers networking chips, FPGAs (via the Altera unit), and edge computing products. Growth here is modest but steady, driven by 5G infrastructure and IoT deployments.

Mobileye, Intel’s majority-owned autonomous-driving subsidiary, generates about $2 billion annually by selling advanced driver-assistance systems to 50+ automakers. It holds leadership in camera-based systems, though Tesla’s in-house approach and Nvidia’s DRIVE platform pose competitive threats.

In other words, “Intel” is now a diversified semiconductor conglomerate trying to own the full stack—design, manufacturing, and AI acceleration—not just the CPU incumbent clinging to legacy markets.

Altera and programmable chips: The quiet growth engine 🕵️♀️

One of Intel’s most defensible franchises sits far from the CPU and GPU headlines: field-programmable gate arrays (FPGAs).

Intel acquired Altera in 2015 for $16.7 billion, then attempted to integrate it—a decision that fully stifled growth. In 2024, Intel spun Altera back into a standalone business unit, taking investment from external partners. FPGAs are reprogrammable chips used in telecom infrastructure, aerospace, and AI inference acceleration. Altera competes primarily with AMD’s Xilinx division. The FPGA market is growing at an estimated 8–10% annually, driven by 5G base stations and edge AI applications where flexibility matters more than raw performance.

Defence and aerospace: Altera holds significant design wins in military systems, where supply chain security and U.S.-based manufacturing matter. Intel’s Ohio fabs will produce Altera FPGAs domestically—a key selling point for defence contractors. This segment generates roughly $2 billion annually with approximately 35% gross margins—lower than historical Intel levels but higher than foundry economics.

“Programmable acceleration” positioning: Intel frames Altera as complementary to its CPU and accelerator lines, enabling customers to optimise workloads with tailored logic. In data centres, FPGAs accelerate tasks like video transcoding, financial modelling, and network packet processing—niches where GPUs are overkill.

This segment is profitable, defensible, and tied to secular growth in 5G and edge computing—very different economics from the capital-intensive foundry bet. For Amazon, it was advertising hiding inside e-commerce. For Intel, Altera could be the stable-margin engine hiding amid the turnaround chaos.

Want to add Intel to your portfolio? Trade INTC directly from India on the WinU.S.sta app. No US bank account needed.

🚀 Join 60,000+ investors — become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

AI infrastructure: Threat meets opportunity 🌪️

CoreWeave’s anticipated results—and the implied volatility in its options—reflect frenzied demand for AI compute. For Intel, this boom is both an existential threat and a potential salvation.

The Nvidia problem: AI training workloads overwhelmingly run on Nvidia GPUs. CoreWeave, Lambda Labs, and other GPU cloud providers buy H100S and H200S at $30,000+ per unit, generating tens of billions for Nvidia. Intel missed this wave. Its Gaudi 2 accelerators launched late and lack the CUDA software ecosystem that locks developers into Nvidia. As of 2024, Intel’s AI accelerator revenue was estimated at under $1 billion—a fraction of Nvidia’s data centre segment, which runs in the tens of billions annually.

The inference opening: AI workloads are split into training (upfront model building) and inference (ongoing predictions). Industry analysts widely project that inference will account for the majority of total AI compute over time, and that it favours cost-efficiency over raw performance. Intel claims its Gaudi 3, shipping in 2025, targets this at roughly half the price of Nvidia equivalents for comparable inference throughput. Amazon already uses Gaudi in some AWS instances. If those economics hold up at scale, Intel could capture budget-conscious hyperscalers—but CUDA lock-in remains the barrier.

Edge AI and the PC renaissance: Intel sees AI reviving PCs through “AI PCs”—laptops with neural processing units (NPUs) for local inference. Microsoft’s Copilot+ initiative and generative AI apps running on-device could drive refresh cycles. Intel’s Meteor Lake chips, launched in 2024, integrate NPUs capable of 34 TOPS (trillion operations per second). If enterprises upgrade fleets for AI capabilities, CCG could return to growth.

For a firm that monetises both chip sales and foundry services, AI’s infrastructure boom means painful displacement in data centres but fresh revenue streams in inference and edge—if execution lands.

Process leadership: The 18A bet 🤖

Intel is not just riding industry trends—it is attempting to leapfrog TSMC technologically through brute-force R&D and capital spending.

18A process node: Intel’s 18A node, targeting production in 2025, represents a bet-the-company milestone. It combines two innovations: RibbonFET (Intel’s take on gate-all-around transistors) and PowerVia (backside power delivery). If successful, 18A could match or exceed TSMC’s N2 node in transistor density and power efficiency. Intel has publicly committed to regaining process leadership by 2025, and 18A is the proof point. Early silicon is reportedly sampling to potential foundry customers, with industry reports linking discussions to names like Broadcom and Qualcomm—though no confirmed high-volume production deals have been announced.

Intel 3 and Intel 4: These intermediate nodes—shipping in 2023–2024—restored Intel’s ability to deliver on roadmaps after years of delays. Intel 4 powers Meteor Lake, while Intel 3 targets server chips. They’re not industry-leading but demonstrate improved execution under the “five nodes in four years” plan.

Foundry 2.0 strategy: To win the foundry business, Intel adopted TSMC’s playbook: modular IP, standardised design flows, and partnership with Synopsys and Cadence for EDA tools. Intel also created a separate P&L with “fair and transparent” pricing, keeping its product divisions at arm’s length from foundry operations. The US military has already contracted Intel for secure chip production under the RAMP-C programme, valuing geopolitical reliability.

Process leadership is both a competitive moat for Intel’s own products and a credibility threshold for attracting third-party foundry customers—it can’t succeed at one without the other.

The financials: Transition pain in the numbers 📊

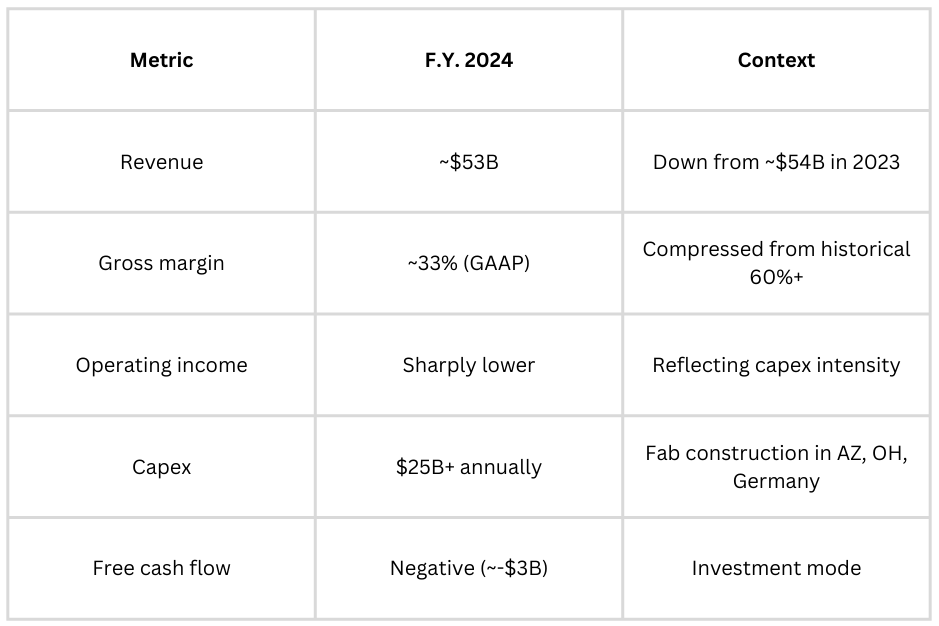

Under the hood, Intel’s financials increasingly resemble a company in transition, sacrificing near-term profitability for long-term positioning.

Intel reported approximately $53 billion in revenue for 2024, down slightly from approximately $54 billion in 2023. Gross margin compressed to around 33%, reflecting mix shift toward lower-margin businesses (foundry, AI accelerators) and competitive pricing pressure in its core markets. This is a dramatic decline from the 60%+ gross margins Intel enjoyed in its prime—and it reflects the cost of transformation, not just competitive weakness.

Foundry losses: Intel Foundry Services is currently unprofitable, with analysts estimating losses of roughly $3 billion in 2024—on top of a disclosed $7 billion operating loss in 2023—as Intel builds capacity ahead of demand. Management frames this as an investment, not a structural weakness, arguing that once fabs reach approximately 70% utilisation, foundry margins will inflect toward 30%—the industry standard for contract manufacturers.

Cost discipline and restructuring: In 2024, Intel cut roughly 15% of its workforce (about 15,000–18,000 roles) and suspended its dividend to preserve cash. These moves, painful but necessary, aim to deliver over $10 billion in annual cost savings by 2025. The dividend suspension alone signals how seriously management views the cash flow pressure.

For investors, Intel is evolving from a cash-generating monopoly into a capital-intensive, diversified semiconductor platform with binary outcomes tied to process node execution.

Someone shared this with you? If this changed how you see Intel, pass it on.

The competitive picture 🏛️

The full-stack model only works if Intel can compete on multiple fronts simultaneously. Can it?

Foundry: TSMC commands over 50% of global foundry revenue and manufactures for Apple, Nvidia, AMD, and Qualcomm. Intel’s IFS is starting from near-zero revenue, while a competitor has decades of customer trust and yield expertise. Samsung Foundry, the only other credible competitor, has struggled with yields on its 3nm GAA process. Intel’s advantage iUSS. locationUSS. fabs with government backing) and integration (it can co-optimise chip design and manufacturing). The disadvantage is credibility—Intel has to prove it can run fabs for outside customers, not just itself.

CPUs: AMD’s EPYC processors have taken meaningful server market share, and ARM-based chips from AWS (Graviton), Apple (M-series), and Qualcomm are pressuring Intel’s x86 dominance from a different architectural direction. Intel’s Xeon still holds the majority of the installed server base, but growth is elsewhere.

AI accelerators: Nvidia’s CUDA ecosystem creates extraordinary lock-in. Even if Intel’s Gaudi offers competitive inference price-performance, developers default to Nvidia because the software tools are mature and ubiquitous. AMD’s MI300X is a more credible Nvidia challenger in the near term. Intel’s path is the budget tier—capturing inference workloads where cost matters more than peak performance.

FPGAs: Altera vs AMD’s Xilinx is a genuine duopoly. Intel’s ability to offer FPGAs manufactured in U.S. fabs gives it a defence/aerospace advantage. This is Intel’s most defensible competitive position.

The moat isn’t one thing. It’s the combination of design capability, manufacturing capacity, government backing, and geographic diversification that no other single company can replicate—even if each piece faces fierce competition.

What it means for your portfolio 📈

“Owning the chipmaker” in a bifurcated semiconductor market

Intel trades at a fraction of Nvidia’s valuation and well below AMD on most metrics. That discount reflects real execution risk—but also prices in very little upside if the turnaround works.

Geopolitical hedge: As U.S.-China tensions escalate, Intel represents the West’s primary opportunity to onshore advanced semiconductor manufacturing. TSMC’s Taiwan location is a geopolitical single point of failure; Intel’s Arizona and Ohio fabs mitigate that risk. The $8.5 billion in CHIPS Act direct funding (plus loans and tax credits) reduces Intel’s capital burden—effectively socialising some of the downside.

Structural cost position: Intel’s integrated model—designing and manufacturing its own chips—historically delivered superior margins. If Intel successfully operates IFS as a foundry while designing leading chips internally, it gains optionality: manufacture for itself or third parties, optimising fab utilisation. TSMC can’t design chips; fabless firms like AMD can’t manufacture. Intel’s hybrid model is theoretically superior—if execution improves.

Binary outcomes: Intel touches AI at several layers: CPUs for general compute, Gaudi accelerators for inference, FPGAs for programmable logic, and foundry services for producing others’ AI chips. This diversification means Intel isn’t a pure-play bet on any single trend but rather a portfolio of semiconductor exposures. The 18A node is the hinge point—success validates the technological resurrection, while failure cements decline into a subscale manufacturer.

This isn’t a safe dividend stock. It’s a turnaround with asymmetric payoffs: either Intel reclaims competitiveness and the stock re-rates dramatically, or the foundry bet fails, and the legacy business slowly erodes. The risk-reward is what makes it interesting—not the certainty.

The risk check ⚠️

No turnaround is guaranteed. Here’s what could go wrong.

Process node execution risk: Intel’s credibility hinges on delivering 18A on time and at performance parity with TSMC. Any delay or yield issues would validate sceptics who argue that Intel can’t compete technologically, spook potential foundry customers and prolong margin pressure.

NVIDIA’s AI moat: CUDA’s software lock-in means developers default to NVIDIA for AI workloads. Even if Gaudi offers better price-performance, switching costs are high. Intel risks remaining a niche player in AI acceleration, limiting its participation in the decade’s defining compute shift.

Foundry customer wins: IFS needs marquee customers to validate its model. So far, Intel has announced partnerships, but few confirmed high-volume production deals. If foundry revenue stalls below $5 billion by 2027, the investment case weakens significantly.

Cyclical downturn: Semiconductor markets are notoriously cyclical. A broader economic slowdown or AI spending pullback could hit Intel’s recovering data centre business and delay foundry ramps, stretching cash flow stress.

Subsidy and political risk: Intel’s reliance on $8.5 billion in government grants introduces political risk. Changes in administration or budget pressures could reduce funding, increasing Intel’s capital burden at exactly the wrong moment.

These risks don’t negate the thesis, but remind investors that even strategically vital chipmakers face existential execution challenges in a market where technology leadership determines survival.

The final word 🏁

Intel is attempting something rare: a full-stack comeback in an industry where leadership, once lost, rarely returns. The company is no longer just a CPU incumbent but a diversified play on AI inference, edge computing, programmable logic, and geopolitically vital foundry capacity. The 18A node is the hinge point—success validates Intel’s technological resurrection, while failure cements its decline. CoreWeave’s AI infrastructure boom underscores both the opportunity (massive compute spending) and the challenge (Nvidia’s dominance). For investors, the calculus is binary: either Intel regains competitiveness and delivers foundry-scale, or it becomes a shrinking legacy player subsidised by government grants. The stock isn’t for those seeking safe income—it’s for those willing to bet on execution, government backing, and the strategic imperative that the West cannot remain dependent on Taiwan for its most critical technology.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The views expressed are those of the author. Always conduct your own research before making investment decisions. Winvesta Technologies Pvt Ltd does not recommend buying, selling or holding any securities.