India’s manufacturing moment: Opportunity, hype, or both?

Every investor with exposure to US tech has heard the phrase “China plus one.” Most assume India is the obvious winner. The reality is considerably more interesting: India is genuinely capturing some of the biggest supply chain shifts in a generation, while simultaneously struggling with structural gaps that Vietnam, Mexico, and others are exploiting. Understanding the difference between the real opportunity and the overstated narrative is the edge.

That’s why we built Winvesta Crisps, to break down what’s actually moving markets, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Apple reportedly chartered cargo aircraft to airlift iPhones out of India in the weeks before new US tariffs took effect in March 2025, becoming one of the year's most widely reported supply chain sprints. That single image tells you more about India’s manufacturing story than any policy announcement: the country has become real enough, fast enough, that the world’s most valuable company is betting its US-market supply chain on Indian factories.

And yet, the same India that assembled a quarter of the world’s iPhones in 2025 controls just 2.8% of global manufacturing output, per available estimates. By comparison, China controls approximately 28.8%. The gap between the headline wins and the structural reality is the most important thing an investor needs to understand about India’s manufacturing moment right now.

This is not a story about whether India will eventually become a major manufacturing hub. It probably will. It is a story about what is actually happening today, what is still five years away, and how the gap between those two things affects the companies you own, the currency you hold, and the returns you take home.

How India became the name on every CEO’s lips🏭

Three shocks broke China’s manufacturing dominance in rapid succession and pushed India into every boardroom conversation:

The 2018-2019 US-China trade war showed that political decisions could overnight make Chinese-made goods uncompetitive for US markets

COVID-19 exposed how fragile single-country supply chains were when a factory cluster goes offline

Liberation Day (April 2, 2025) imposed sweeping tariffs on Chinese goods, turning “diversify away from China” from aspiration into an urgent operational priority

India was already positioning. Key policy moves that made it a credible destination:

The PLI scheme: 14 strategic sectors, ~$26 billion outlay, 836 approved applications, committed investments crossing INR 2.16 lakh crore, per Ministry of Commerce data (December 2025)

PM Gati Shakti: dedicated freight corridors, industrial corridors, and port upgrades layered on top

The results are measurable:

$81 billion in total FDI in FY 2024-25, up 14%, per DPIIT provisional data; manufacturing FDI grew 18% to $19 billion

iPhone exports from India crossed INR 2 lakh crore in FY26, India’s single largest branded export

India now assembles roughly 25% of global iPhone output, up from 18% in 2024, per Counterpoint Research.

The February 2026 US-India interim trade deal added a geopolitical tailwind: a US reciprocal tariff on Indian goods cut from 25% to 18%, more favourable than the 20%-plus rates faced by Vietnam and Bangladesh, with a broader Bilateral Trade Agreement in negotiation.

How “China plus one” actually works, and where India fits in 🔧

Moving production out of China is not a simple relocation. It is rebuilding an ecosystem: suppliers, logistics, skilled workers, component producers, and regulatory infrastructure that took China thirty years to assemble. Where India is genuinely ahead:

Labour costs among the lowest in Asia, roughly 30-40% cheaper than Vietnam for equivalent skill levels in many sectors, per DocShipper’s 2026 logistics analysis

Logistics costs have decreased from roughly 13-14% of GDP to approximately 8%, per logistics industry estimates, driven by freight corridors and port upgrades

A large domestic market means export factories can also serve domestic demand, de-risking the investment case

Where the honest picture is more complicated:

Domestic value addition in iPhone assembly is roughly 15-20% in India versus 40-45% in China, per industry estimates — India is assembling, not yet deep manufacturing

India’s goods trade deficit with China sits above $100 billion annually, with roughly 80%, per trade analysis, in electronics, machinery, organic chemicals, and plastics — the very components Indian factories need

The race is also multi-destination, not just India vs China:

Vietnam: $165 billion in electronics exports (2023), built on Samsung’s multi-decade investment

Mexico: 4-8 day road freight to US distribution centres versus 25-35 days by sea from India

Bangladesh, Indonesia, Thailand: all competing in specific categories

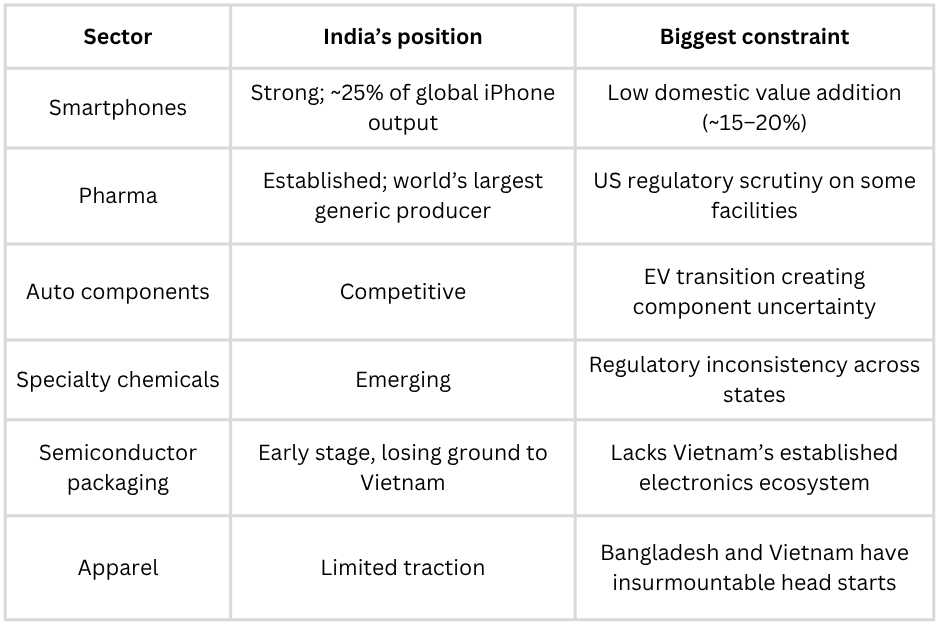

India’s strongest sectors: smartphone assembly, pharmaceuticals, auto components, speciality chemicals, select capital goods. India’s largest gaps: advanced semiconductor packaging (where Vietnam is currently pulling ahead), apparel, and high-precision electronics components.

India’s March 2026 amendment to Press Note 3, easing Chinese FDI restrictions into 40 manufacturing sub-sectors, is a pragmatic bet that building local component depth with Chinese partners is worth the dependency risk.

The dynamics covered in this article affect every US stock in your portfolio. Trade from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

The honest scorecard: Where India is winning and where it is struggling 📊

(Illustrative framework based on publicly available research. Not investment advice)

Three structural constraints cut across every sector:

Logistics still lag: port congestion, inconsistent inland freight, and state-level policy variation continue to create an “India cost” that erodes the labour advantage

Skill gaps are real: less than 5% of India’s workforce has formal vocational or technical training, according to published research, compared with more than 50% in South Korea, according to comparative labour studies.

Manufacturing’s GDP share has remained at approximately 16-17% for years despite sustained policy efforts; the 25% target requires structural reform well beyond PLI.

What this means if you’re an Indian investor holding US equities 🇮🇳

India’s manufacturing rise hits your portfolio in multiple directions simultaneously.

US stocks that benefit directly:

Apple: physically committed to Indian manufacturing at scale, with most US-bound iPhones targeting India assembly by end-2026

Contract manufacturers, industrial suppliers, and logistics names enabling the India supply chain transition

Defence and aerospace companies are benefiting from the US-India technology partnership under the bilateral framework

US stocks and sectors under indirect pressure:

Indian IT services face tighter discretionary tech budgets as US clients shift capex toward hardware and direct manufacturing investment; Liberation Day’s corporate planning disruption showed up in Indian IT order books within two quarters

Companies with high China-sourced component dependency still face tariff and supply chain costs that compress margins even as they build India capacity

Currency dimension:

India’s tariff resolution at 18% stabilises the rupee outlook versus the depreciation pressure of mid-2025, when India faced up to 50% US tariffs

But India’s $100 billion-plus annual trade deficit with China remains a structural rupee headwind that no US trade deal can directly fix.

The practical takeaway: the India manufacturing story does not have a simple “buy” or “sell” signal for a diversified investor. It is a reason to be sector-specific, not to treat “India” or “US tech” as homogeneous categories.

If this changed how you see India’s manufacturing story and what it means for your portfolio, share it with your investing circle.

What to watch: The signals that actually matter 🧭

Five signals tell you whether India’s manufacturing transition is on track or stalling:

Apple’s India output share: Counterpoint Research and PLI data track this quarterly. Progress toward 30-35% confirms the thesis; stalling below 25% means structural constraints are biting.

India-China goods trade deficit: if the deficit starts narrowing in electronics and machinery, domestic value addition is genuinely improving; if it keeps widening, India is primarily a finishing location, not an independent hub

US-India BTA negotiations: the interim deal locked in 18%, but the broader Bilateral Trade Agreement could deepen or complicate India’s tariff advantage, depending on agricultural and digital trade concessions

Manufacturing FDI quality: total FDI can look strong while being dominated by financial services and portfolio flows; watch DPIIT’s manufacturing-specific FDI line — if the $19 billion figure grows, the factory-building is real

Corporate earnings call language: every Apple, Foxconn-adjacent, or industrial supply chain earnings call now includes India production commentary; that guidance language leads any government data release by months

The bottom line 🏁

India’s manufacturing moment is real. The data confirms it:

Apple is building most of its US-market iPhones in India

FDI is rising, and the PLI scheme is generating measurable output

The US-India trade deal has given India a tariff edge over several competing destinations

And the honest framing is that this is the beginning of a decade-long transition, not the end of one:

Assembly is not the same as manufacturing depth

A 25% iPhone output share sits alongside a $100 billion-plus annual component import deficit from China

Vietnam leads in semiconductor packaging, Mexico wins US proximity, and Bangladesh and Vietnam dominate apparel

For investors, the right mental model: India captures a significant but differentiated share of global supply chain restructuring, concentrated in smartphones, pharma, auto components, and speciality chemicals, moving more slowly than headlines suggest in semiconductors and apparel.

The companies that benefit most are those positioned in India’s strongest sectors, not those exposed to categories where India’s structural gaps are widest. That distinction matters enormously when sizing positions or evaluating whether the India story is already priced into a specific holding.

By the numbers 📊

~25% of global iPhone output is now assembled in India, up from 18% in 2024, with Foxconn and Tata as the two primary manufacturers, per Counterpoint Research and government PLI data

INR 2 lakh crore (~$23 billion) in iPhone exports from India in FY26, making iPhones India’s single largest branded export item

$81 billion in total FDI into India in FY 2024-25, up 14% year-on-year, with manufacturing FDI growing 18% to $19 billion, per DPIIT provisional data

~$100 billion, India’s trade deficit with China in FY25, with roughly 80%, per trade analysis, concentrated in electronics, machinery, organic chemicals, and plastics, the very components Indian assembly lines depend on

18%, the US reciprocal tariff on Indian goods under the February 2026 interim trade deal, more favourable than the 20%+ facing Vietnam and Bangladesh, per White House joint statement

2.8% vs 28.8%, India’s and China’s respective shares of global manufacturing output, per available estimates, the gap that defines the gap between India’s current position and its stated ambition

16-17%, India’s manufacturing share of GDP, essentially flat for years despite sustained policy effort; the government’s target is 25%, a goal that requires structural reform well beyond the PLI scheme alone

$500 billion, India’s commitment to purchase US energy, aircraft, technology, and goods over five years as part of the bilateral trade framework, a measure of how much geopolitical alignment is now driving the economic relationship

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.