How index inclusion moves billions overnight

Every rupee sitting in a Nasdaq-100 fund, a QQQ position, or a broad US index ETF is partly managed by a rulebook rather than by a person. When a stock joins a major index, every fund tracking that index has to buy it, regardless of price, valuation, or whether anyone actually thinks it’s a good investment. SpaceX’s entry into the Nasdaq-100 this week forced exactly that: billions of dollars of automatic buying into a stock where almost none of the shares are available to trade. That mechanism sits quietly underneath a growing share of every Indian investor’s US portfolio, and understanding it changes how you read stock moves that otherwise look irrational. That’s why we built Winvesta Crisps: to break down what’s actually moving markets in plain language before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Before the opening bell on Tuesday, July 7, every fund tracking the Nasdaq-100 became a forced buyer of SpaceX stock. J.P. Morgan estimated automatic purchases of up to 4.3 billion dollars from the QQQ ETF alone, and as much as 27 billion dollars once every fund tracking the Nasdaq-100 and Russell indices was counted, landing on stocks where only 3 to 5% of shares actually trade freely. None of that buying happened because a portfolio manager decided SpaceX was cheap. It happened because a rulebook said so.

This is index inclusion, one of the least understood mechanics in modern investing. It operates quietly in the background of nearly every diversified portfolio, including Nasdaq-100 mutual funds and ETFs that hundreds of thousands of Indian investors use for one-tap exposure to Apple, Microsoft, and Nvidia. Most of the time it barely registers. Then a company the size of SpaceX joins overnight, and the scale of what these rules actually do becomes impossible to ignore.

How index investing quietly took over the market 📈

Passive investing was pitched as the boring option. Buy a fund that tracks an index, pay a low fee, and let the market do the work instead of trying to beat it. That pitch has been so successful that passive funds now own a genuinely large share of the market they were designed to simply mirror.

By 2024, the combined assets of passively managed mutual funds and ETFs in the US had overtaken those of actively managed funds for the first time. As of May 2026, indexed mutual funds and ETFs held $ 21.82 trillion, compared with $ 18.75 trillion in active funds, per Investment Company Institute data. Within US equities specifically, industry estimates put the passive share at somewhere around 60% of fund assets. Some academic research argues the true passive ownership share, once you count internal indexing by pension funds and closet indexing by active managers, runs higher still, though those estimates are contested.

None of this is a conspiracy. It is the direct result of decades of evidence showing that most active managers fail to beat their benchmarks after fees, and of investors voting with their money accordingly. But the side effect is mechanical: index funds do not decide what to buy. The index provider decides, through a published rulebook, and every fund tracking that index follows along, on the same day, at the same price, regardless of what any of that money actually thinks the stock is worth.

Mega IPOs are where this becomes visible. SpaceX went public on June 12, 2026, closing its first day of trading at a market capitalisation of roughly 2.1 trillion dollars, one of the largest listings in history. Historically, an IPO that size would sit outside every major index for up to a year, waiting to season and build a tradable float. Nasdaq changed that. Effective May 1, 2026, any newly listed company that ranks in the top 40 of the Nasdaq-100 by market cap can enter the index after just 15 trading days, with no minimum float requirement. SpaceX qualified almost the moment it started trading.

The mechanics: how a 3% float meets a 27 billion dollar order 🔧

Index inclusion sounds simple: a stock gets added, funds buy it. The scale of the numbers involved is where it gets genuinely strange.

Nasdaq-100 funds don’t buy a company at its full market capitalisation. They weight it by float, the portion of shares actually available for public trading, since that’s the only portion an index fund can realistically acquire. SpaceX’s total market cap on inclusion day sat above 2 trillion dollars, but with only 3 to 5% of shares in public hands, its float-adjusted value was a fraction of that headline number.

Nasdaq’s new methodology carried one unusual wrinkle: a weighting multiplier for low-float stocks, scaling up a large IPO’s float-adjusted weight by up to 3 times until its float ratio reaches 33.3%, according to Morningstar’s analysis of the rule change. Nasdaq built that multiplier so large new listings would be represented at something closer to their true economic size, rather than an artificially tiny weight simply because insiders haven’t sold yet. The side effect is that funds have to buy more of a stock than its tradable float alone would suggest, concentrating demand into an even smaller pool of shares. Total assets tracking the Nasdaq-100, across ETFs, mutual funds, and derivatives, exceed $ 1.4 trillion. SpaceX’s initial weight in the index still landed under 1%, since the float adjustment keeps even a 2-trillion-dollar company small on paper for now, but the mechanical buying still had to happen on schedule, all at once, at the market open.

The S&P 500 works differently, and the contrast is worth sitting with. In May 2026, S&P Dow Jones Indices opened a consultation on relaxing its own rules for megacap IPOs, shortening the 12-month seasoning period and waiving the requirement for four consecutive quarters of GAAP profitability. On June 4, it rejected its own proposal. All existing eligibility rules remained in place. That single decision means SpaceX cannot enter the S&P 500, where more than 11 trillion dollars in assets are benchmarked, until at least mid-2027, and only once it posts a full year of GAAP profits. Two of the world's most influential index providers looked at the same company and made opposite calls. Nasdaq is optimised to represent large companies as they actually are. S&P optimised for protecting index investors from unprofitable, unseasoned businesses. Neither choice is neutral, and both now sit permanently inside the fund you may already own.

This isn’t a new phenomenon, only a faster and larger version of an old one. When Tesla joined the S&P 500 in December 2020, the stock was already up more than 700% for the year, carrying a market capitalisation of over 600 billion dollars. Jefferies estimated at the time that funds needed to buy roughly 74 billion dollars worth of Tesla shares, about 118 million shares, equal to three days of its normal trading volume, on a single rebalance day. Tesla fell 6.5% on its actual first day in the index, as traders who had bought ahead of the event sold into the forced demand. Three years later, Tesla shares were up just 6.7% while the S&P 500 itself had climbed roughly 27%, per Bloomberg data, and Apartment Investment and Management, the stock Tesla replaced, outperformed Tesla by a wide margin over the following six months. Index funds tend to buy high. That isn’t a flaw hidden in the fine print. It’s how a market-cap-weighted index is built to work.

The dynamics covered in this article affect every US stock in your portfolio. Trade from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

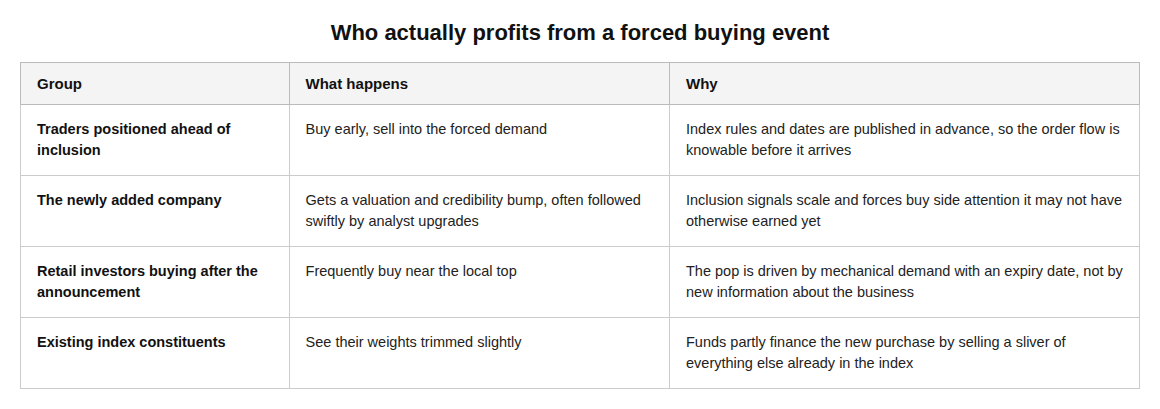

Who actually profits from a forced buying event 🏆

Forced buying creates predictable winners and a very predictable trap.

SpaceX was flooded with buy ratings from Stifel and RBC within hours of its inclusion in the index, a pattern that tends to accompany inclusion regardless of where the stock trades a year later. TradingKey’s market commentary this week noted that Palantir and Strategy, two other recent high-profile inclusions, both peaked around their respective inclusion dates before cooling off once the mechanical flow dried up.

SpaceX’s own float is scheduled to expand well before the index rebalances again. Roughly 20% of insider shares become saleable after the August 6 earnings report, with another 10% unlocking if the stock trades 30% above its $135 IPO price for five of any ten consecutive sessions. A staggered slice of the remainder frees up through December 2026. The same mechanism that squeezed the stock higher this week can, in principle, work in reverse once insiders are free to sell into whatever demand is left.

What this means if you hold a Nasdaq 100 fund from India 🇮🇳

This mechanism isn’t a distant US market curiosity. It runs directly through several products Indian retail investors already hold.

The Motilal Oswal Nasdaq 100 ETF alone carries roughly 11,241 crore rupees in assets under management, with a tracking error of just 0.06%, making it one of the primary routes Indian investors use to access the index. Alongside it sit fund of funds structures such as the Motilal Oswal Nasdaq 100 FoF, the ICICI Prudential Nasdaq 100 Index Fund, and offerings from Navi, Invesco, and Axis, all promising the same thing: rupee-based, one-tap exposure to the hundred largest non-financial companies on the Nasdaq. The pitch has worked. The Nasdaq-100 delivered close to 97% returns over the five years to mid-January 2026, and Indian money has followed suit, investing in these funds at scale.

Every one of these vehicles is a passenger on the exact mechanism this article describes. When SpaceX or any future mega IPO gets added, these funds buy it too, using Indian investor money, at the reconstitution price, with zero say from the fund manager on timing or valuation. Someone running a lump sum SIP into a Nasdaq 100 FoF this month has effectively become an indirect part owner of a company that went public less than a month earlier, trading at roughly 54 times its forecast 2026 sales, without ever choosing to make that specific bet. That isn’t a criticism of the fund. It’s simply what tracking an index means, and it’s worth knowing exactly what you signed up for.

Investors who would rather choose their own exposure, rather than accept whatever the index rulebook adds next, can hold individual US stocks and ETFs directly through platforms like Winvesta under the Liberalised Remittance Scheme, rather than relying solely on Indian FoF wrappers. Neither approach is inherently better. One hands the decision to a rulebook, the other keeps it with you, and it helps to know which one you’re actually using.

What to watch in the months ahead 🔭

The SpaceX inclusion event is over, but the mechanism continues to generate catalysts.

August 6, 2026, doubles as SpaceX’s first earnings report and its first insider lockup expiration, releasing roughly a fifth of insider shares, with a further tranche becoming eligible if the stock has held well above its IPO price. Watch whether float actually expands, or whether insiders choose to sit tight.

September and December 2026 bring Russell index reconstitution windows, during which SpaceX is expected to join the Russell 1000 given FTSE Russell’s relaxed float threshold, triggering a second, separate wave of mechanical buying across a different set of funds. December also brings the Nasdaq-100’s annual reconstitution, when weights get recalculated against updated float, likely pushing SpaceX’s index weight higher as more shares become tradable.

Mid-2027 is the earliest point SpaceX could qualify for the S&P 500, contingent on posting four consecutive quarters of GAAP profitability. That single event would dwarf everything that’s happened so far, given the more than 11 trillion dollars benchmarked to that index.

Beyond SpaceX specifically, the rule itself is now permanent. Any future mega IPO that clears the top-40 market-cap threshold on Nasdaq can expect the same mechanical demand within weeks, rather than the year it once took. The next large private company to list, in AI, defence, or anywhere else, inherits this exact playbook the moment it prices its shares.

If this changed how you see the mechanics behind your index fund, pass it on.

The bottom line 🏁

Index funds are not passive in the way the marketing implies. They execute a rulebook that forces predictable, price-insensitive trades on predictable days, and that rulebook is written by index providers, who make judgment calls about float, profitability, and timing that most fund holders never see.

For a diversified long-term investor, this mostly evens out over time and is not a reason to abandon index investing, which remains the cheapest and most reliable way to hold broad market exposure. It is a reason to stop reading a post-inclusion rally as validation of the underlying business, and to recognise that a chunk of every Nasdaq 100 or broad-market fund you hold, Indian wrapper or otherwise, is being continuously reshaped by rules you never voted on. The next time a mega IPO announces it’s joining an index, read it for what it actually is: a scheduled, mechanical trade, not a verdict on the company.

By the numbers 📊

27 billion dollars: estimated forced buying across Nasdaq-100 and Russell index funds triggered by SpaceX’s July 7 inclusion, against a public float of just 3 to 5%, per J.P. Morgan estimates cited across market reporting

15 trading days: how quickly SpaceX qualified for the Nasdaq-100 under the fast entry rule Nasdaq introduced on May 1, 2026, versus the roughly one year IPOs previously had to wait

1.4 trillion dollars plus: total assets tracking the Nasdaq-100 across ETFs, mutual funds, and derivatives

Roughly 60%: passive funds’ estimated share of US equity fund assets, per industry estimates, a share that has grown steadily since 2010

74 billion dollars: the one-day forced buying event when Tesla joined the S&P 500 in December 2020, per Jefferies estimates at the time

6.7% versus roughly 27%: Tesla’s share price gain three years after joining the S&P 500, against the index’s own gain over the same stretch, per Bloomberg data

11,241 crore rupees: assets under management in the Motilal Oswal Nasdaq 100 ETF, one of the main routes Indian investors use into this exact mechanism

Mid-2027: earliest point SpaceX could qualify for S&P 500 inclusion, contingent on four straight quarters of GAAP profitability

Disclaimer: All content provided by Winvesta India Technologies Ltd. is for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember, your capital is at risk. Terms & Conditions apply.