Google (GOOGL): The AI infrastructure play hiding inside the world’s biggest search engine

Picking a tech stock meant choosing between the search giant, the social network, and a handful of e-commerce plays and calling it diversification. Not anymore. Google’s evolution from advertising monopoly into a full-stack AI infrastructure company—complete with quantum breakthroughs, a cloud business finally generating real profit, and a subscription engine most analysts still underweight—has made this one of the most layered risk/reward setups in global technology.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors still think of Google as a search engine that happens to own YouTube. That framing is accurate and dangerously incomplete. Today’s Alphabet is simultaneously the world’s dominant intent-driven advertising marketplace, a fast-growing cloud infrastructure provider competing seriously for enterprise AI workloads, and a quantum computing pioneer whose own researchers are flagging long-term cryptographic risks that could reshape enterprise cloud security over the coming decade. It processes over 8.5 billion searches daily, commands over a billion hours of daily YouTube watch time, and runs one of the three largest hyperscale cloud platforms globally.

Alphabet recorded revenue north of $400 billion for FY 2025, per its official earnings release—Google Cloud has turned sustainably profitable, Workspace is compounding quietly in the background, and an AI summary layer now appears across a meaningful and growing share of US search results. The transformation isn’t cosmetic. Whether investors are positioned to benefit from it depends on what happens in courtrooms, competitive markets, and quantum laboratories simultaneously.

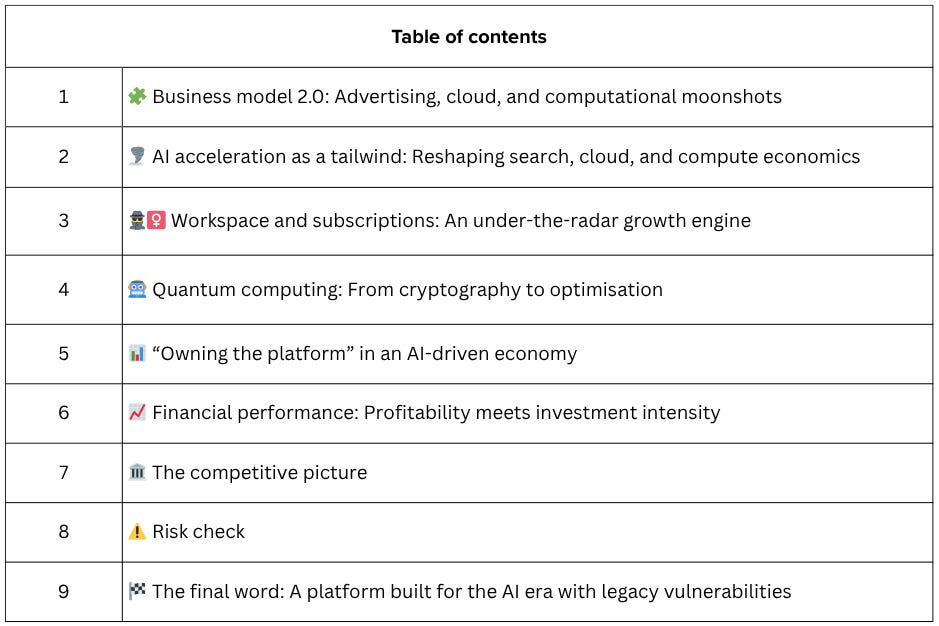

🧩 Business model 2.0: Advertising, Cloud, and computational moonshots

Google’s revenues now flow from three distinct engines rather than just search advertising, though that legacy business still generates the overwhelming majority of cash flow.

Google Services (advertising + subscriptions)

This segment includes Search, YouTube ads, the Google Network, and subscription offerings such as YouTube Premium and Google One. In 2025, Google Services generated revenues estimated to represent roughly three-quarters of Alphabet’s total, with Search advertising as the dominant contributor, per Alphabet’s filings. Growth rates in core advertising have moderated to mid-single digits as the business matures, while YouTube continues to deliver double-digit expansion in ad revenue. These directional splits are derived from Alphabet’s public reporting, though precise segment-level line items should be treated as approximate given consolidated reporting structures.

Google Cloud Platform

Google Cloud has transformed from a distant third into a genuine competitor to AWS and Azure. Cloud revenues grew strongly in 2025, well ahead of the prior year, per Alphabet’s FY 2025 filings. Critically, Google Cloud has now achieved sustained operating profitability—a meaningful structural shift from years of losses as Google invested aggressively in infrastructure. The platform includes infrastructure-as-a-service, data analytics via BigQuery, and increasingly AI model deployment through Vertex AI.

Other Bets and hardware

Waymo, Verily, Google Pixel devices, and Fitbit wearables sit here. Waymo has completed millions of paid autonomous rides, representing a meaningful commercial milestone. Hardware revenue from Pixel phones, Nest devices, and wearables contributes to the Services segment. While small relative to total revenue, these initiatives represent Google’s positioning for post-mobile computing paradigms.

In other words, ‘Google’ is now a diversified technology conglomerate with advertising subsidising aggressive investments in cloud infrastructure and speculative computing platforms—not just a search monopoly.

🌪️ AI acceleration as a tailwind: Reshaping search, Cloud, and compute economics

The generative AI wave continues reshaping Google’s core businesses, creating both defensive imperatives and offensive opportunities.

Search transformation and AI Overviews

Google has been integrating AI-generated summaries—called AI Overviews—into Search results across an expanding share of US queries. External tracking from analytics providers such as Semrush suggests AI Overview coverage currently appears on roughly 15–30% of US queries, depending on query category—a significant rollout, though not yet universal. Where AI Overviews do appear, independent analytics studies suggest queries increase by roughly 10% or more, as users ask follow-up questions and refine searches. Google appears to maintain similar ad density in AI Overview experiences to that in traditional search, though publicly quantified ad-load parity data has not been formally released by the company. The technology relies on Gemini models to process queries with multimodal understanding, a capability competitors struggle to match at scale.

Cloud AI services boom

Google Cloud’s AI and machine learning products are growing at a strong clip, with industry estimates suggesting revenue in this category is expanding rapidly—though a precise, publicly broken-out figure should be treated as an editorial estimate rather than a reported segment. Vertex AI, the platform for deploying custom models, serves a growing enterprise customer base with notable deployments, including Deutsche Bank migrating risk models and Walmart deploying inventory optimisation algorithms via the platform. Google’s TPU chips offer better price-performance than GPU alternatives for specific AI workloads, meaningfully creating differentiation against AWS and Azure.

Infrastructure advantage and flywheel

Google operates over 40 data centre regions globally, with dedicated subsea cable infrastructure providing substantial capacity across key ocean routes. This physical footprint enables training of frontier AI models like Gemini while offering cloud customers competitive inference latency in major markets. The flywheel works: internal AI development improves cloud products, cloud revenue funds infrastructure expansion, and better infrastructure attracts more AI workloads.

For a firm that monetises both consumer attention and enterprise compute, AI acceleration usually means expanded addressable markets rather than simple substitution.

🕵️♀️ Workspace and subscriptions: An under-the-radar growth engine

One of Google’s fastest-growing franchises sits far away from the advertising spotlight: collaboration software and consumer subscriptions.

Google Workspace momentum

Google Workspace—Gmail, Docs, Sheets, Drive, Meet—serves a large and growing enterprise customer base. Analyst estimates suggest Workspace is approaching roughly 10 million paying enterprise customers and generating meaningful annual recurring revenue. However, precise ARR, growth rate, and ARPU figures are not broken out in Alphabet’s public filings and should be treated as directional industry models rather than reported facts. Workspace includes advanced AI features like automated meeting summaries in Meet and writing assistance in Docs, powered by Gemini—capabilities Google has been upselling to premium enterprise tiers.

Expanding consumer subscriptions

Google One, YouTube Premium, YouTube TV, and Nest Aware collectively generated meaningful subscription revenue during 2025. YouTube Premium has crossed the 100 million subscriber milestone globally, as confirmed by Google in prior disclosures, with growth continuing through 2025—though precise year-over-year growth rates and specific regional breakdowns beyond formal disclosures should be treated as directional estimates. YouTube TV, the live television streaming service, has attracted a mid-single-digit million-subscriber base per third-party estimates at its published pricing—approaching cable-replacement relevance in the US market.

Higher-margin recurring revenue

This segment exhibits fundamentally different economics from advertising. Gross margins on subscriptions are estimated to be substantially higher than on advertising-dependent revenue, with low incremental cost per user once infrastructure is deployed. Enterprise churn rates for Workspace are widely considered sticky—consistent with the predictable revenue profile Wall Street assigns premium multiples to—though exact churn figures are not formally disclosed. Management has highlighted subscriptions as a strategic priority, citing their relatively defensive revenue profile compared to cyclical advertising.

This segment is high-margin, recurring, and structurally growing—very different economics from the auction-based advertising that still defines Google’s financial identity.

Want to add Alphabet to your portfolio? Trade GOOGL directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors—become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

🤖 Quantum computing: From cryptography to optimisation

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.