EWY and the KOSPI at 8,000+: AI supercycle or the most crowded trade on earth?

Before we begin. Buying “Korea exposure” used to mean betting on Samsung phones and Hyundai cars. Not anymore. The KOSPI has surged over 90% year-to-date in 2026, and the fund that tracks it — EWY — has returned over 107% year-to-date through late May 2026, because South Korea is now the memory chip backbone of the global AI infrastructure build. But as the index knocks on the door of 9,000 today, margin loans just hit a publicly reported record of approximately $21.8 billion per the Kobeissi Letter, foreign investors have been net sellers for weeks, and the last time this market tried to hold above 8,000, it crashed 12% in a single session (March 4, 2026 — the KOSPI’s worst single day in its 46-year history, per Reuters and CNBC), before rebounding nearly 10% the following day.

That’s why we built Winvesta Crisps — to help you figure out when a supercycle is real and when you’re walking into somebody else’s exit. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

The KOSPI hit an all-time high of 8,788 yesterday. Today, it’s up another 2% in pre-market, targeting 9,000. Jensen Huang is flying to Seoul this week. Samsung just unveiled HBM4. SK Hynix has roughly doubled or more in 2026. Nvidia’s new PC chip wiped out Intel overnight.

Every signal says buy Korea. The AI trade is real. The memory supercycle is real. The corporate governance reform is real.

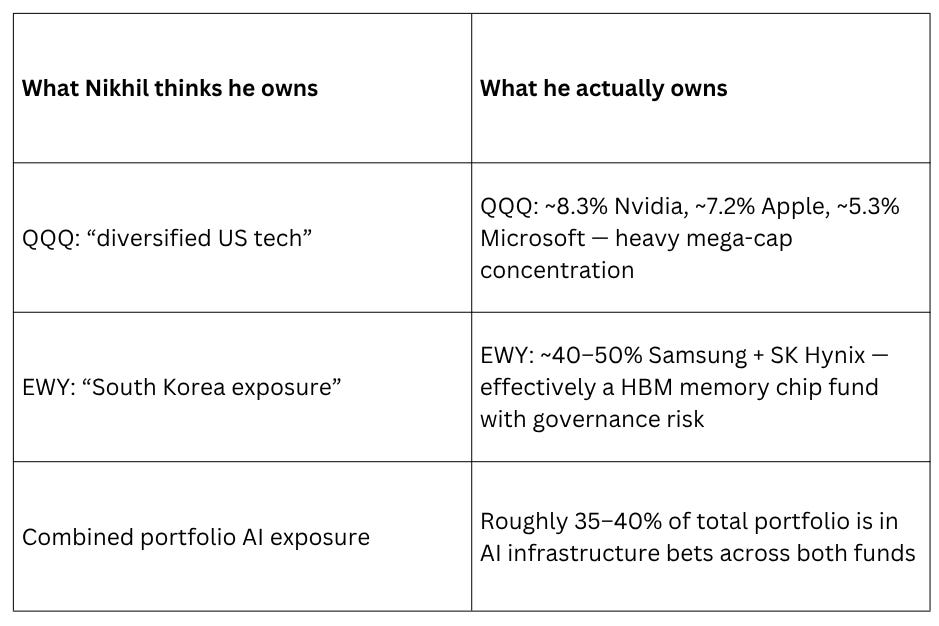

But here is what the data also says: Korean retail investors are now borrowing at a 20-year record to buy shares they cannot afford without their bank’s money. Foreigners have been net sellers for weeks, offloading billions of dollars while Korean retail absorbs every wave of supply. The top two holdings of EWY — Samsung and SK Hynix — now make up approximately 40–50% of the fund. Buying EWY at today’s prices is not diversifying into South Korea. It is making a concentrated, leveraged bet on whether the AI memory chip upcycle has another leg.

That dilemma — supercycle or crowded exit — is exactly what this week’s article is about.

🙋 Meet Nikhil

Nikhil, 41, a senior finance manager in Bengaluru. Portfolio: ₹55 lakhs across US markets. He bought QQQ two years ago as his “tech exposure.” He added a small position in EWY in January 2026 after reading about the Korea chip story. It’s up roughly 80% since then and is now his best-performing position — worth approximately ₹7.8 lakhs against an original ₹4.3 lakh entry.

Here is what Nikhil thinks he owns versus what he actually owns:

Nikhil’s dilemma right now: EWY is up 80% from his entry. The KOSPI is pushing toward 9,000. Jensen Huang is visiting Seoul this week. Every instinct says let the winner ride.

But his original thesis was “Korea as diversification.” That thesis has long since been replaced by something far more specific: a single-theme, high-conviction bet on whether AI memory chip demand keeps growing faster than the market expects. And a 12% single-day crash in March showed him what happens when that conviction gets tested.

Does he add here, hold, or use the rally to reduce?

🔍 What EWY actually is

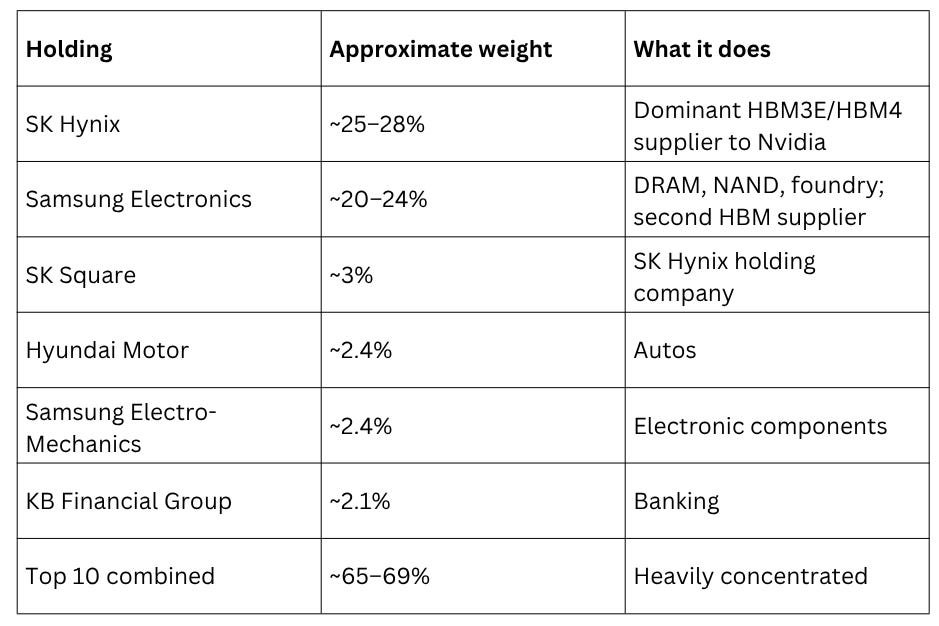

EWY is the iShares MSCI South Korea ETF, managed by BlackRock. Launched in 2000, it is the largest and most liquid vehicle for South Korea exposure available to non-Korean investors, with assets under management of $24.14 billion as of May 29, 2026 (per iShares). It tracks the MSCI Korea 25/50 Index, which applies concentration caps — no single issuer can exceed 25% of the index — specifically because without those caps, SK Hynix and Samsung would likely consume an estimated 60% or more of the fund based on their relative market capitalisation.

Top holdings as of late May 2026 (approximate, subject to quarterly rebalancing):

Sector breakdown:

Information Technology: ~50–52% (MSCI classification; some narrower classifications show ~36–38%)

Industrials: ~18%

Financials: ~10%

Consumer Discretionary: ~8%

The honest description of EWY: it is not a diversified Korea fund. It is a memory chip supercycle fund wrapped in a country ETF structure. The governance reform story (Corporate Value-up Program 2.0, enacted in mid-2025, requiring companies to cancel treasury shares and boost dividends) is real and adds a valuation re-rating tailwind. But at current prices, the dominant driver of EWY returns is HBM demand from Nvidia, AMD, and hyperscalers — full stop.

Here is the approximate direction of EWY and KOSPI flows over the past four weeks (ILLUSTRATIVE):

Note: Flow figures below are directional estimates and illustrative editorial models. They are not drawn from a single audited dataset. Cross-reference with Bloomberg, ETF.com, or TrackInsight before acting.

Past 4 weeks (EWY, US-listed): Net positive, meaningfully elevated inflows — retail and institutional buying on AI chip narrative (Source: ETF.com / Bloomberg, directional estimate)

Past 4 weeks (KOSPI, domestic): Strongly positive domestic flows; foreign net selling — Korean retail absorbing foreign distribution (Source: Korea Financial Investment Association; ZeroHedge / Goldman)

Past 2 weeks (foreign KOSPI flows): Persistent net selling, focused on tech — foreigners net sold 9+ consecutive sessions (Source: Goldman; ZeroHedge)

Past 1 week (Korean margin loans): Record high, ~$21.8B (~29 trillion won) — retail buying on borrowed money (Source: Korea Financial Investment Association; Kobeissi Letter, May 28)

The divergence that matters most: EWY inflows from international investors look positive in the US. Inside Korea, the picture is more unsettling — domestic retail has been absorbing a sustained wave of foreign selling with borrowed money. When the sellers are institutions and foreigners, and the buyers are leveraged retail, history has a pattern about how that resolves.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.