China went from "uninvestable" to everyone's favourite trade overnight

Before you buy in, check what you already own.

Avoiding China after the regulatory crackdown looked like the obvious call, the tech platform takedowns. The property sector collapsed. The zero-COVID shadow that outlasted every forecast. Not anymore. The US Supreme Court just stripped out a major chunk of Trump’s tariff toolkit. The US-China trade truce now runs through November 2026, with both sides having meaningfully reduced bilateral tariffs from last year’s extreme levels. And Chinese AI names like Alibaba’s Qwen have racked up 700 million downloads, competing directly with US models at a fraction of the cost. The “uninvestable” story is cracking. But before you open Winvesta and add MCHI, FXI, or KWEB, there is a calculation most Indian investors have never done.

That is why we built Winvesta Crisps: to decode what is actually moving the funds you own in plain language before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Markets are doing that thing where a structural story and a tactical setup arrive simultaneously, and suddenly everyone wants in. The US-China tariff war, which briefly saw bilateral reciprocal tariff rates spike past 100% in April 2025, has settled into something far more manageable. The US Supreme Court struck down IEEPA-based tariffs in February 2026, per Holland and Knight’s trade briefing. Trump replaced them with a 10% Section 122 tariff valid through July 24 2026. And crucially, the November 2025 US-China bilateral truce, which significantly reduced the specific April 2025 escalation tariffs on both sides, now extends through November 10 2026, per reporting from China Briefing and the Congressional Research Service. The “China reopening” narrative has upgraded itself into a “China rerating” thesis.

MCHI, FXI, and KWEB have all responded. The one-year total return on MCHI came in around 31% in USD over the 12 months to December 31 2025, per BlackRock iShares performance data. FXI trades at a low-teens forward P/E on many sell-side estimates, roughly half the S&P500's mid-20s multiple, with a trailing dividend yield in the mid-2% range. And KWEB, the most beaten-up of the three, holds some of the hottest AI names by monthly active users, including Alibaba, Baidu, and Tencent.

Here is what nobody is telling you: if you own VT, EEM, or any emerging markets fund, you already own China. You do not know how much. The question is not” Should I buy China?” It is “Do I know my real exposure before I add more?”

Let me introduce you to someone who might be you.

🎯 Meet Meera

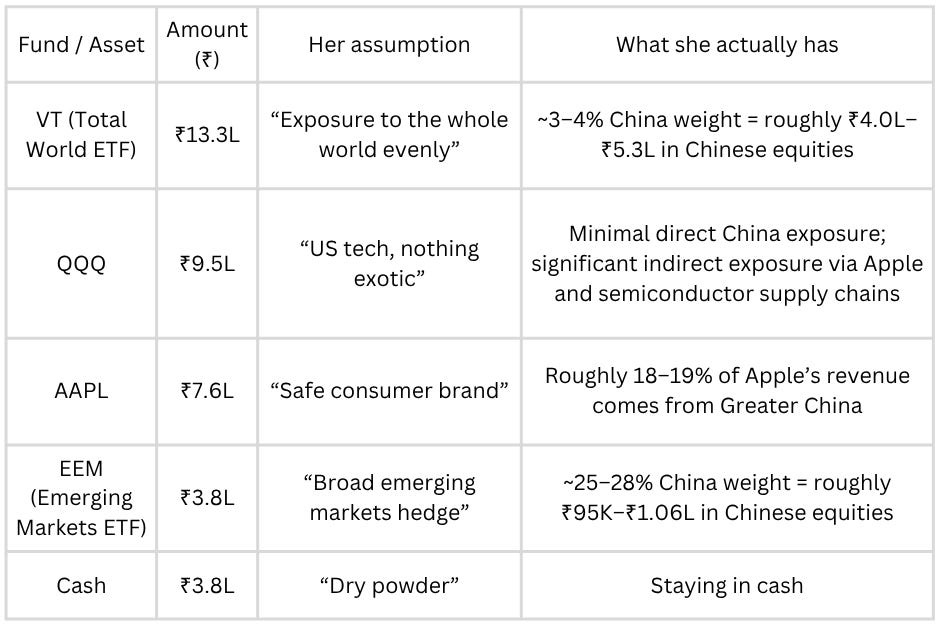

Meera, 33, product manager at a Bengaluru fintech. Portfolio: ₹38 lakhs across US markets through Winvesta. She built her allocation over three years following a sensible-sounding framework: VT for global diversification, QQQ for tech growth, Apple because “everyone uses iPhones,” and EEM because her finance-savvy colleague kept saying emerging markets are cheap.

Here is what Meera thinks she owns versus what she actually owns:

Note: ETF country weights are approximate and shift regularly. The above is illustrative of concentration risk, not a precise audit. Verify directly with the fund provider before making allocation decisions.

Meera's hidden reality: She has never bought MCHI, FXI, or KWEB directly. She believes she has zero deliberate exposure to China. But between VT and EEM alone, she already has roughly ₹1.35 to ₹1.59 lakhs in Chinese equity exposure, approximately 3.5 to 4.2% of her total portfolio. She does not know this.

Now she is reading headlines about the tariff truce and the KWEB AI story, and she is seriously considering adding ₹3 lakhs directly into MCHI. If she does that without accounting for her existing exposure, her real China allocation jumps to roughly ₹4.35 to ₹4.59 lakhs, or close to 11-12% of the portfolio.

That is not diversification. That is an undeclared, concentrated bet on a single geopolitical relationship.

What happened to Meera when tariff escalation peaked in April-May 2025:

When US-China tariffs hit extreme levels, EEM sold off sharply, VT dropped on its China weight, and Apple fell on supply chain fears and China revenue concerns. Her “safe, diversified” portfolio behaved like a single correlated trade, because the China risk was spread across every fund she owned. The tariff truce brought it all back. But she could not explain why her portfolio moved in either direction.

That inability to explain the move is the trap.

📊 What the three funds actually give you

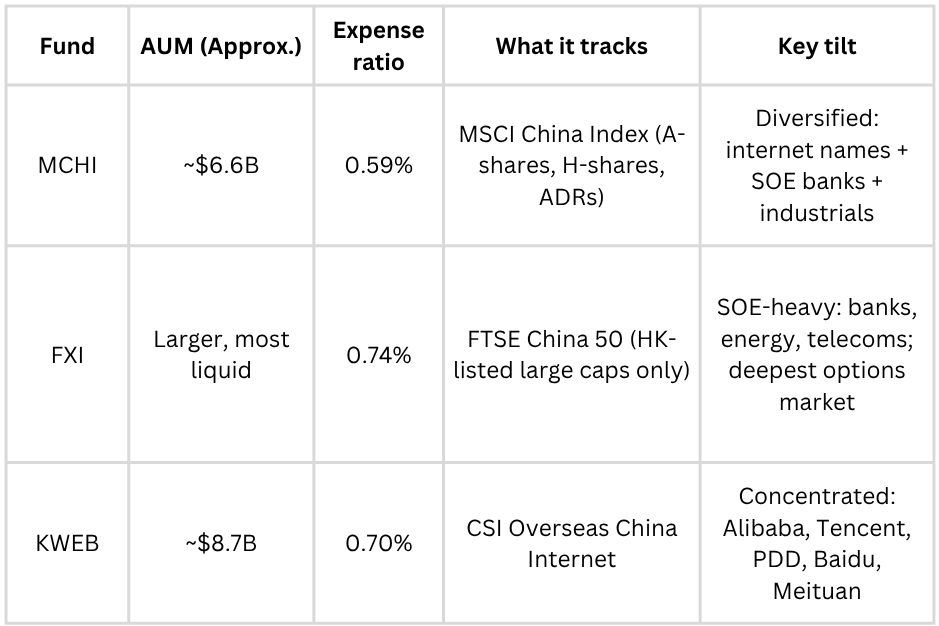

Before looking at flows, it is worth understanding what MCHI, FXI, and KWEB actually hold, because these are not interchangeable China plays.

KWEB is the most interesting story right now. Alibaba's Qwen model family surpassed 700 million downloads on Hugging Face as of January 2026, making it the world’s most widely used open-source AI system, according to data cited by the South China Morning Post. Baidu's ERNIE Bot and Tencent’s Hunyuan platform are among the top 10 global AI applications by monthly active users as of January 2026, per Statista data cited by KraneShares. KWEB companies collectively grew their AI and cloud-attributable revenue roughly 12% year-over-year in 2025, per KraneShares company data.

But KWEB is also the most scarred: it remains roughly 50% below its 2021 peak, even after the recent rally. It is the highest-beta, highest-conviction play of the three. If you are right, it rips. If you are wrong or early, it grinds.

FXI is the trader's vehicle: deep options activity, tight spreads, SOE-heavy, more stimulus-sensitive than AI-sensitive. On many sell-side estimates, it trades at a low-teens forward P/E versus the S&P500's mid-20s multiple, with a trailing dividend yield in the mid-2% range, providing a partial buffer while you wait. If you believe Beijing will continue to push fiscal support, FXI is the cleaner expression. If you believe in platform rerating and China AI, MCHI or KWEB is the call.

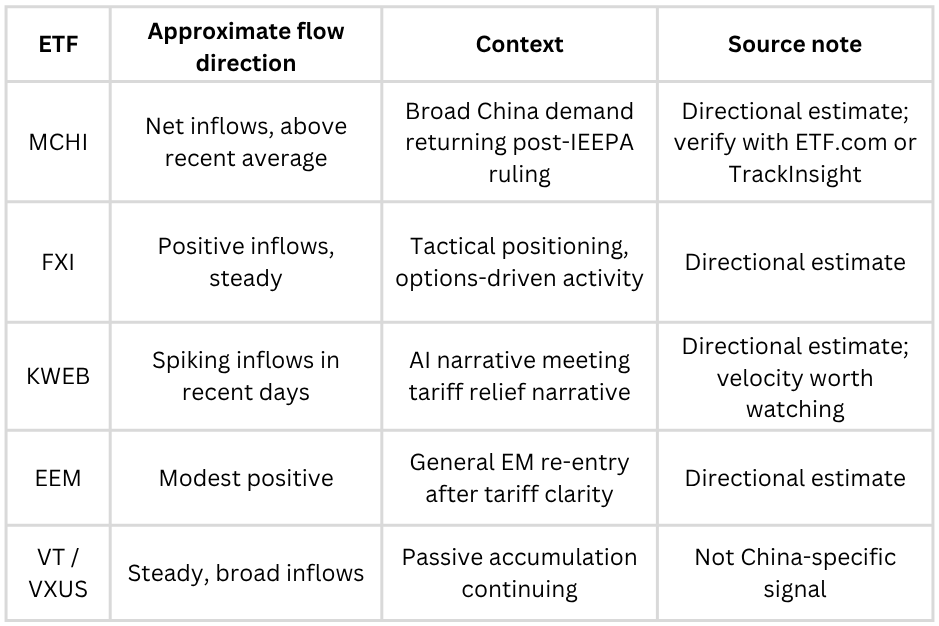

Approximate ETF flow direction (past 4 weeks through April 28, 2026 - ILLUSTRATIVE, not drawn from a single audited dataset):

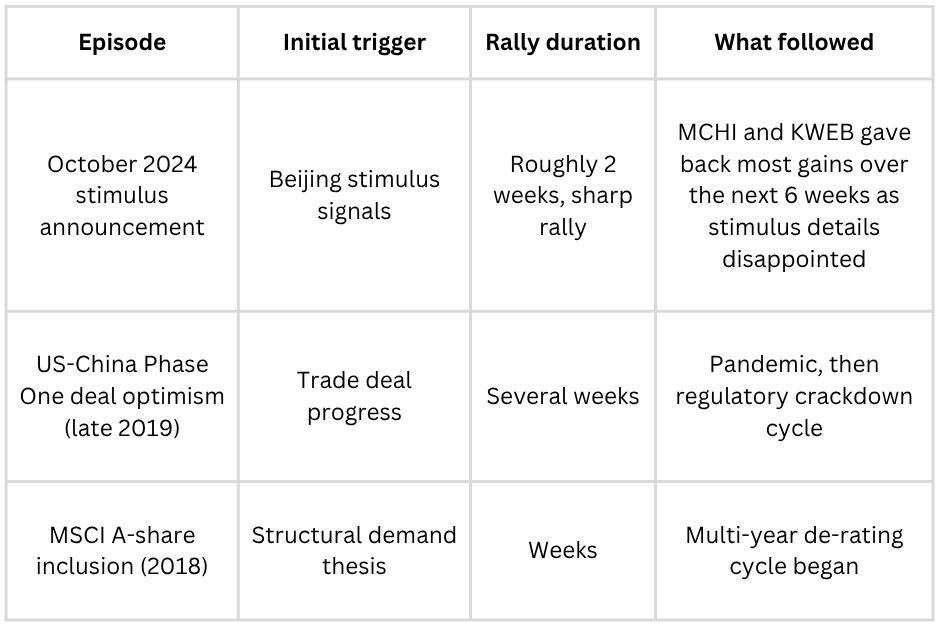

Here is the divergence worth watching: KWEB’s inflow velocity has accelerated sharply, driven by a combination of the AI narrative and tariff-truce headlines. That is exactly the pattern seen in October 2024, when Beijing announced stimulus measures and Asian ETFs surged. Retail money chased the story. Institutions trimmed into the move. KWEB gave back most of its gains over the following weeks as stimulus details disappointed and the carry-trade math reset. The structural thesis turned out to be real. The entry point turned out to matter anyway.

Institutions are returning to China. The question is whether you are arriving with them or after them.

🧠 The psychology trap

Right now, the China bull thesis is assembling itself out of genuinely real pieces:

✅ “The IEEPA tariffs are legally dead, and the bilateral truce holds through November 2026.”

✅ “China is trading at roughly half the US market’s P/E. That is a generational discount”.

✅ "Alibaba's Qwen has 700 million downloads. China IS the other AI story”.

✅ “The Section 122 tariffs are only 10%. The worst tariff escalation is clearly behind us”.

Every one of these is factually grounded. But here is the cognitive trap: these arguments have been partially true for the last two years, during which KWEB remained deeply below its 2021 peak,k and FXI underperformed. What changed is not the thesis. What changed was that the price action improved, making the thesis feel more convincing.

That is recency bias wearing a value-investing outfit.

Historical China ETF recovery pattern (illustrative, approximate):

The structural thesis was real every single time. The rally faded anyway. Not because the thesis was wrong, but because the market priced in more certainty than the situation actually contained.

The rational vs FOMO checklist:

Ask yourself honestly:

❌ Can you explain the difference between what Section 122 tariffs mean for China versus what IEEPA tariffs meant, and why the legal mechanism change matters for future trade policy risk?

❌ Do you know what the USTR’s Section 301 investigations launched in March 2026 could do to the trade relationship if they find violations? (Hearings are running through April and May 2026, per China Briefing.)

❌ Can you name three reasons KWEB has better risk/reward today versus six months ago, beyond "the price is up"?

❌ Would you be adding China exposure right now if you had not seen the tariff truce headline?

If you answered “no” to three or more, you are not making a thesis-based investment. You are momentum-chasing in the region with the world’s most consequential bilateral risk relationship.

🚀 Want to add MCHI, FXI, or KWEB to your portfolio? Trade China ETFs directly from India on the Winvesta app. No US bank account needed!

Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

💡 Three realistic scenarios for Meera's portfolio

Let’s model what actually happens to Meera’s ₹38 lakh portfolio, including her hidden China exposure, under different macro outcomes over the next 6 months. The following scenarios, probabilities, and return estimates are illustrative stress tests based on assumed returns and subjective probabilities, not forecasts, market consensus, or guarantees of future performance.

Scenario 1: “Truce holds, structural recovery” (30% probability)

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.