Broadcom (AVGO): The custom AI chip empire hiding inside a semiconductor conglomerate

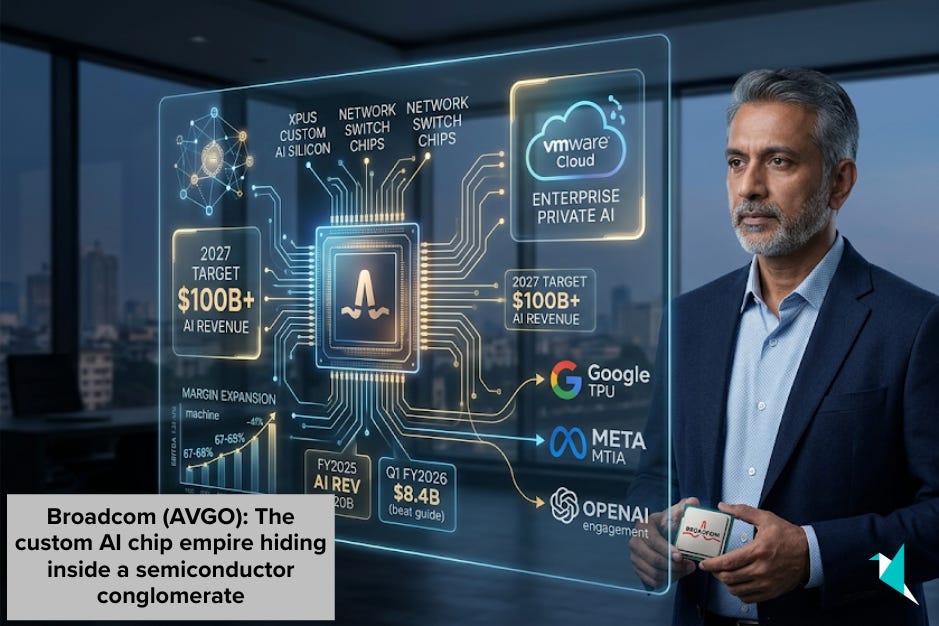

Following Broadcom meant tracking which enterprise software company Hock Tan would acquire next. CA Technologies, Symantec, VMware: three of the largest technology acquisitions ever executed, each converted into a margin-expansion machine. That playbook is complete. What has replaced it is something most investors haven’t fully processed: a capital-allocation genius who has pointed the whole machine at AI, locked in multi-decade chip-design contracts with Google, Meta, and OpenAI, and is now guiding toward $100 billion in AI chip revenue by 2027. The quietest trillion-dollar AI story in the market.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors think of Broadcom as a diversified chipmaker that fell into software when it bought VMware. That framing is accurate and dangerously incomplete. Today’s Broadcom is simultaneously the dominant architect of custom AI silicon for the world’s most powerful AI companies, the company that designs and supplies the Ethernet switching chips connecting virtually every large-scale AI cluster on the planet, and an enterprise software platform generating gross margins above 93% on a base of hundreds of billions in contracted recurring revenue. Hock Tan, the CEO, told analysts on the Q1 FY2026 call that he has “line of sight to achieve AI revenue from chips, just chips, significantly in excess of $100 billion in 2027.” He said it quietly and without drama, which is exactly how Broadcom operates.

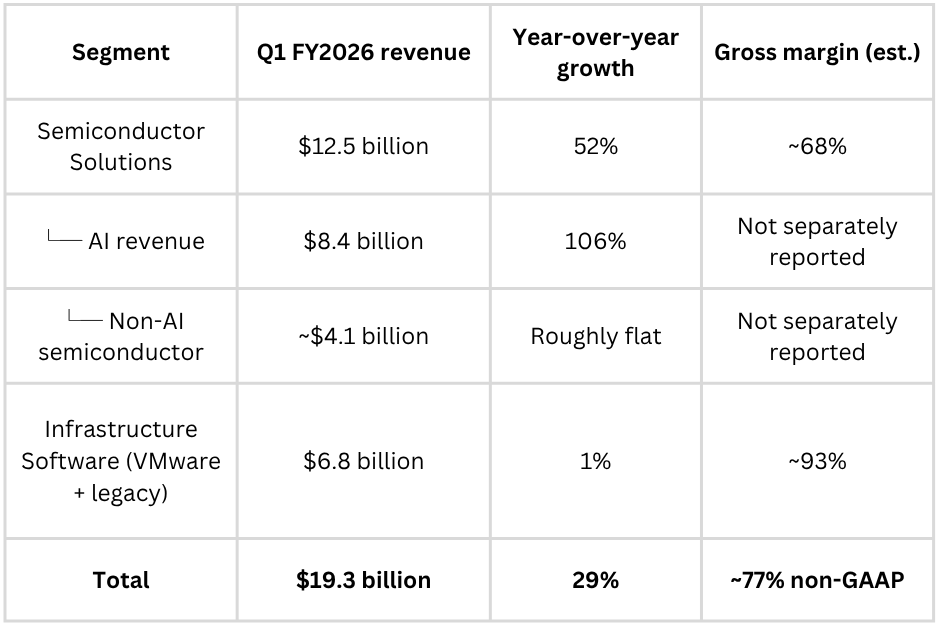

The company reported Q1 FY2026 revenue of $19.3 billion, up 29% year-over-year, per its March 2026 earnings release, with AI semiconductor revenue at $8.4 billion, up 106% year-over-year and ahead of its own forecast. It then guided Q2 FY2026 revenue to approximately $22 billion, a number that the market received very positively and validated a thesis most of the market has been slow to price: Broadcom is not riding the AI wave. It is the infrastructure beneath it.

🏭 What Broadcom actually is today

Broadcom operates two engines: semiconductors and infrastructure software. Within semiconductors, the story has bifurcated sharply between the legacy businesses, wireless chips for Apple iPhones, broadband chips for telcos, storage controllers, and a fast-accelerating AI portfolio that now drives the majority of segment growth.

The semiconductor business is best understood as having three layers. First, custom AI accelerators called XPUs: chips co-designed directly with hyperscalers over 18 to 24-month engineering cycles, optimised for their specific AI workloads rather than general-purpose use. Broadcom designs Google’s TPU (Tensor Processing Unit), Meta’s MTIA (Meta Training and Inference Accelerator), and has now confirmed a multi-year custom chip engagement with OpenAI. Second, AI networking silicon: the Tomahawk and Jericho families of Ethernet switch and router chips that stitch together the massive GPU and XPU clusters inside AI data centres. Third, everything else: wireless chips, storage controllers, fibre-optic components — a collection of category-leading products that generate healthy but slower-growing revenues.

The software business is VMware, now repackaged as VMware Cloud Foundation (VCF). This private cloud operating stack allows large enterprises to run virtualised and AI workloads on their own infrastructure rather than in public clouds. Broadcom acquired VMware in November 2023 for approximately $69 billion, converted the customer base from perpetual licences to subscription contracts, stripped the product portfolio down to VCF as the core offering, and has been executing a margin-expansion playbook since. The results have been striking: software gross margins reached 93% in Q4 FY2025, per Broadcom’s earnings release, and operating margins in the segment improved to 78% by the same period.

The combination is unusual in technology: a capital-light, high-switching-cost software engine generating the cash flows to fund the engineering investment behind the world’s most sophisticated custom chip designs.

🧩 Segment breakdown

Broadcom reports two segments: Semiconductor Solutions and Infrastructure Software.

Source: Broadcom Q1 FY2026 earnings release, March 2026. Gross margin figures are non-GAAP. AI versus non-AI semiconductor split based on management commentary; segment-level margin breakdown is not separately reported in Broadcom’s public filings.

Within semiconductors, the AI component is now the overwhelming growth driver. Non-AI semiconductor revenue — wireless, broadband, industrial, and storage — is running roughly flat as the smartphone and networking refresh cycles work through their troughs. The non-AI business is still profitable and cash-generative, but it is no longer the thesis.

Within infrastructure software, the 1% growth in Q1 FY2026 reflects a deliberate quarter: VMware renewal cycles are seasonal, and management has guided low-double-digit growth for the segment over the full FY2026 year, per the Q4 FY2025 earnings call. The software business is not accelerating dramatically, but it is producing extremely high margins on a very large, sticky, recurring-revenue base, with bookings exceeding $10.4 billion in Q4 FY2025, up from $8.2 billion a year earlier, providing strong forward revenue visibility.

Want to add Broadcom to your portfolio? Trade AVGO directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

🤖 XPUs, networking, and the $100 billion AI chip target

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.