Apple (AAPL): The services transformation hiding inside the iPhone story

Many people think Apple is a hardware company that sells premium phones. It’s not. It’s a platform operator collecting recurring fees on subscriptions, transactions, advertising, and financial services — layered on top of 2.35 billion active devices worldwide. The company generated approximately $100 billion in free cash flow in fiscal 2024, even as many still compared it to Samsung. Here’s why that framing is outdated, how the services transformation actually works, and what it means for your portfolio.

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam

🧩 Business model 3.0: Devices as distribution, services as margin

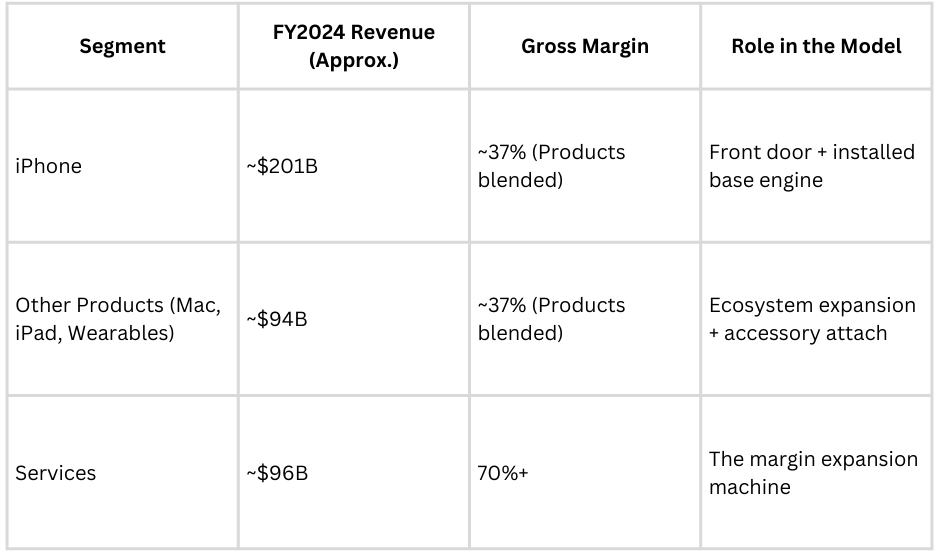

Apple’s revenues now come from two fundamentally different engines rather than just iPhone sales. In fiscal 2024, the company generated $391 billion in total revenue. Products accounted for roughly $295 billion, whilst Services delivered about $96 billion — a record high. But the composition matters more than the headline split.

Products: Still the largest bucket, but maturing

The Products segment includes iPhone, Mac, iPad, Wearables (Apple Watch, AirPods), and accessories. iPhone alone contributed approximately $201 billion in fiscal 2024, representing just over 51% of total revenue — down from 65% a decade ago. Unit growth has stalled in mature markets. The current story is average selling price expansion (driven by Pro models) and installed base growth. Apple’s active installed base reached approximately 2.35 billion devices globally by early 2025, up about 150 million year over year. Each device is a potential subscriber to services.

Services: The margin expansion machine

Services grew around 13% year-on-year in fiscal 2024 and carry gross margins exceeding 70%, compared to Products’ about 37%. This segment includes the App Store (and its 15-30% take rate), Apple Music, iCloud storage subscriptions, Apple TV+, Apple Pay transaction fees, AppleCare, licensing fees from Google (estimated at $20 billion annually for default search placement), and a rapidly growing advertising business. Paid subscriptions across all services surpassed 1 billion in 2024, more than doubling since 2020. The App Store remains the crown jewel, generating an estimated $85 billion in gross billings annually, of which Apple keeps roughly $25-30 billion after developer payouts.

Emerging ecosystem revenue

Apple doesn’t break out all components, but within Services lies a nascent fintech and advertising operation. Analysts estimate Apple Pay processes around $6 trillion in payment volume annually. Analysts estimate Apple’s advertising business — primarily App Store search ads and nascent display inventory — generates $5-7 billion in revenue, growing 20-25% annually. The company launched a high-yield savings account with Goldman Sachs, attracting $10 billion in deposits within months, and continues expanding Apple Card penetration.

In other words, ‘Apple’ is now a subscription and transaction platform monetising 2.35 billion devices, not just a hardware manufacturer refreshing handsets annually.

Someone shared this with you? Get your own insider updates directly — no intermediary needed.

🕵️♀️ Advertising: The quiet monster

Apple’s ad business deserves its own spotlight because it’s the most underappreciated part of the thesis — much like Amazon’s advertising was five years ago.

Search Ads’ momentum.

Apple’s App Store Search Ads allow developers to bid for placement when users search for apps. The product launched in 2016 but accelerated sharply after 2021, when Apple introduced App Tracking Transparency (ATT), which requires apps to ask for permission before tracking users across other apps and websites. ATT devastated Meta and Snap’s advertising targeting capabilities, but Apple’s own ad products — which rely on first-party App Store data — were unaffected. Analysts estimate Search Ads revenue at $5–7 billion annually, growing 20-25% year-on-year, with remarkably high conversion rates because the inventory sits at the point of intent.

Expanding inventory: Apple News, Stocks, Maps

Apple quietly expanded ad placements into Apple News and Stocks in 2022, then into Maps in 2023 (search ads for local businesses). The company is reportedly developing display advertising capabilities within Apple TV+ and exploring in-app ad networks that would compete directly with Google’s AdMob. The addressable inventory is enormous: 2.35 billion active devices, rich first-party behavioural data, and premium user demographics.

“Privacy-first advertising” as a moat

Apple frames its advertising as privacy-preserving because it doesn’t track users across third-party properties and relies on on-device processing. This positioning allows Apple to sidestep the regulatory and reputational issues plaguing Meta and Google, whilst still building a high-margin advertising business. If Apple’s ad revenue reaches an estimated $15-20 billion over the next three to five years — entirely plausible given installed base growth and inventory expansion — it would represent a meaningful contribution to total Services revenue.

This segment is early-stage, high-margin, and structurally advantaged by Apple’s privacy policies—very different economics from the hardware-centric origins.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.