Amazon’s hidden engine: The advertising giant hiding inside the world’s biggest store

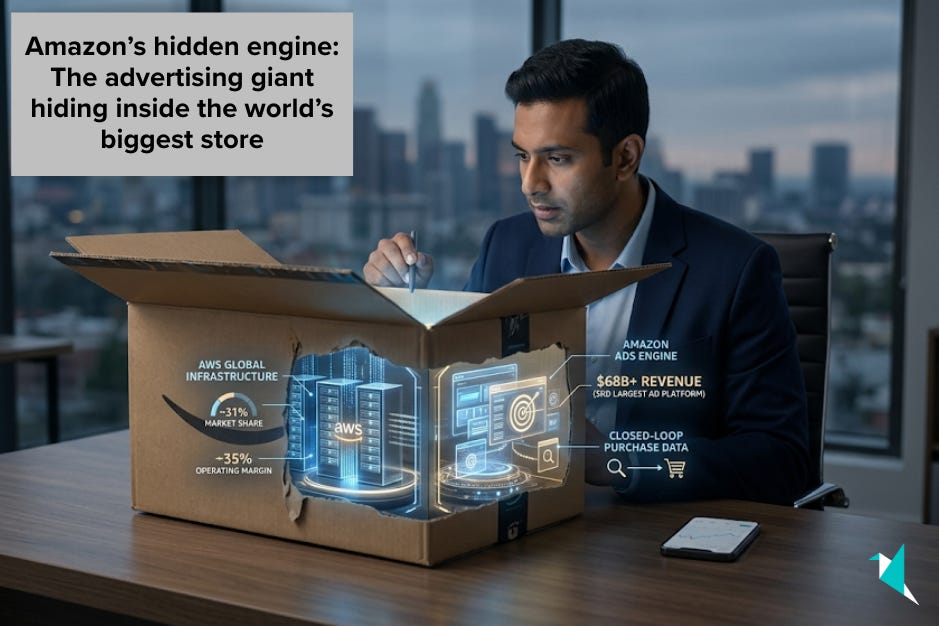

Thinking of Amazon as the world’s biggest online store may have worked. Not anymore. Amazon’s retail business runs on single-digit margins and is now under genuine tariff pressure in 2026. The parts of the business quietly compounding are a cloud platform with roughly 31% global market share and operating margins in the mid-30% range, and an advertising engine that generated more than $68 billion in revenue last year, making it the world’s third-largest digital ad platform behind only Google and Meta.

That’s why we built Winvesta Crisps, to decode what’s actually driving the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in spam.

Most investors hear “Amazon” and picture a cardboard box at the door. That is fair. Amazon runs the world’s most visited online marketplace, ships a massive portion of all US e-commerce packages, and employs more people than most countries’ military forces. The problem is that the cardboard-box framing completely misses where the money is made. Amazon’s retail business, the thing most people think the company is, runs on thin single-digit margins and has been squeezed further by tariffs in 2026, per recent management commentary and public reporting.

The parts of Amazon that are genuinely compounding are its cloud infrastructure business, which holds roughly 31% of the global cloud market per industry estimates, and an advertising business that generated more than $68 billion in full-year 2025 revenue and has quietly become the world’s third-largest digital ad platform, behind only Google and Meta, per company filings and industry data. This is not a transformation story. It is a revelation about what Amazon has always been building, not about how most investors have described it.

📦 Not one company, but four

The way Amazon reports its results hides the real story. Most coverage leads with total revenue, which crossed approximately $717 billion for full-year 2025, per public reporting. That number tells you almost nothing useful on its own. The business is four distinct operations running under one roof, each with dramatically different economics.

North America retail is the familiar story: online stores, third-party marketplace fees, Prime memberships, and fulfilment logistics across the US, Canada, and Mexico. It generates enormous revenue but operates on margins far thinner than the other segments. Tariff pressure in 2026 has made life harder for the millions of third-party sellers who populate the marketplace. Jassy has acknowledged in recent public appearances that tariffs are creating price pressure for marketplace sellers and are showing up in consumer prices, and that the inventory buffer many sellers had pre-built largely ran out by late 2025, per recent reporting.

International retail covers everything outside North America. It ran at a loss for years as Amazon invested in infrastructure across the UK, Germany, Japan, India, and newer markets. It has only recently begun turning profitable at the segment level, per public reporting. The India business, in particular, is a multi-decade bet: Amazon committed to investing $35 billion in India by 2030, per company announcements from December 2025, covering everything from logistics and fulfilment to AWS data centre infrastructure. That is not e-commerce spend. That is an infrastructure ownership thesis.

AWS is where the economics get genuinely interesting. The cloud segment posted $35.6 billion in revenue in Q4 2025 alone, growing 24% year-over-year and at its fastest rate in 13 quarters, per company disclosures. Operating margin at AWS runs around 35%, meaning the cloud business generated approximately $12.5 billion in operating income in a single quarter. AWS holds roughly 31% of the global cloud market share, according to industry estimates, ahead of Microsoft Azure in the mid-20s and Google Cloud at around 11%.

The advertising business is the one most investors still overlook. Amazon’s ad services generated more than $68 billion in full-year 2025 revenue, growing at around 22% year-over-year, per company filings and industry estimates. That makes it the third-largest digital advertising platform on the planet. The ad business does not have the household name recognition of Google or Meta, but it has something neither of them has: closed-loop purchase data. When a brand advertises on Amazon, it can measure exactly how many units are sold as a direct result. That measurement capability is pulling TV budgets, branded search spend, and retail media dollars into Amazon at an accelerating pace.

🚀 The dual engines: AWS and advertising

The two Amazon businesses compounding fastest are the two with the least obvious connection to cardboard boxes.

AWS: Custom silicon and the AI infrastructure bet

Amazon is making an enormous bet that AI compute demand will remain insatiable for the better part of this decade. The 2026 capital expenditure plan stands at approximately $200 billion, predominantly for AWS infrastructure, per management's guidance on the Q4 2025 earnings call. That is roughly double what the company spent in 2025 and one of the largest corporate infrastructure commitments in US history.

What makes the bet coherent is the backlog sitting behind it. AWS’s contracted revenue backlog approached the mid-$200 billion range at the end of Q4 2025, growing substantially faster than reported revenue, per company disclosures and subsequent analysis. These are signed enterprise commitments, not pipeline projections. Per CEO Andy Jassy’s remarks, AWS added more absolute revenue in 2025 than either Microsoft Azure or Google Cloud.

The AI angle runs deeper than just selling cloud capacity. Amazon has built its own silicon: Trainium chips for AI training and Inferentia chips for inference, which together are approaching a roughly $20 billion annual revenue run rate and growing at triple-digit year-over-year rates, per Jassy’s commentary. Bedrock, Amazon’s managed AI service that lets enterprises deploy large language models on proprietary data within AWS infrastructure, crossed a multi-billion-dollar annualised run rate, with customer spend growing by around 60% quarter-over-quarter, per company disclosures.

The custom chip strategy matters because it gives Amazon pricing leverage over Nvidia-dependent workloads. Trainium3, with claimed 40% better price-performance than the prior generation, per the company, makes it structurally cheaper to run AI workloads on AWS than on competing clouds that rely entirely on Nvidia GPUs. Amazon has also committed approximately $25 billion to Anthropic across multiple investment tranches, per public reporting, giving AWS a deep integration with one of the leading AI labs and a reason to exist in every enterprise AI conversation.

Amazon Ads: The closed-loop advantage

Amazon’s advertising business has an architecture that Google and Meta genuinely cannot replicate. When someone searches for a product on Amazon, buys it, and the brand then retargets that buyer across Fire TV, Prime Video, and sponsored display placements, Amazon has complete purchase-to-conversion data across the entire journey. Google has search intent. Meta has audience targeting. Amazon has the purchase receipt. That closed-loop visibility is what is pulling retail media budgets toward Amazon at a pace that is still early relative to the total addressable market.

Prime Video is the newest and fastest-growing inventory layer. Amazon launched advertising across all Prime Video programming in 2024 and reported an average monthly ad-supported audience of 315 million viewers globally, up from 200 million disclosed in April 2024, per Deadline. This audience spans 16 countries, including India, and gives Amazona premium video inventory that competes directly with traditional broadcast television budgets. Q4 2025 advertising revenue came in at $21.3 billion, up about 22% year-over-year, per company filings.

The advertising business also carries structurally higher margins than the North American retail sector. Amazon does not break out ad profitability directly. Still, analysts broadly characterise it as the company's highest-margin operations, per consensus commentary. CFO Brian Olsavsky noted on the earnings call that advertising contributed more than $12 billion of incremental revenue in 2025 versus 2024. As the ad business scales, it pulls up Amazon’s consolidated margin profile even as the $200 billion capex cycle creates near-term earnings pressure.

Want to add Amazon to your portfolio? Trade AMZN directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors, become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

💰 Financial performance

The figures below reflect Q4 2025 reported results and full-year 2025 actuals, per company filings. Q1 2026 figures are based on management guidance and analyst consensus, not reported results.

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.