Amazon (AMZN): The cloud infrastructure company hiding inside an online shop

Most investors still look at Amazon as an e-commerce stock. They see Prime Day headlines and delivery vans and think they understand the business. Meanwhile, AWS is quietly generating 58% of operating income, advertising is growing faster than Google’s, and the real valuation story is hiding in cloud infrastructure margins — not retail revenue. That’s why we built Winvesta Crisps — to decode what actually drives the companies you own, in plain language, before the consensus catches up. 60,000+ investors from all over India are already in. What about you?

🔔 Don’t miss out!

Add winvestacrisps@substack.com to your email list so our updates never land in your spam folder.

Everyone thinks Amazon is an e-commerce company that happens to run servers. It’s not. It’s the dominant cloud infrastructure company that subsidises a retail and media empire—backed by custom AI silicon, a digital advertising business rivalling Google’s, and a logistics network no competitor can replicate. AWS generated $107.6 billion in revenue in 2024, accounting for roughly 58% of Amazon’s total operating income despite representing only about 17% of revenue. The retail operation—$638 billion in total sales—exists primarily to feed the flywheel: acquire customers, convert them to Prime, monetise them through ads, and funnel enterprise relationships into AWS contracts. That combination makes Amazon the most structurally embedded company in the global economy. Here’s why the real story isn’t the online shop—it’s the plumbing underneath.

The cloud giant’s business model, explained 🧩

Amazon doesn’t make most of its money from a single business anymore. It makes money across four distinct engines—each with different growth trajectories, margin profiles, and competitive dynamics.

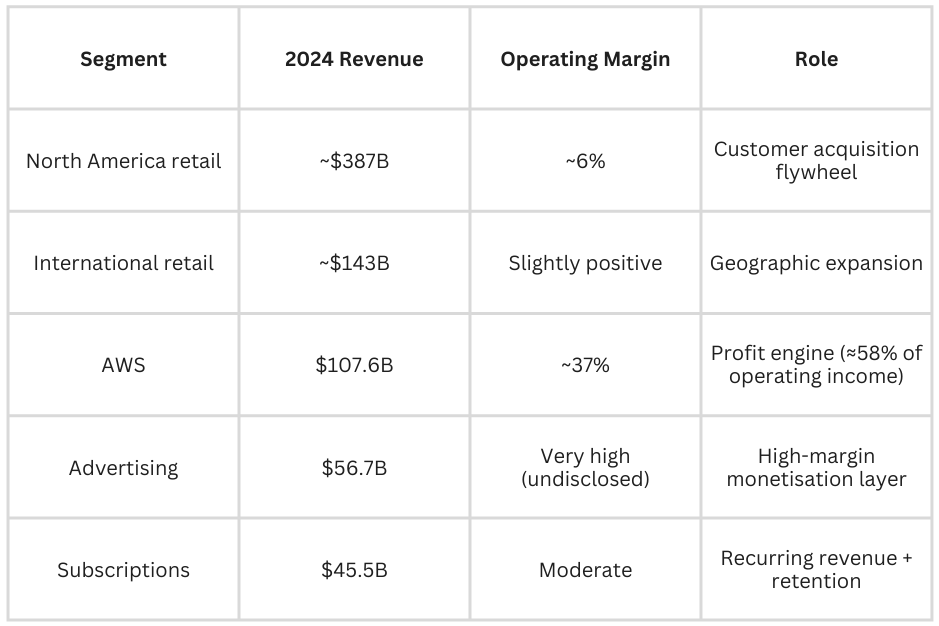

North America and International retail generated roughly $530 billion in combined revenue for 2024. Still, operating margins remain in the low single digits—approximately 6% in North America, with International only recently turning slightly positive after years of losses. Amazon treats retail as a customer acquisition flywheel: get people buying diapers and detergent, convert them to Prime members, then monetise them through faster shipping, streaming content, and the advertising inventory their eyeballs generate. The retail business isn’t designed to be hugely profitable on its own.

Amazon Web Services is where the real money lives. AWS generated $107.6 billion in revenue in 2024, growing at roughly 19% year-on-year, and delivered $39.8 billion in operating income—accounting for about 58% of Amazon’s total operating profit despite representing only around 17% of revenue. AWS isn’t just compute and storage anymore: it offers over 200 services spanning databases, machine learning, Internet of Things, and satellite ground stations. Customers include startups, enterprises, and governments. The Middle East has been a strategic growth region, with data centres in the UAE and Bahrain serving local enterprises, financial institutions, and government clients seeking data residency compliance.

Subscription services generated $45.5 billion in 2024. Amazon does not officially disclose Prime member counts, but third-party estimates place the figure at over 200 million globally. Prime creates predictable recurring revenue and deepens the customer flywheel—once a household subscribes, they consolidate spending on Amazon.

In other words, “Amazon” is now a cloud infrastructure company that subsidises a retail and media empire—not an online shop that dabbled in servers.

Advertising: The quiet profit engine hiding inside e-commerce 🕵️♀️

One of Amazon’s most valuable businesses sits far from the AWS headlines: digital advertising.

Amazon’s advertising services generated $56.7 billion in 2024, up 24% year-on-year—making it one of the world’s largest digital ad platforms, rivalling Google and Meta. Sponsored product listings, display ads across Amazon properties, and streaming ads on Prime Video generate revenue with minimal incremental capital. Amazon does not disclose standalone advertising profitability, but analysts estimate the segment operates at very high margins—potentially in the 40–50% range—making it one of the most profitable businesses inside Amazon.

Search intent monetisation: Unlike social media ads that interrupt, Amazon ads appear when customers are actively shopping. This makes Amazon’s ad inventory among the highest-converting in digital advertising—advertisers pay premiums because buyers are already in purchase mode.

Prime Video as ad surface: With the introduction of ads on Prime Video in 2024, Amazon unlocked a new inventory layer. Streaming ads carry significantly higher CPMs than product listings, and Amazon can target them using its unmatched purchase-history data—something Netflix and Disney+ can’t replicate.

Flywheel effect on retail margins: Advertising revenue effectively subsidises lower product prices and faster delivery, attracting more customers and generating more ad inventory. This self-reinforcing loop is why retail margins are improving even as Amazon invests heavily elsewhere.

For Intel, it was Altera hiding inside the turnaround chaos. For Amazon, advertising is the stable, high-margin engine hidden within the e-commerce narrative—and it grew slightly faster than AWS in 2024.

AI everywhere: From inference workloads to custom silicon 🌪️

Amazon is not just benefiting from the AI boom—it is actively positioning AWS as the infrastructure backbone for enterprises deploying machine learning at scale.

Custom silicon: Graviton, Trainium, Inferentia: AWS developed Graviton processors for general-purpose compute, offering better price-performance than traditional x86 chips. For AI specifically, Trainium chips handle model training, while Inferentia chips optimise inference workloads. These custom chips allow AWS to offer lower prices than competitors reliant on Nvidia GPUs, which remain supply-constrained and expensive. AWS has publicly claimed substantial price-performance advantages for Trainium-based instances over GPU-based equivalents for training large language models—though exact figures vary by workload and benchmark, and the comparison depends heavily on configuration.

Bedrock and SageMaker: Amazon Bedrock is a fully managed service that lets enterprises access foundation models from Anthropic, Stability AI, Meta, and Amazon’s own Titan models through APIs. SageMaker offers end-to-end machine learning workflows—data labelling, model training, deployment, and monitoring. Both services abstract away complexity, allowing companies to build AI features without hiring specialist teams or managing infrastructure. AWS has reported rapid growth in SageMaker adoption, though specific annual growth figures have not been disclosed in public filings.

The inference opening: AI workloads are split into training (upfront model building) and inference (ongoing predictions). Industry analysts widely project that inference will account for the majority of total AI compute over time, and that it favours cost-efficiency over raw performance. AWS’s custom silicon—particularly Inferentia—targets exactly this: high-throughput inference at lower cost than GPU-based alternatives. If the economics hold at scale, AWS could capture budget-conscious enterprises that can’t justify the cost of Nvidia pricing for every workload.

Internal AI as a cost lever: Internally, Amazon uses AI to optimise warehouse robotics, forecast inventory demand, personalise recommendations, and improve delivery routing. Management has highlighted billions in cost savings from logistics and fulfilment optimisation driven by AI and automation—a tangible demonstration that AI isn’t just a product to sell but an operational advantage within Amazon’s own business.

For a firm that both sells AI infrastructure and uses it internally, the boom is a double-edged advantage: revenue from customers plus operational savings.

Want to add Amazon to your portfolio? Trade AMZN directly from India on the Winvesta app. No US bank account needed!

🚀 Join 60,000+ investors — become a paying subscriber or download the Winvesta app and fund your account to get insights like this for free!

Keep reading with a 7-day free trial

Subscribe to Winvesta Crisps to keep reading this post and get 7 days of free access to the full post archives.